Samsung Life Insurance Shifts to Direct Management; KB and Shinhan Also Expand

Direct Ownership of Land and Buildings Required; Initial Investment of 50?60 Billion Won

Scope of Non-Covered Services Also Limited

Insurance companies are looking to enter the senior care industry, including nursing facilities, in response to the aging population. However, regulations such as the requirement for direct ownership of land and buildings, as well as limitations on the scope of non-covered services, are proving to be obstacles. Currently, the domestic nursing facility market is centered around individual business owners. There are calls to ease related regulations to lower entry barriers and promote competition in services.

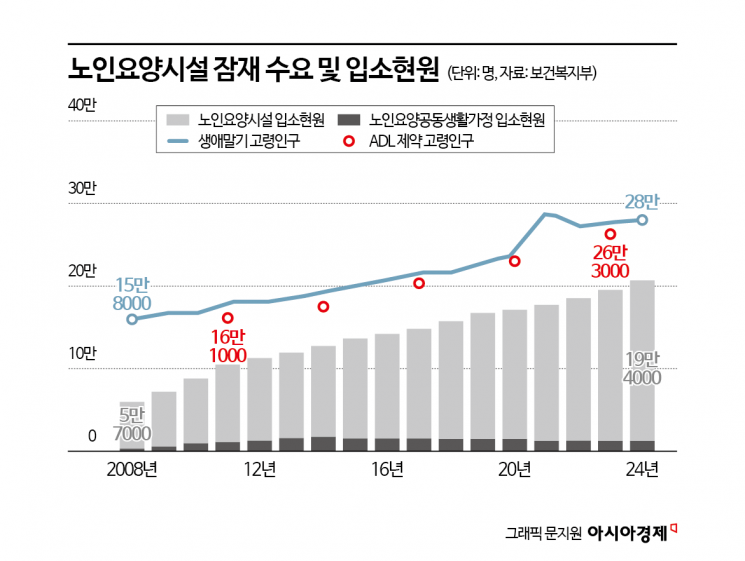

According to Statistics Korea, as of 2025, the proportion of the population aged 65 and older has exceeded 20%, and it is estimated to reach 30% by 2035. As the elderly population increases, demand for long-term care is also expected to rise. The Presidential Committee on Ageing Society and Population Policy projects that the number of people eligible for long-term care will surge from 1 million in 2023 to 1.71 million in 2035, and to 3.04 million in 2050.

In line with this trend, life insurance companies are also entering the nursing care market. Samsung Life Insurance has launched its subsidiary, Samsung Noble Life, and recently acquired the premium senior town "Samsung Noble County," which had been operated by the Samsung Life Public Welfare Foundation for 25 years. KB Life Insurance and Shinhan Life Insurance are also considering expanding their nursing facility businesses or strengthening related organizations. Their strategy is to connect their core insurance business with facility operations to manage the entire life cycle of customers.

Insurance companies are focusing on the nursing care market because they anticipate synergy effects. They can connect long-term care insurance or nursing care riders with the use of nursing facilities for their policyholders, and manage both insurance benefit payments and care services together.

However, significant challenges remain due to regulatory barriers. Nursing care facilities are required to own land and buildings directly, resulting in a high initial investment burden. According to the insurance industry, establishing a facility for 100 residents requires an investment of 50 billion to 60 billion won. The entry barrier is even higher in the Seoul metropolitan area due to high land prices.

An official from a life insurance company stated, "To build a facility in a location in the Seoul metropolitan area that is conveniently accessible for family visits, a tremendous amount of capital is required just for land acquisition. Even if you invest 60 billion won to build a facility for 100 residents, it is difficult to guarantee profitability with a monthly usage fee of around 3 million won per person."

Therefore, the industry believes that regulations should be rationally eased, such as allowing the leasing of land and buildings, provided that the residential safety and service quality for residents are sufficiently guaranteed. By enabling a wider range of operators to enter the nursing care market, service competition would increase, ultimately raising the overall quality of care.

Song Yoona, a research fellow at the Korea Insurance Research Institute, pointed out, "In Seoul, due to high land prices, small-scale facilities with fewer than 10 beds-which are exempt from ownership requirements-account for 53% of the total, a much higher proportion than the national average of 28.5%, and most are operated by individuals. While expanding public nursing care facilities, we should also consider allowing leases in areas where land prices are particularly high."

The restricted scope of non-covered services is also cited as a significant regulatory hurdle. According to the current Enforcement Regulations of the Long-Term Care Insurance Act and the Guidelines for Senior Health and Welfare Projects, nursing facility operators cannot collect deposits from residents. Non-covered services are also limited to meal ingredient costs, additional charges for higher-grade rooms, and grooming expenses. For items outside these categories, operators are effectively prohibited from charging fees. Due to these regulations, it is difficult to meet the diverse needs of the elderly, such as premium meal plans, customized rehabilitation and cognitive training programs, and digital healthcare services. With high initial investment costs and a structure that makes it difficult to generate profits, life insurers are hesitant to enter the market.

The situation is different overseas. According to the Korea Life Insurance Association, in Japan, daily living expenses and special service fees are distinguished separately from food and housing costs. Expenses such as hairdressing, personal item purchases, and hobby supplies are classified as daily living costs, while charges for special rooms or premium meals are categorized as special service fees, allowing users to choose. In Germany, additional services beyond the basic benefit range are permitted, and users pay separate fees for premium services.

Accordingly, the industry believes that to revitalize the long-term care market, it is necessary to: (1) reasonably expand the scope of non-covered services; (2) make requirements for direct land and building ownership more flexible (by allowing long-term leases or REITs); and (3) redesign incentives for private sector participation. It is also recommended that the public sector stably expand the basic infrastructure to guarantee minimum access to care, with the private sector driving service upgrades through quality competition based on this foundation.

However, some point out that if large life insurance companies with strong capital bases enter the nursing care market in earnest, the quality of services available could vary greatly depending on wealth and income levels, potentially intensifying polarization in care services. Therefore, while easing entry regulations, it is essential to establish institutional measures to maintain public interest.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}