President Lee Calls for Regulation of Speculative Non-Resident Single-Home Owners

June 27 Measures Blocked New Gap Investments... Regulatory Scope Expanding to Existing Gap Investors

Jeonse Loan Restrictions and Stricter DSR Regulations Likely

Following last year's June 27 measures that blocked new gap investments, the financial authorities are now tightening regulations on "non-resident single-home gap investors"-those who purchase a home using jeonse deposits or loans but reside elsewhere. With President Lee Jaemyung naming "speculative non-resident single-home owners" as a regulatory target, the scope of regulation is expanding from owners of multiple homes to single-home gap investors.

Market observers believe that going forward, the government will specify the definition of "speculation" based on factors such as amount and region, and will introduce measures to further restrict funding sources for gap investments. There is speculation that a range of options will be considered, such as restricting jeonse loan eligibility for certain gap investors, strengthening the debt service ratio (DSR) regulations, and tightening the screening process for tenants’ jeonse loans.

Financial Authorities: "Speculative Non-Resident Single-Home Owners Also Subject to Regulation"

On March 3, an official from the financial authorities stated, "We are closely examining regulations on speculative non-resident single-home owners to stabilize the real estate market," adding, "New gap investments have been blocked by the June 27 measures, but no separate action has been taken for existing gap investors, so we are considering institutional improvements."

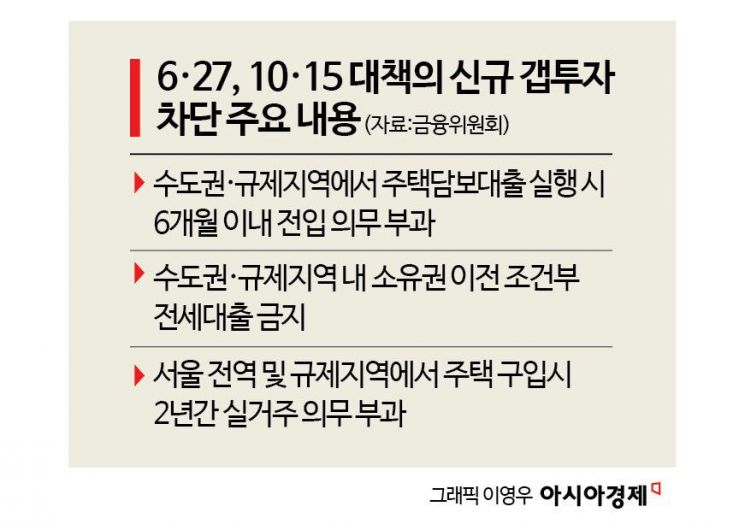

The financial authorities believe that purchasing homes using jeonse deposits or loans as leverage has triggered a chain move to higher-priced areas, intensifying upward pressure on prices. Accordingly, the Financial Services Commission blocked new gap investment channels through the June 27 measures. In the Seoul metropolitan area and other regulated regions, a requirement was imposed to move into the property within six months when taking out a mortgage, and tenants were prohibited from taking out new jeonse loans if the property changed ownership. Subsequently, the October 15 measures imposed a two-year residence requirement for home purchases throughout Seoul, effectively shutting down new gap investments.

However, those who acquired homes using jeonse deposits before the June 27 measures have so far been excluded from direct regulation. The financial authorities are now considering additional management measures to ensure that holding a home without actually residing in it becomes unfavorable for asset growth.

Considering Ban on Jeonse Loans and Tighter DSR Regulations

As the government begins preparing tax and financial regulations targeting speculative non-resident single-home owners, the market is speculating on what kinds of regulatory measures financial authorities will introduce.

The most likely measure is the strengthening of jeonse loan regulations for non-resident single-home owners. Currently, in regulated areas such as Seoul and the metropolitan area, single-home owners can obtain up to 200 million won in jeonse loans if they wish to rent another property. However, if the government sets criteria such as property value and location to classify someone as a "speculative non-resident single-home owner," there is speculation that jeonse loans could be fundamentally prohibited for this group.

There is also discussion about applying the DSR (Debt Service Ratio) regulation more strictly. Under the October 15 measures, for single-home owners in regulated areas, not only the principal and interest of mortgages but also the interest payments on jeonse loans are included in the DSR (40%) calculation. In the future, there may be discussions about including the principal of jeonse loans as well, or differentiating the applicable ratio.

Additionally, the scenario of expanding the June 27 policy of blocking new gap investments to include existing gap investors cannot be ruled out. One possible measure being considered is strengthening the review process when extending the maturity of jeonse loans already taken by tenants in homes owned by non-resident single-home owners.

An official in the financial sector commented, "Restricting jeonse loans for single-home owners with expensive properties would be a relatively less burdensome policy for the authorities," adding, "Given the potential impact on the jeonse market, a phased approach based on amount and region could be considered."

However, there are concerns that applying uniform regulations based solely on residence status could negatively impact those who have to move due to unavoidable reasons, such as job relocation, children's education, or caring for parents. This is why there are calls to carefully design exceptions even as regulations are tightened.

Meanwhile, on this day, the Financial Services Commission is convening financial sector representatives for a meeting chaired by Vice Chairman Kwon Daeyoung to discuss loan regulation measures for normalizing the real estate market. The meeting is expected to address not only restrictions on the extension of loans for owners of multiple homes, but also the strengthening of loan regulations related to non-resident single-home owners. It has also been reported that the financial authorities are considering restrictions on extending loan maturities not only for residential rental business operators who own apartments in regulated areas, but also for non-residential rental business operators who own commercial properties such as retail spaces or offices.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}