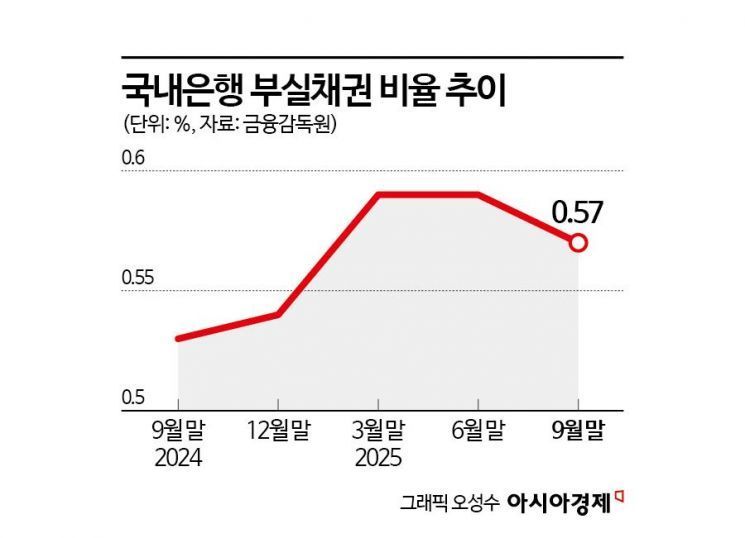

As of the end of September this year, the non-performing loan (NPL) ratio of domestic banks stood at 0.57%, up 0.04 percentage points from the same period last year.

According to the "Status of Non-Performing Loans at Domestic Banks as of the End of September 2025 (Provisional)" released by the Financial Supervisory Service on November 27, the NPL ratio of domestic banks at the end of September this year was 0.57%, an increase of 0.04 percentage points compared to the same period last year (0.53%). Compared to the previous quarter (0.59%), it fell by 0.02 percentage points.

The amount of non-performing loans was 16.4 trillion won, a decrease of 200 billion won compared to the previous quarter (16.6 trillion won). By category, non-performing loans consisted of 13.1 trillion won in corporate loans, 3 trillion won in household loans, and 300 billion won in credit card receivables.

During the same period, the balance of loan loss provisions stood at 27.1 trillion won, down 300 billion won from the previous quarter (27.4 trillion won). The loan loss provision coverage ratio was 164.8%, a decrease of 0.7 percentage points from the previous quarter (165.5%). Compared to the same period last year (188.0%), it dropped sharply by 22.6 percentage points.

Newly generated non-performing loans during the same period amounted to 5.5 trillion won, a decrease of 900 billion won from the previous quarter (6.4 trillion won).

New corporate non-performing loans totaled 3.9 trillion won, down 1 trillion won from the previous quarter (4.9 trillion won). Newly generated household non-performing loans were 1.4 trillion won, similar to the previous quarter (1.4 trillion won).

The non-performing loan ratio for corporate loans was 0.71%, down 0.01 percentage points from the previous quarter. By sector, the NPL ratio for large corporate loans was 0.41%, the same as the previous quarter (0.41%). In contrast, the NPL ratios for small and medium-sized enterprises and small corporations fell by 0.02 percentage points and 0.05 percentage points, respectively, to 0.88% and 1.11% compared to the previous quarter.

During the same period, the NPL ratio for household loans was 0.30%, down 0.02 percentage points from the previous quarter (0.32%). The NPL ratio for mortgage loans was 0.20%, a decrease of 0.03 percentage points from the previous quarter (0.23%), while the NPL ratio for other unsecured loans rose by 0.01 percentage points to 0.62% compared to the previous quarter (0.61%). The NPL ratio for credit card receivables was 1.87%, down 0.06 percentage points from the previous quarter (1.93%).

An official from the Financial Supervisory Service stated, "The balance and ratio of non-performing loans at domestic banks improved compared to the previous quarter due to a decrease in new non-performing loans," and added, "Going forward, we will continue to monitor asset quality, guide banks to strengthen their management of non-performing loans through active collection and sales, and encourage them to enhance their loss-absorbing capacity in advance so that they can maintain smooth funding even if internal and external uncertainties increase."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}