Credit Finance Association Targets Completion of Technology Verification in First Half of Year

PG Companies Seek to Expand Influence in the Payments Market

"Limited Consumer Impact" Expected

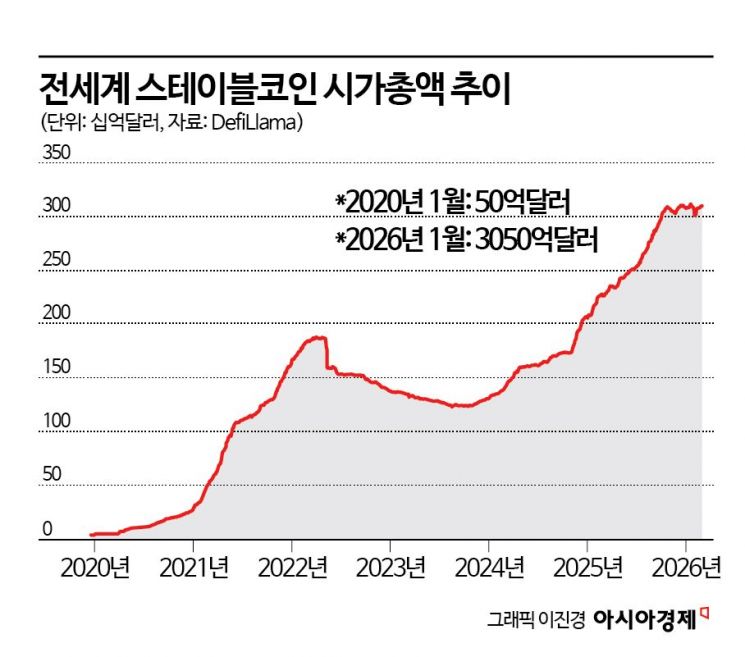

As discussions surrounding the institutionalization of Korean won stablecoins accelerate, a sense of tension is rising across the entire payments and settlement industry. Credit card companies are adopting strategies to incorporate stablecoins into their existing approval and settlement systems, while payment gateway (PG) companies are seeking to elevate their position as payment entities by applying for trademarks and internalizing wallet infrastructure. Industry observers note that the sector has entered a phase of structural realignment, with competition intensifying over which players will control the center of the payments market-moving beyond a simple new business rivalry.

According to the financial sector on March 4, a stablecoin task force led by the Credit Finance Association recently shared a draft guideline with the industry, aiming to implement anti-money laundering (AML), know-your-customer (KYC), fraud detection systems (FDS), and the travel rule (which mandates sender and receiver information for virtual asset transfers) within the existing card company control framework. A proof-of-concept (PoC) will begin this month to verify whether Korean won transactions can be processed in stablecoin form, with the goal of completing this process in the first half of this year.

From the perspective of credit card companies, the key is to 'maintain credit functionality.' While stablecoin payments are inherently prepaid, card companies provide additional features such as postpaid settlement, installment plans, and point accumulation. The industry believes that even if stablecoins are introduced, if the final approval and settlement are processed through card infrastructure, card companies will be able to maintain a portion of their existing revenue model.

Additionally, the card industry is focusing on overseas payment domains. Currently, international payments involve fees for using global brand networks and currency exchange. If real-time settlement using stablecoins becomes possible, dependency on international networks could decrease, and there is potential to adjust the cost structure. As a result, some in the industry predict that stablecoins could impact the settlement framework currently dominated by Visa and Mastercard.

The PG sector also views stablecoins as a tool for innovating settlement infrastructure, not simply as a payment method. Major players such as Toss (Viva Republica), Naver Pay, Kakao Pay, KG Mobilians, NHN KCP, and Danal are actively applying for trademarks related to Korean won stablecoins and preparing to enter the market.

PG companies have secured payment and settlement data based on direct contracts with hundreds of thousands of merchants. By adding digital asset wallets, they could establish a blockchain-based settlement framework connecting merchants and PG companies. In this scenario, a model that bypasses the card approval network is theoretically possible. An industry official stated, "If the card approval network is bypassed, the fees that card companies typically receive may be reduced or eliminated. How this gap is addressed could lead to adjustments in the fee structure for PG companies, which in turn may change the actual costs borne by merchants."

Despite the heightened tension across the payments industry, it is expected that consumers will experience limited changes for the time being. In South Korea's offline payment environment, card and simple payment infrastructures are already highly advanced, making it difficult for consumers to perceive significant differences in convenience. Currently, the actual use of stablecoins is mixed between virtual asset trading and payment purposes, and stablecoins based on the US dollar are estimated to account for less than 1% of all transactions classified as retail payments. Baek Jinsoo, a research fellow at the Korea Institute of Finance, stated, "The fact that the proportion of retail payments is limited shows that stablecoins are currently used more for settlement within financial infrastructure or for cross-border remittances than for everyday transactions. Payment companies are increasingly utilizing stablecoins as a means to improve settlement efficiency," he said.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}