Oil Prices Surge After U.S. Attack on Iran

Rising Inflation Concerns Drive Treasury Yields Higher

Focus Shifts to Whether the Conflict Drags On

WGBI Inflows Seen as Supply-and-Demand Tailwind

The domestic bond market, which had seemed to catch its breath following the markedly dovish February Monetary Policy Board meeting of the Bank of Korea, has once again been swept by uncertainty. This is due to renewed concerns about rising inflation, as international oil prices surged after the United States attacked Iran. However, there are also expectations that funds related to the World Government Bond Index (WGBI), which may begin to flow in as early as the end of this month, will serve as a buffer for supply and demand.

Bond Market Volatile Amid Middle East Risks

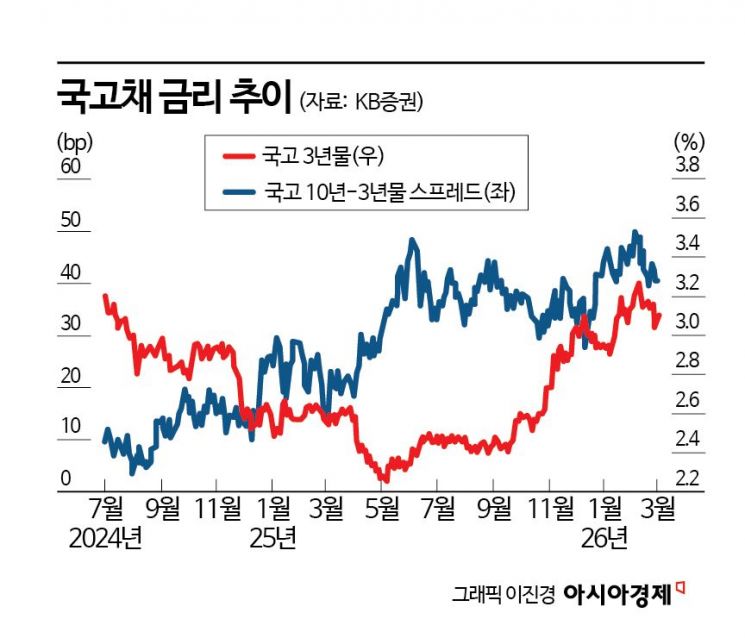

According to the Korea Financial Investment Association, on March 3-the first trading day after the military conflict between the United States and Iran-the three-year Korean Treasury bond yield in the Seoul bond market rose by 13 basis points (1bp = 0.01 percentage point) from the previous session to 3.180%. The 10-year Treasury yield also climbed to 3.594%, reversing last week’s post-Monetary Policy Board meeting drop below the 3.4% level. Rising bond yields mean falling bond prices.

This is interpreted as the result of global financial markets being shaken by the escalating military conflict between the United States and Iran over the weekend. Jae Kyun Ahn, a researcher at Korea Investment & Securities, noted, "The Iranian crisis has emerged as an unexpected negative factor in what had been a somewhat improving bond market," adding, "For now, the upside risk is higher."

Unlike the stock market, which has continued to hit record highs, the bond market has faced downward pressure since the end of last year amid rising expectations for economic growth and uncertainty over policy direction. The three-year Korean Treasury yield, which was in the 2.9% range at the end of last year, surged to an annual high of around 3.26% on February 9, and the spread over the base rate widened to 60-70 basis points. This is nearly double the post-pandemic average of 35 basis points. However, following last week’s Monetary Policy Board meeting, a dot plot indicating a preference for a rate hold was presented, and Bank of Korea Governor Rhee Changyong hinted at the possibility of outright purchases of Korean Treasuries by stating that the spread was excessive. The bond market immediately breathed a sigh of relief. In intraday trading, the three-year yield fell to 3.03%, and securities analysts flooded the market with comments such as, "The bond market, which had been entirely weak, has reached a turning point," and "The peak in yields has essentially been confirmed."

However, the outbreak of the US-Iran conflict has dealt a direct blow to the bond market, as concerns about a 'V-shaped rebound' in inflation in the second half of the year have not fully abated and now present an additional variable. Sung Soo Kim, a researcher at Hanwha Investment & Securities, said, "Given that about 72% of Korea’s crude oil imports and 35% of natural gas imports come from the Middle East, the shock to the Korean Treasury market could be greater than that to the US market," and predicted the upper limit for the 10-year Treasury yield at 3.65%. Jae Kyun Lim, a researcher at KB Securities, said, "The conflict in the Middle East will put upward pressure on international oil prices," adding, "While concerns about rate hikes have eased somewhat since the February Monetary Policy Board meeting, the pace and magnitude of this easing will be slower and smaller."

The Key Issue: Duration of the Crisis... 'Positive Supply Factors Awaited'

Experts cite the duration of the current situation as the most critical variable. Yeosam Yoon, a researcher at Meritz Securities, warned, "If the situation lasts more than a month and oil prices exceed $100, this will heighten tension in the bond market." Researcher Ahn also pointed out, "If the crisis persists for more than two months, there is concern that major bond yields could retest their annual highs," and added, "Both Korea and the US could see widening pressure on the yield curve."

On the other hand, researcher Lim projected, "In the short term, escalating attacks by both sides will increase uncertainty," but also noted, "Given that the US faces mid-term elections this year, the situation is likely to be resolved before autumn at the latest."

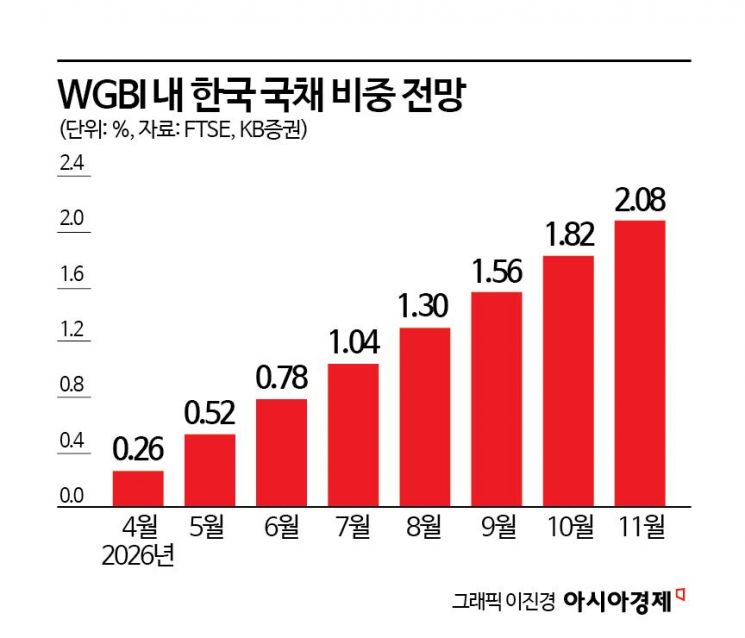

On the supply and demand side, there are also factors in place to cap the upper end of yields. With Korean government bonds set to be included in the WGBI in April, related global funds are expected to begin flowing in from the end of this month. In this case, long-term bonds are likely to benefit the most. KB Securities expects the proportion of Korean government bonds in the WGBI to rise from 0.26% in April to over 1% in July, and surpass 2% in November.

Pension fund inflows are also anticipated. Seungwon Kang, a researcher at NH Investment & Securities, estimated, "As of February, the National Pension Service would need to purchase domestic bonds exceeding 58 trillion won in order to meet its asset allocation targets." Following verbal intervention by the Bank of Korea, the government is also working to stabilize the bond market by minimizing government bond issuance in the first quarter. The securities industry currently projects that the issuance progress will approach the lower end of the government’s first-quarter target (27-30%) by March.

Researcher Kim noted, "The Bank of Korea’s commitment to market stability was confirmed at the February Monetary Policy Board meeting, and weak domestic demand momentum may partially offset supply-side inflationary pressures." He added, "Given that Iran’s ability to blockade the Strait of Hormuz is judged to be limited, war-related yield rises are likely to be temporary." Researcher Kang stated, "The main drivers of the early-year weakness in the government bond market were concerns about up to two rate hikes and a supply-demand gap," predicting that as these two factors ease, the domestic bond market will steadily stabilize in March. NH Investment & Securities projects the three-year and 10-year Korean Treasury bond yield bands for March to be 2.95-3.20% and 3.30-3.60%, respectively.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}