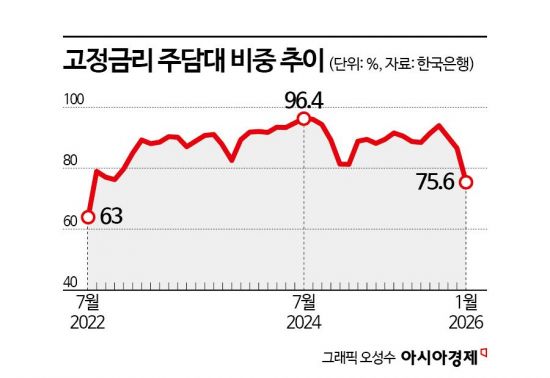

75.6% in January, Down 11 Percentage Points in One Month

Largest Drop in Five Years Due to Widening Gap Between Fixed and Variable Rates

The proportion of borrowers choosing a five-year fixed interest rate for mortgage loans has dropped sharply. Within just one month, it fell by 11 percentage points, reaching the lowest level in three and a half years. This decline is attributed to the increase in the five-year financial bond rate, which serves as a benchmark interest rate, causing fixed-rate mortgage loans to have higher rates than variable-rate mortgages. Although banks are encouraging customers to choose fixed-rate mortgage loans by adjusting their interest rate spreads, the gap between the rates remains persistent.

According to the economic statistics system of the Bank of Korea on March 3, the proportion of fixed-rate mortgages among newly issued home loans by deposit banks stood at 75.6% at the end of January. This is the lowest level recorded since July 2022 (63%), marking the lowest point in three and a half years. The month-on-month decline was 11 percentage points, the largest drop in the past five years.

The proportion of fixed-rate mortgages had remained high, even rising further due to government incentives and other factors, despite the interest rate cut cycle that began in the second half of 2024. As recently as October last year, the proportion was as high as 94%, but it has dropped for three consecutive months as more borrowers have rapidly shifted to choosing variable-rate mortgages. The previously maintained 80-90% range over the past three years has also collapsed.

This recent drop is considered to be due to the interest rate gap between variable-rate and fixed-rate mortgages. As of the previous day, the mortgage rates at the five major commercial banks (KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup) were as follows: the five-year hybrid (fixed for five years, then switching to variable) ranged from 4.18% to 6.52% per annum, and the six-month variable-rate ranged from 3.65% to 6.35%. Fixed-rate mortgage loans have interest rates that are 0.53 percentage points higher at the lower end and 0.17 percentage points higher at the upper end compared to variable-rate mortgages.

Banks are uniformly setting higher spreads for variable-rate mortgages to encourage borrowers to choose fixed-rate mortgages. Specifically, the spreads for variable-rate mortgages are set between 1.79% and 3.54%, while for fixed-rate mortgages, they range from 1.17% to 2.86%, resulting in a difference of about 0.6 percentage points.

Nevertheless, the final interest rates for fixed-rate and variable-rate mortgages have diverged due to differing trends in their respective benchmark rates: the five-year financial bond rate for fixed-rate mortgages and the short-term financial bond rate and the Cost of Funds Index (COFIX) for variable-rate mortgages. According to the Korea Financial Investment Association, the five-year financial bond rate rose from 3.497% in early January to 3.723% in just one month. A financial industry insider explained, "Long-term rates are more sensitive to the future direction of policy or economic outlook than short-term rates," adding, "With expectations of a policy rate cut having disappeared and concerns over expansionary fiscal policy by the government, long-term rates have risen at a faster pace."

Although the five-year financial bond rate eased somewhat to 3.572% as of February 27, following Bank of Korea Governor Rhee Changyong's remark at the February monetary policy press briefing that it was 'excessive compared to the policy rate,' there is still a gap of about 0.76 percentage points compared to the six-month financial bond rate (2.812%). In particular, another benchmark for variable-rate mortgages, COFIX, turned downward in January to 2.77% for the first time in five months, suggesting that even more borrowers may opt for variable-rate mortgages in the future. A banking industry official commented, "Although the policy rate is expected to remain on hold for an extended period, market rates have become increasingly volatile," adding, "Borrowers should carefully consider future interest rate outlooks before choosing the type of mortgage."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}