March business sentiment index outlook at 97.6... up 6.6p

Driven by improved working days and expectations for semiconductor equipment market conditions

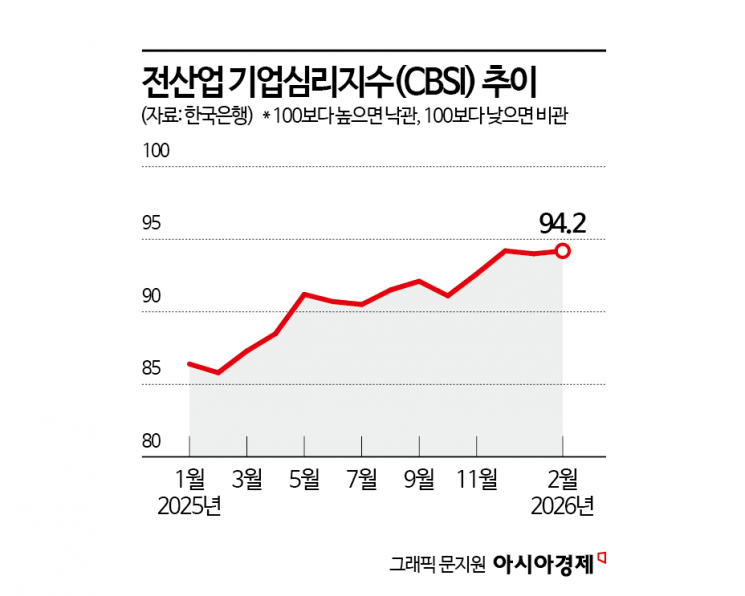

February business sentiment index rebounds 0.2p to 94.2

Driven by expectations that the semiconductor supercycle will bring a spring breeze to the economy, the business survey outlook for next month has climbed to its highest level in 3 years and 3 months, moving close to the baseline.

'Combined effects' of recovery in March working and business days + expectations for semiconductor equipment market conditions

According to the "February 2026 Business Survey and Economic Sentiment Index (ESI)" released by the Bank of Korea on the 25th, the outlook for the Composite Business Survey Index (CBSI) for all industries for next month came in at 97.6, up 6.6 points from the previous month. This is the highest level in 3 years and 3 months since November 2022 (97.6). The magnitude of the increase is also the largest since November 2020 (7.1 points). The rise in both the manufacturing and non-manufacturing outlooks produced this result. The CBSI is a business sentiment indicator derived from key indices within the Business Survey Index (BSI). Using the long-term average (from January 2003 to December 2025) as the reference value of 100, a reading above 100 is interpreted as corporate expectations for the economy being more optimistic than the long-term average, while a reading below 100 is interpreted as pessimistic.

The manufacturing outlook for March recorded 98.9, up 3.9 points from the previous month, marking the highest level since September 2022 (101.2). In particular, the outlook for small and medium-sized manufacturing firms improved sharply from 90.5 in February to 97.0 in March, a gain of 6.5 points, which had a large impact. The manufacturing outlook rose mainly in electronic, visual, and communication equipment, other machinery and equipment, and medical and precision instruments. Lee Heunghu, head of the Economic Sentiment Survey Team at the Economic Statistics Department 1 of the Bank of Korea, explained, "Compared with February, when the Lunar New Year holidays fell, the number of working days improved, and expectations for business conditions in semiconductor equipment segments such as other machinery and equipment and medical and precision instruments also played a role."

The non-manufacturing outlook also improved sharply. The non-manufacturing outlook for March stood at 96.8, up 8.4 points from the previous month, the highest level since October 2023 (98.7). The increase is the largest since August 2020, when it rose by 9.1 points. The non-manufacturing outlook rose mainly in wholesale and retail trade, information and communications, and professional, scientific, and technical services. Lee said, "Wholesale and retail trade improved on expectations of an increase in the number of business days, and information and communications improved on continued expectations for investment in artificial intelligence (AI). In addition, as the weather warms in March and there are expectations that seasonal orders from the public sector will increase toward the end of the quarter, professional, scientific, and technical services also rose."

Rebound in February despite fewer working days due to Lunar New Year holidays... Increased pre-sale supply and expectations for expanded AI investment

This month, the CBSI for all industries rebounded for the first time in a month, posting 94.2, up 0.2 points from the previous month. Manufacturing came in at 97.1, down 0.4 points from the previous month due to factors such as fewer working days during the Lunar New Year holidays, but non-manufacturing rose for the first time in a month, climbing 0.5 points to 92.2.

In February, actual manufacturing performance declined mainly in food, automobiles, and metal processing. The food sector was affected by the spread of three major livestock infectious diseases, including avian influenza (AI), as well as rising prices of imported agricultural products such as wheat and soybeans. The automobile sector could not avoid the impact of a sharp reduction in the number of working days, which fell from 23.5 days in January to 19 days this month. Metal processing was also hit by fewer working days and higher raw material prices.

By contrast, actual non-manufacturing performance this month rose mainly in real estate and information and communications. In real estate, expectations were boosted by anticipated increases in pre-sale supply, as some companies began scheduling apartment pre-sales. According to the Housing Industry Research Institute, the Apartment Pre-sale Supply Outlook Index improved from 84.4 in December last year to 92.2 in January this year and 98.6 in February. In information and communications, the early-year order gap in the software development sector was filled, and expectations of expanded investment in AI infrastructure also played a role.

The ESI, which combines the BSI and the Consumer Sentiment Index (CSI), recorded 98.8, up 4.8 points from the previous month, the highest level since September 2022 (99.0). The cyclical component, which removes seasonal and other factors, stood at 97.2, up 0.8 points from the previous month.

Meanwhile, this survey was conducted from the 5th to the 12th of this month on 3,524 corporate entities nationwide. A total of 3,229 companies responded (a response rate of 91.6%), including 1,793 in manufacturing and 1,436 in non-manufacturing.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}