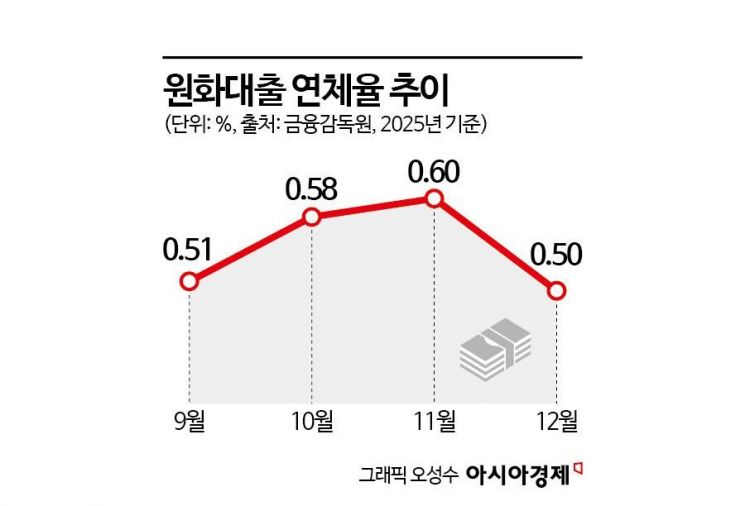

Downturn After Increases in October and November

Driven by Fewer New Delinquencies and Year-End Delinquent Loan Cleanups

Delinquency Rate Still Higher Than a Year Ago

As the scale of year-end write-offs of delinquent loans increased, the delinquency rate on won-denominated loans at domestic banks turned downward for the first time in two months. However, compared with the previous year, the corporate loan delinquency rate edged up for both large corporations and small and medium-sized enterprises (SMEs). This is seen as a result of companies' repayment capacity not having fully recovered yet, amid ongoing economic slowdown and the impact of high interest rates.

According to the Financial Supervisory Service on February 24, the delinquency rate on won-denominated loans at domestic banks (based on principal and interest overdue by one month or more) stood at 0.50% at the end of December 2025, down 0.10 percentage point from 0.60% at the end of the previous month. The delinquency rate on won-denominated loans had risen for two consecutive months in October and November last year, but turned downward in December.

This was due both to a decrease in newly delinquent loans and to large-scale write-offs and disposals of delinquent assets. At the end of last year, newly generated delinquencies amounted to 2.4 trillion won, down 200 billion won from the previous month. In contrast, the scale of delinquent loan resolution surged to 5.1 trillion won, an increase of 3.2 trillion won from the previous month.

As a result, the new delinquency rate at the end of last year fell to 0.10%, down 0.01 percentage point from 0.11% in the previous month. The new delinquency rate is calculated by dividing the amount of newly delinquent loans in a given month by the loan balance at the end of the previous month. Delinquency rates typically rise during a quarter and then decline at quarter-end due to large-scale clean-ups, and analysts see the year-end clean-up effect as having been reflected this time as well.

For both corporations and households, delinquency rates declined compared with the previous month. The corporate loan delinquency rate fell to 0.59%, down 0.14 percentage point from 0.73% a month earlier, while the household loan delinquency rate dropped to 0.38%, down 0.06 percentage point from 0.44%. More specifically, the rates for large corporations (0.12%), SMEs (0.72%), small corporate borrowers (0.78%), and individual business owners (0.63%) each declined by between 0.04 and 0.20 percentage point. Mortgage loans (0.27%) and unsecured and other credit loans (0.75%) also fell by 0.03 percentage point and 0.15 percentage point, respectively.

However, the overall delinquency rate on won-denominated loans was 0.06 percentage point higher than at the end of the same month a year earlier (0.44% at the end of December 2024). Even taking into account that year-end figures usually reflect the effect of large-scale write-offs of delinquent loans, the December reading is the highest for a December since December 2015 (0.58%).

Compared with one year earlier, the corporate loan delinquency rate rose by 0.09 percentage point, with the rates for large corporations and SMEs up 0.09 percentage point and 0.10 percentage point, respectively. The rates for small corporate borrowers and individual business owners also increased by 0.14 percentage point and 0.03 percentage point, respectively. While the overall household loan delinquency rate was unchanged from a year earlier, both mortgage loans and unsecured and other credit loans rose by 0.01 percentage point. This suggests that the repayment capacity of both corporations and households has weakened somewhat compared with the previous year.

The Financial Supervisory Service stated, "In preparation for a possible increase in domestic and external uncertainties, we plan to continue to encourage banks to strengthen asset quality management, including by increasing provisions for bad debts in vulnerable sectors and industries."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}