Publication of the report

"The Dawn of Autonomous Driving: Competitive Strategies in the Robotaxi Market"

Market analysts say that this year could reveal whether robotaxis can move beyond the technology demonstration stage and transition into an industrial model that generates real revenue.

On the 23rd, Samjong KPMG published a report titled "The Dawn of Autonomous Driving: Competitive Strategies in the Robotaxi Market." The report defines robotaxis not as a simple technology experiment, but as a comprehensive industrial ecosystem competition centered on data, assets, regulation, and reputation.

According to the "Global Automotive Executive Survey 2025" released by KPMG, 87% of respondents expect autonomous driving to become the standard across all vehicle types by 2030. The autonomous vehicle market is projected to grow at an average annual rate of about 23% from last year, reaching 122 billion dollars (approximately 17.5802 trillion won) by 2030.

Robotaxis have significant strategic importance as a business model that can both test the public acceptance of autonomous driving technology and generate substantial revenue. Global market research firm MarketsandMarkets forecasts that the robotaxi market will record high growth of around 71% to 108% annually from 2023 to 2030, pointing to its explosive expansion potential.

The report identifies autonomous driving software, vehicle platform development and mass production, and ride-hailing ecosystem building and operation as the core capabilities for realizing robotaxis. Based on these, it derives six business models: complete vertical integration, platform lifetime extension, solution-integrated operation, next-generation ride-hailing, manufacturing-based technology integration, and system orchestration.

The complete vertical integration model internalizes all three capabilities, resulting in low collaboration intensity and low solution openness. Tesla and Amazon’s Zoox are representative examples. The platform lifetime extension model sources vehicle mass production from external OEMs while promoting the generalization of autonomous driving solutions. Baidu (Apollo Go) and Pony.ai are typical players.

The solution-integrated operation model works closely with external OEMs and focuses on commercializing the autonomous driving service itself; Waymo is a representative case. The next-generation ride-hailing model is structured around platform operation capabilities combined with external technologies, with Uber and Lyft being the leading companies.

The manufacturing-based technology integration model is a method by which traditional automakers internalize autonomous driving technology or procure it externally and integrate it. Hyundai Motor Group (centered on Motional) and Volkswagen Group (centered on MOIA) fall into this category.

Finally, the system orchestration model internalizes certain capabilities while flexibly combining them through strategic partnerships, as demonstrated by the collaboration among Stellantis, Nvidia, Uber, and Foxconn.

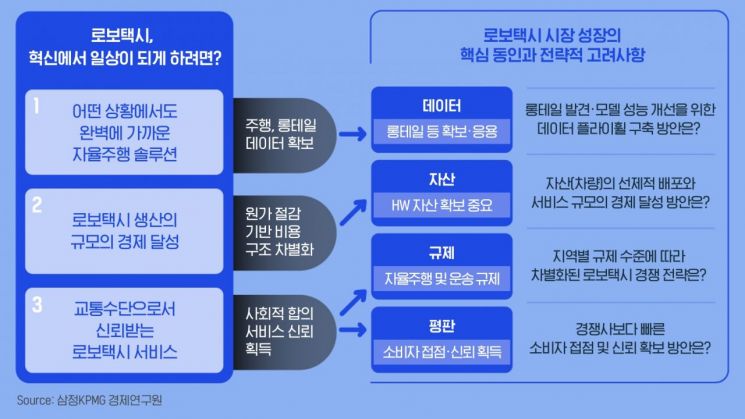

The report presents data, assets, regulation, and reputation as the key challenges that must be addressed for robotaxis to become an everyday mode of transportation. The core of data competitiveness is building a "data flywheel." In particular, securing so-called "long-tail data" for very low-frequency exceptional situations is crucial. Because of the nature of the long tail, it is difficult to collect real-world cases, so attention must be paid to ways of generating such data. The report proposes multiple strategies, including procuring proven platforms for data generation, in-house development of generative AI-based simulation, and hybrid models that combine external procurement with in-house development.

On the asset side, early deployment of vehicles to secure first-mover advantage in the market and cost reduction are key. The report analyzes that asset lightness must be achieved through mass production systems, utilization of existing complete-vehicle platforms, and autonomous driving foundry (contract manufacturing) models in order to be price-competitive with existing taxi and ride-hailing services. Responding to the regulatory environment is also important. In the early stages, securing assets takes priority, but as the market matures, operational efficiency becomes the decisive factor for competitiveness. Demand-forecast-based fleet operation, minimizing charging and maintenance time, and standardizing operating models are presented as major tasks.

Reputation management is also a critical variable. Ensuring the explainability of AI decision-making processes, establishing transparent response systems in the event of accidents, and building safety infrastructure in cooperation with governments are cited as key elements in securing trust.

"This year is a critical inflection point at which the robotaxi market must prove its existence not merely as a demonstration of autonomous driving technology, but as a future growth engine and a profitable business model," said Jaeyeon Kim, Executive Director and Automotive Industry Leader at Samjong KPMG. "For domestic companies to enter the leading group in the global robotaxi market, they must secure structural competitive advantages across data, assets, regulation, and reputation."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}