Corporate Loan Balances at Banks Rise for Five Consecutive Months

Growth in Mortgage Loans Slows Significantly

Need to Manage Delinquency Rates and Shell Loans for Soundness

As the government emphasizes productive finance, the growth of corporate loans by banks is accelerating. With mounting concerns over excessive household debt, banks are expected to continue reducing household loans such as mortgage loans and expanding corporate loans. However, some point out that, due to the nature of corporate loans, delinquency rates are higher than those of household loans, and the volume of so-called "non-performing loans," also known as "shell loans," is increasing, which means banks must pay close attention to risk management.

Bank Corporate Loan Balances Rise for Five Consecutive Months

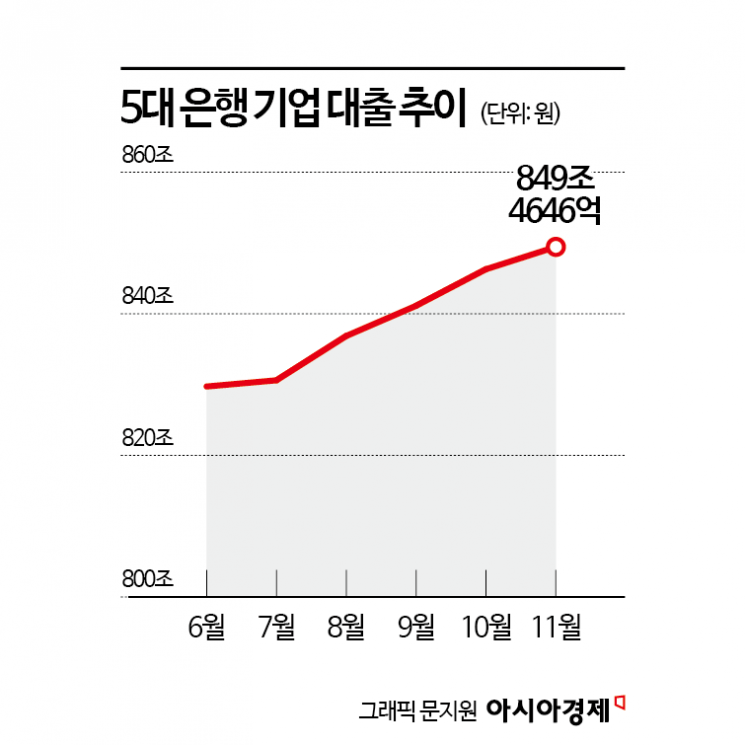

According to the financial sector on December 3, the outstanding balance of corporate loans at the five major commercial banks-KB Kookmin Bank, Shinhan Bank, Hana Bank, Woori Bank, and NH Nonghyup Bank-stood at 849.4646 trillion won at the end of last month, up 3.1587 trillion won from the previous month. During the same period, the increase in household loans was 1.5125 trillion won, and the increase in mortgage loans was 639.6 billion won, making the growth in corporate loans notably larger.

The outstanding balance of corporate loans at the five major banks has been on the rise for five consecutive months since July. Over the five-month period, corporate loans increased by a total of 19.6263 trillion won. This increase is larger than the 13.2996 trillion won rise in household loans during the same period. The growth in lending was centered on small and medium-sized enterprises (SMEs) rather than large corporations: over the five months, loans to large corporations increased by 6.4851 trillion won, while loans to SMEs grew by 13.1412 trillion won.

Analysts attribute this trend to the Lee Jaemyung administration's emphasis on productive finance, prompting banks to competitively expand corporate lending. The government has argued that excessive real estate lending leads to rising housing prices and polarization, and has requested that banks expand lending to productive sectors such as corporate loans rather than household loans. According to the Bank for International Settlements (BIS), as of the first quarter of this year, Korea's household debt-to-GDP ratio stood at 89.5%, one of the highest among major economies. As a result, banks have been reducing the proportion of household loans, including mortgage loans, and increasing corporate loans in the second half of the year.

An official from one of the commercial banks explained, "In the case of mortgage loans, we significantly reduced the scale because they fall under the total household loan regulation," adding, "Instead, we established a business policy to expand corporate lending."

There are also concerns that the aggressive expansion of corporate lending by banks could lead to future financial soundness issues. Corporate loans generally have higher delinquency rates than household loans, making them more difficult for banks to manage.

According to the Financial Supervisory Service, as of September, the delinquency rate for corporate loans at domestic banks was 0.61%, much higher than the 0.39% for household loans. In particular, the delinquency rate for SME loans reached 0.75%. The SME delinquency rate has been rising annually, from 0.49% in September 2023 to 0.65% last year and 0.75% this year. It has been pointed out that as the economy deteriorates, delinquency rates are increasing, especially among SMEs.

Banks Must Also Manage Non-Performing Loans, Including Shell Loans

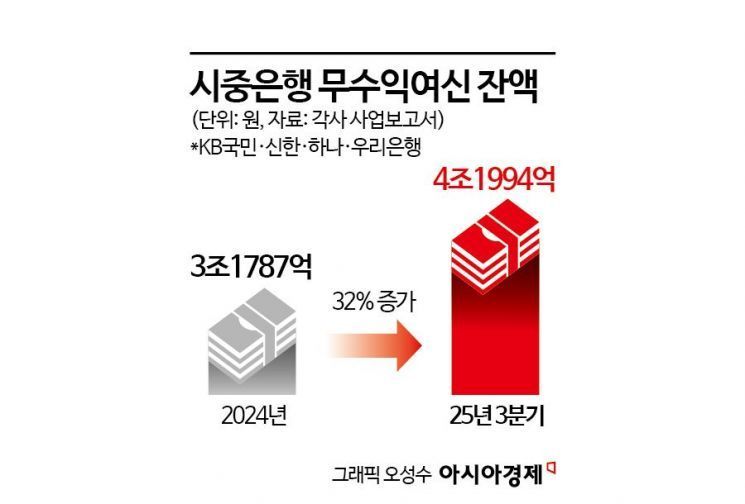

As corporate loans rapidly increase, "non-performing loans" are also rising quickly. The outstanding balance of non-performing loans-loans from which banks cannot even collect interest-increased by about 1 trillion won over the past nine months. As of the third quarter of this year, the non-performing loan balance at the four major banks (excluding Nonghyup Bank) stood at 4.1994 trillion won, a sharp increase of 1.0207 trillion won from the end of last year (3.1787 trillion won). This far exceeds the annual increases of 475.3 billion won in 2023 and 426.2 billion won in 2024.

Non-performing loans refer to loans where banks cannot collect even interest from borrowers. This includes loans that have been delinquent for more than three months, as well as loans under court receivership or bankruptcy, for which no interest income is generated. Since neither principal nor interest can be recovered, banks treat these as even more problematic than substandard loans-so-called "shell loans," which are regarded as malignant bad debts.

By bank, KB Kookmin Bank had the largest balance and increase, with 1.2668 trillion won in non-performing loans as of the third quarter, up 343.7 billion won. Hana Bank also exceeded 1 trillion won, with its balance rising by 139.6 billion won over nine months to reach 1.1305 trillion won. Shinhan Bank and Woori Bank followed with balances of 983.2 billion won and 818.9 billion won, respectively.

While both corporate and household non-performing loans increased, the growth was particularly pronounced among corporations. At KB Kookmin Bank, 76% (262.1 billion won) of the increase came from corporate loans. At Hana Bank, 127.7 billion won (91%) of the total 139.6 billion won increase was from corporate loans. For both KB Kookmin Bank and Hana Bank, the proportion of non-performing loans out of total loans expanded to 0.31%.

Given the pace of growth in corporate loans, the outstanding balance of non-performing loans could increase further by the end of this year. A financial sector official stated, "The increase in corporate insolvencies is due to challenging internal and external business conditions," adding, "As productive finance becomes more prominent next year, managing banks' bad loans could become a new challenge."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}