Bank of Korea Releases "Household Credit (Provisional) for Q3 2025"

Q3 Balance Hits Record High at 1,968.3 Trillion Won

Growth Slows from 25.1 Trillion to 14.9 Trillion Won

"Mortgage Loan Growth May Slow Further in Q4... Difficult to Predict Stock Investment Trends"

Household credit (debt) in South Korea has once again reached an all-time high. However, due to the government's stringent regulations, the growth of mortgage loans has slowed, and unsecured loans have shifted to a decline. There are expectations that mortgage loans will continue to remain stable in the fourth quarter as a result of the government's strong household loan regulations.

Minsu Kim, Head of the Financial Statistics Team at the Economic Statistics Division 1, Bank of Korea, is explaining the main features of household credit (provisional) for the third quarter of 2025 at the Bank of Korea in Jung-gu, Seoul on the morning of the 18th. Photo by Bank of Korea

Minsu Kim, Head of the Financial Statistics Team at the Economic Statistics Division 1, Bank of Korea, is explaining the main features of household credit (provisional) for the third quarter of 2025 at the Bank of Korea in Jung-gu, Seoul on the morning of the 18th. Photo by Bank of Korea

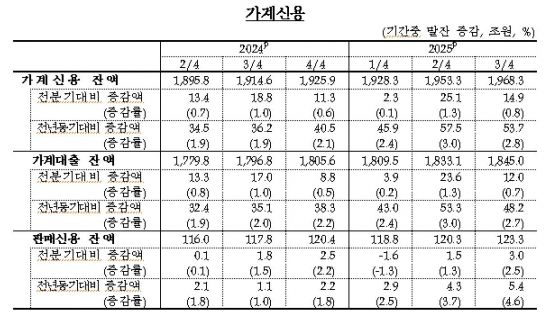

According to the "Household Credit (Provisional) for the Third Quarter of 2025" announced by the Bank of Korea on the 18th, the balance of household credit at the end of the third quarter this year stood at 1,968.3 trillion won. This is an increase of 14.9 trillion won compared to the previous quarter, marking the highest level since related statistics began to be published. However, the growth was smaller than in the previous quarter, when it had increased by 25.1 trillion won.

Household credit refers to comprehensive household debt, which includes loans received by households from banks, insurance companies, private lenders, and public financial institutions, as well as credit card spending (sales credit) before settlement.

Household credit in South Korea has continued to increase for six consecutive quarters since it turned to growth in the second quarter of last year, when it rose by 13.4 trillion won from the previous quarter. Although the increase in the third quarter of this year was smaller than in the second quarter of this year, which was the largest since the third quarter of 2021, it was still greater than in the fourth quarter of last year (11.3 trillion won) and the first quarter of this year (2.3 trillion won).

The balance of household loans, excluding credit card payments (sales credit), was 1,845 trillion won, up 12 trillion won from the previous quarter. The growth was smaller than in the second quarter, when it had increased by 23.6 trillion won.

Among household loans, the balance of mortgage loans was 1,159.6 trillion won, up 11.6 trillion won from the previous quarter. Other loans, such as unsecured loans, increased by only 300 billion won during the same period. Minsu Kim, Head of the Financial Statistics Team at the Economic Statistics Division 1 of the Bank of Korea, explained, "Due to the government's June 27 household debt management measures and other factors, the growth of mortgage loans has slowed, and unsecured loans have shifted to a decline."

By lending channel, the balance of household loans at deposit banks was 1,003.8 trillion won, up 10.1 trillion won from the previous quarter. Mortgage loans increased by 10.9 trillion won, while other loans, including unsecured loans, decreased by 800 billion won.

The balance of household loans at non-bank depository institutions, such as mutual finance companies, mutual savings banks, and credit unions, was 316.2 trillion won, up 2 trillion won from the previous quarter.

The balance of household loans at other financial institutions, such as securities companies, insurance companies, and asset securitization companies, was 525 trillion won, down 1 trillion won from the previous quarter. Kim stated, "While the amount of credit extended by securities companies expanded in the second quarter, the growth slowed in the third quarter."

The balance of sales credit (credit card payments) within household credit in the third quarter was 123.3 trillion won. This is an increase of 3 trillion won from the previous quarter, attributed to the recovery in private consumption due to increased credit card use during the holiday season and higher demand for local tax payments.

As of the end of the third quarter, policy loans from the Korea Housing Finance Corporation and the Housing and Urban Fund totaled 333.0379 trillion won, accounting for 28.7% of total mortgage loans.

The Bank of Korea expects that the pace of mortgage loan growth could further slow in the fourth quarter. Kim commented, "Due to the June 27 measures, the loan limit was capped at 600 million won, and the October 15 measures further reduced the limit, so the stable trend is likely to continue." Regarding the amount of credit extended by securities companies, which is often perceived as "stock investment on borrowed money," he said, "Although the growth slowed in the third quarter, it is currently difficult to predict future trends."

The Bank of Korea assessed that the household debt-to-nominal GDP ratio may decline in the third quarter. Kim explained, "Given that real GDP, which is included in nominal GDP, rose by 1.7% in the third quarter and the pace of household credit growth also slowed, there is a possibility that the household debt ratio will decline in the third quarter."

He further addressed concerns that instability in the housing market persists despite the decline in the household debt ratio, stating, "The household debt ratio has been stabilizing downward for three consecutive years. It is significant that the ratio of household debt is decreasing relative to the pace of economic growth from a macro and aggregate perspective," adding, "We must remain vigilant and respond appropriately to any future developments."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}