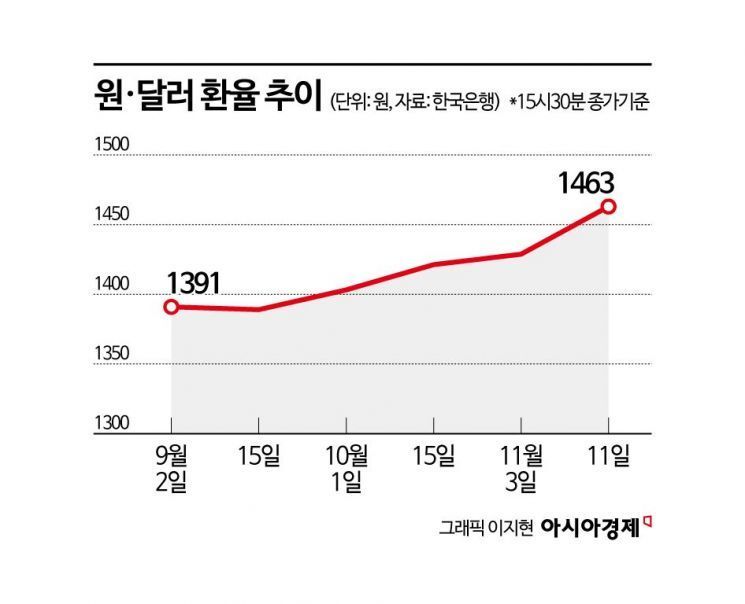

Won-dollar exchange rate surges over 70 won in two months

Bank capital ratios expected to decline as exchange rate rises

Expansion of corporate lending for productive finance also weighs on soundness

On the 12th, when the won/dollar exchange rate continued to fluctuate, the status board in the dealing room of Hana Bank in Jung-gu, Seoul displayed the won/dollar exchange rate, KOSPI, and others. 2025. 11.12 Photo by Cho Yongjun

On the 12th, when the won/dollar exchange rate continued to fluctuate, the status board in the dealing room of Hana Bank in Jung-gu, Seoul displayed the won/dollar exchange rate, KOSPI, and others. 2025. 11.12 Photo by Cho Yongjun

As the won-dollar exchange rate continues its sharp upward trend, banks are now on high alert to manage their financial soundness. With banks already expanding corporate lending and taking on additional financial burdens to promote productive finance, the recent surge in the exchange rate has raised concerns that the Common Equity Tier 1 (CET1) ratio-a key indicator of financial soundness for major financial holding companies-could decline.

Won-dollar exchange rate surges by over 70 won in two months, putting pressure on banks' soundness

According to the financial markets on November 13, the won-dollar exchange rate, which stood in the 1,380 won range in mid-September, has surged by more than 70 won in just two months, closing at 1,465.7 won as of the previous day's weekly trading session. During intraday trading the previous day, it reached 1,470 won, marking the highest level in seven months since April 9.

The surge in the exchange rate is attributed to a combination of factors, including increased volatility in the U.S. stock market, a rise in domestic investors' U.S. stock investments, and the strengthening of the dollar. Lee Changyong, Governor of the Bank of Korea, mentioned in a foreign media interview the previous day that volatility in U.S. AI-related stock prices, the U.S. government shutdown, the strong dollar, and policy uncertainty in Japan are all factors contributing to the weakening of the Korean won.

The sharp rise in the exchange rate is a factor that lowers banks' CET1 ratios. CET1 is calculated by dividing common equity by risk-weighted assets (RWA). When the exchange rate rises, the won-denominated value of banks' RWAs increases, resulting in a lower CET1 ratio. It is known that if the exchange rate rises by 100 won, the CET1 ratio can arithmetically fall by up to 0.3 percentage points.

Last year, when the exchange rate soared at the end of the year due to the state of emergency, major financial holding companies also saw a sharp drop in their CET1 ratios. For example, KB Financial Group's CET1 fell by 0.34 percentage points from 13.85% in the third quarter of last year to 13.51% at year-end, while Shinhan Financial Group's CET1 dropped by 0.1 percentage points from 13.13% to 13.03% over the same period. Both financial authorities and financial holding companies use a CET1 ratio of 13% as the benchmark for shareholder returns, so concerns arose at the time that a lower ratio could undermine value-up (corporate value enhancement) policies. As of the third quarter of this year, the CET1 ratios for major financial holding companies were: KB Financial Group at 13.83%, Shinhan Financial Group at 13.56%, Hana Financial Group at 13.30%, Woori Financial Group at 12.92%, and NH Nonghyup Financial Group at 12.34%. There are projections that these figures could decline in the fourth quarter.

Expansion of corporate lending also adds to soundness concerns

Banks' efforts to boost productive finance by increasing corporate lending are also weighing on their financial soundness. According to the financial sector, the outstanding balance of small and medium-sized enterprise loans at the five major banks stood at 675.8371 trillion won at the end of last month, up 4.7495 trillion won from the previous month. Compared to the increase of 1.876 trillion won in the first half of this year, the growth rate has surged 6.5 times in just four months.

Banks are reducing mortgage lending and expanding corporate lending in line with the government's push for productive finance. However, corporate loans carry a higher risk of default compared to mortgage loans, which puts additional pressure on banks' soundness. Capital contributions to funds such as the National Growth Fund to promote productive finance are also expected to be a financial burden. Choi Jungwook, a researcher at Hana Securities, explained, "For loans to key growth industries under productive finance, corporate lending is expected to increase by about 6-7% annually. While a weakening of the capital ratio is inevitable, the decline is not expected to be as severe as feared." Choi also analyzed, "The downward pressure on CET1 due to the creation of internal investment funds, such as the National Growth Fund and private funds, is estimated to be about 20 basis points (1bp=0.01 percentage points) per year."

Some experts point out that banks, which are pursuing financial stability, now face a dilemma as they are exposed to external variables such as the expansion of productive finance and the sharp rise in the exchange rate. Kim Youngdo, Head of Banking Research at the Korea Institute of Finance, stated, "As the shift toward full-fledged productive finance accelerates, balancing the expansion of corporate lending with maintaining financial stability has become a top priority. While demand for corporate loans is expected to rise, aggressively expanding productive finance will force banks to also ensure appropriate delinquency rates and capital ratios, creating a dilemma."

Kim added, "For bank capital adequacy, the minimum RWA regulation is set to rise from 60% this year to 65% starting in early 2026, which will further intensify downward pressure on capital ratios. If slow economic recovery and restructuring in certain industries overlap, it may become difficult for domestic banks to maintain their current level of soundness."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}