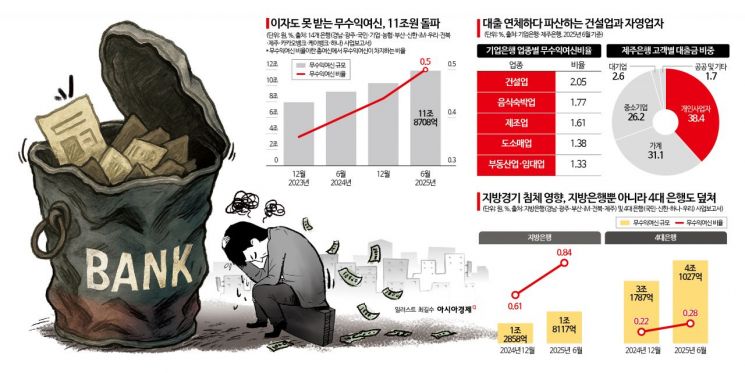

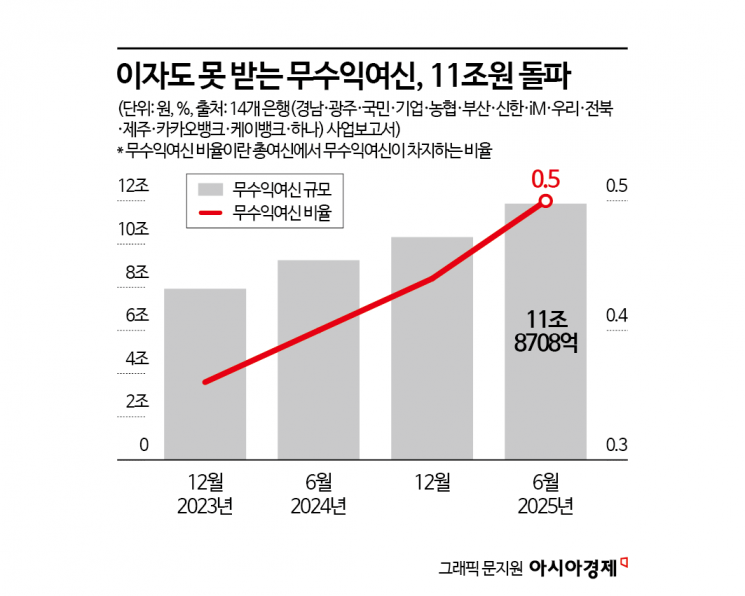

Total Non-Performing Loans at 14 Banks Exceed 11 Trillion Won as of June

Growth Accelerates Sharply

Not Only Regional Banks, But Major Banks Also See Steep Increases

Slump in Construction and Self-Employed Sectors Drives Trend

Delinque

The total amount of so-called "shell loans"-loans from major banks where neither principal nor interest is being repaid-has surpassed 11 trillion won. Notably, in the first half of this year, the growth rate of these shell loans was even steeper than the overall increase in lending. The main reason cited is the rising number of bankruptcies among construction companies and self-employed individuals who have failed to repay their loans on time.

While total loans remain flat, only non-performing loans are increasing... From regional banks to the four major banks, all are seeing record-high growth

As of June 2025, the non-performing loans of 14 banks-including the four major banks (KB Kookmin, Shinhan, Hana, Woori), specialized banks (NH Nonghyup, IBK Industrial Bank), regional banks (Busan, Kyongnam, iM, Jeonbuk, Gwangju, Jeju), and internet banks (KakaoBank, K-Bank)-totaled 11.8708 trillion won, based on semiannual data since December 2023. The ratio of non-performing loans to total loans also rose to 0.5%. The volume of non-performing loans, which had already exceeded 10 trillion won at the end of December 2024 (10.3215 trillion won), continued its steep upward trend. From the end of last year to June 2025, non-performing loans increased by 15%, which is slightly lower than the 16.7% increase from June to December 2023. However, considering that total loans grew by only 1.76% in June 2025 (compared to a 4.31% increase in the previous period), the growth of non-performing loans reached a record high. In other words, while the total loan volume stagnated, only non-performing loans continued to rise.

Non-performing loans refer to loans where neither principal nor interest is being collected. This figure is calculated by adding loans with more than three months of overdue principal payments to loans where interest is no longer being accrued, and it mainly includes loans to bankrupt companies. Because no interest income is generated, these loans are considered more problematic than substandard loans and are commonly referred to as "shell loans." Substandard loans are defined as loans that have been overdue for more than three months and are difficult to recover.

The increase in non-performing loans was led by regional banks and the four major banks. The non-performing loans held by regional banks rose by 525.9 billion won from the end of December 2024, reaching 1.8117 trillion won-a 41% increase. This is 24 percentage points higher than the 17% growth seen in June 2024 and 13.7 percentage points higher than the 27.3% growth at the end of December 2024. As of June 2025, the non-performing loans of the four major banks totaled 4.1027 trillion won, up 29% from the end of last year. This represents the steepest increase among banks, especially considering that the growth rates were only 7% in June 2024 and 7.9% in December 2024. Woori Bank saw the highest increase among the four major banks at 42%, followed by Shinhan (41%), KB Kookmin (33%), and Hana (10%).

Construction companies and self-employed individuals: Delinquency leads to business closure and bankruptcy

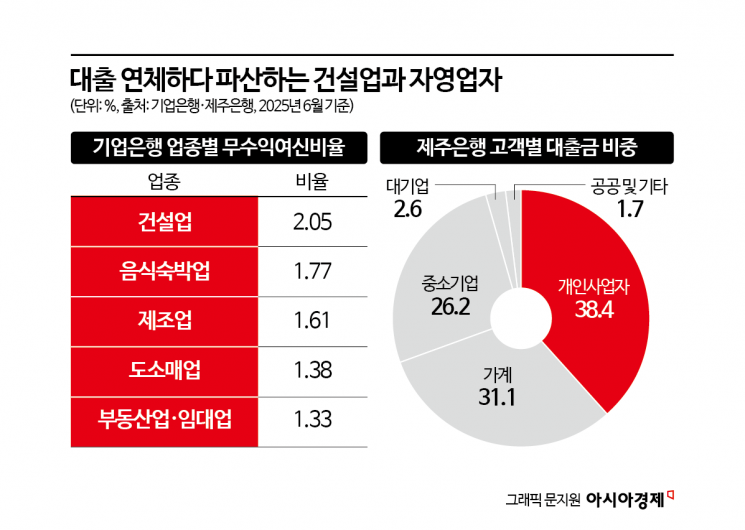

The main reason for the surge in non-performing loans is the sluggish domestic economy, which has led to more companies falling behind on their payments. This trend is particularly pronounced among construction businesses and self-employed individuals. This can be seen in the non-performing loan ratios of Jeju Bank (1.69%) and IBK Industrial Bank (1.37%), which are the highest among the 14 banks. Jeju Bank's loan portfolio is characterized by a high proportion of loans to industries with many self-employed individuals (wholesale/retail, food, and accommodation), accounting for 41% of its total won-denominated loans, and loans to individual business owners make up the largest share (38.4%) of its customer loans. IBK Industrial Bank, with a 24.4% market share in SME lending, has a significantly higher proportion of loans to small businesses compared to other banks.

As of June 2025, IBK Industrial Bank's non-performing loan ratio by sector was highest in construction at 2.05%, followed by food and accommodation at 1.77%. In terms of delinquency rates, food and accommodation ranked first at 1.8%, followed by construction at 1.34%. Jeju Bank's overall delinquency rate as of June 2025 was 1.68%, with the corporate loan delinquency rate at 1.73%, higher than the household loan delinquency rate of 1.41%.

Companies are facing the "double blow" of repeated delinquencies leading to business closure and bankruptcy. According to the National Tax Service's "Status of Business Openings and Closures," there were 60,700 business closures in June 2025. Of these, 43% were in retail (18,000) and food service (11,000). From January to July 2025, there were 309 closure reports from general construction companies (according to the Ministry of Land, Infrastructure and Transport), a 4.74% increase compared to 295 cases during the same period last year. According to the Court Statistics Monthly Report, the number of corporate bankruptcy filings submitted to the courts on a semiannual basis from June 2023 to June 2025 reached an all-time high of 1,104 cases in June 2025, continuing a steady increase since 724 cases in June 2023.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}