Financial Supervisory Service Discloses Major Dispute Cases on Dental Insurance Compensation

Check Exemption Periods and Coverage Details for Each Policy

Choi, who had a tooth that was loose for some time, pulled it out himself at home. He later visited a dental clinic and received implant treatment. He filed an insurance claim for the implant treatment under his dental insurance policy, but the claim was denied. This is because insurance benefits cannot be paid if dental treatment is received after self-extraction of a tooth.

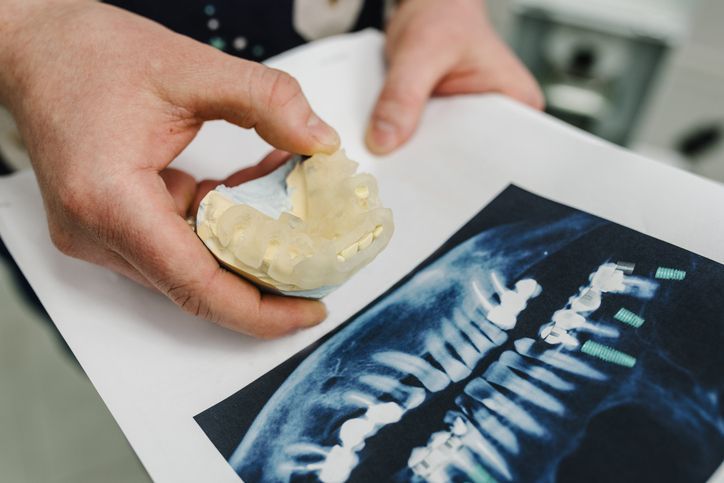

A case was revealed where five permanent teeth were extracted during the treatment of gum disease, but insurance benefits were paid for only three teeth. Getty Images

A case was revealed where five permanent teeth were extracted during the treatment of gum disease, but insurance benefits were paid for only three teeth. Getty Images

The Financial Supervisory Service disclosed major dispute cases related to dental insurance compensation on June 24.

Dental diseases such as cavities and gum disease are common conditions experienced by most people. As expensive treatments like implants have become more widespread, the financial burden of dental care on the public has increased, and demand for dental insurance as a safeguard continues to rise.

Dental insurance policies differ in terms of coverage scope and waiting periods depending on the product, and there may be limitations on insurance payouts or periods where benefits are reduced (by 50%), so policyholders need to exercise caution.

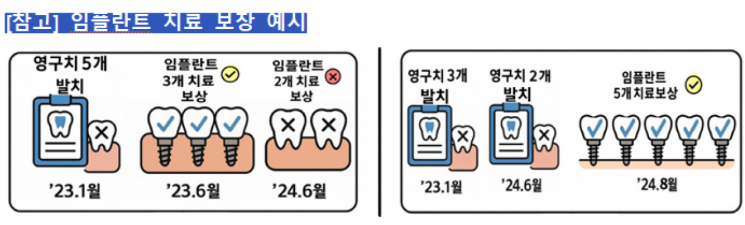

In January 2023, Park had five permanent teeth extracted during the treatment of severe gum disease. In June of the same year, implant treatment was performed on three of these teeth, which had less alveolar bone damage. For the remaining two teeth, implant treatment was performed in June 2024, and an insurance claim was filed. The insurance company only covers up to three permanent teeth per year for implant treatment, based on the number of extracted permanent teeth. As a result, insurance benefits were paid for only three out of the five teeth that received implant treatment.

The annual coverage limit for prosthetic treatments (bridges and implants) is determined by the number of extracted permanent teeth, not the number of teeth treated. Even for the same type of treatment, the annual coverage limit may differ depending on the insurance product. It is important to carefully compare and check the details when enrolling in dental insurance.

Kim, who had dental insurance that covered tooth extraction treatment, experienced severe pain as a wisdom tooth erupted and had the wisdom tooth extracted at a dental clinic, then filed an insurance claim. However, the insurance company explained that wisdom teeth are not covered, so insurance benefits could not be paid. Lee was advised during a dental consultation that orthodontic treatment was necessary due to overlapping teeth and protruding front teeth. Lee then had two teeth extracted and filed an insurance claim, but the claim was denied.

Certain teeth, such as wisdom teeth, may be excluded from coverage for extraction treatment. It is essential to check the coverage scope in the policy terms and conditions. If teeth are extracted as part of orthodontic treatment, insurance benefits may not be paid, so caution is needed.

Han, who enjoyed eating sweets, enrolled in dental insurance to reduce the financial burden of cavity treatment. One month later, Han visited a dental clinic and received treatment for dental caries (cavities), then filed an insurance claim, but was not eligible to receive benefits.

Dental insurance policies may include waiting periods and benefit reduction periods to prevent claims for conditions such as cavities that existed before enrollment. If cavities are diagnosed and treated before the coverage start date, insurance benefits may not be paid. In the early period after coverage begins, only partial benefits may be paid. However, if a tooth is damaged due to an accident, the contract date may be considered the coverage start date, so the policy terms should be checked.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}