Secret Contracts with Private Equity Funds Scratching Companies' Itches

No Disclosure Obligation for 'Shareholder Agreements' Leads to Market Disruption

Need for Capital Market Players to Ensure Transaction Transparency and Investor Protection

Various forms of cooperation between companies and private equity funds (PEFs) are increasing. To protect management rights from activist funds or hostile mergers and acquisitions (M&A) attacks, mutual cooperation is being strengthened, and transactions to alleviate the burden of corporate succession are also on the rise. New contractual behaviors aimed at maximizing profitability during initial public offerings (IPOs) and delisting processes are also being observed. As cooperation between companies and PEFs manifests in diverse contractual forms in the capital market, there are calls for institutional support to ensure fairness and transparency. This is due to concerns that secret contracts between large-capital PEFs and companies could deteriorate into illegal or irregular practices exploiting legal blind spots.

Secret Meetings Between Companies and PEFs... Blind Spots Disrupting Minority Shareholders and Capital Markets

Domestic PEFs have experienced explosive growth over the past 20 years. Although still in the early stages compared to global PEFs with histories exceeding 100 years, the market size and operational aspects of general partners (GPs) have now reached a certain trajectory. In particular, in terms of scale, after two funds totaling 400 billion KRW were established at the end of 2004, the committed capital reached approximately 136.4 trillion KRW with 1,126 funds as of the end of 2023, marking rapid growth. As PEFs with such large financial power voluntarily take on the role of key players in the capital market and problem solvers for companies, secret contracts with PEFs have frequently begun to disrupt the capital market.

A representative case is the recently surfaced secret agreement between Bang Si-hyuk, chairman of HYBE, and PEFs. Chairman Bang entered into conditional contracts with three PEFs one to two years before HYBE’s IPO in 2020. The contract stipulated that an IPO would occur within a certain period, with about 30% of the investment profits going to the PEFs, but this contract was not disclosed during the listing process. The PEFs sold large amounts of shares from the first day of listing without lock-up restrictions, and Chairman Bang received about 400 billion KRW from these PEFs. HYBE’s stock price surged 160% intraday compared to the public offering price on the first day of listing, but the flood of PEF shares caused the stock price to halve within about a week from its peak. While general investors suffered losses, the PEFs and the largest shareholder gained enormous profits through secret contracts.

This incident has drawn criticism within the investment industry that secret contracts between PEFs and major shareholders infringed on the interests of general shareholders in the capital market. While diverse and creative contracts are allowed in the capital market, listed companies deciding on IPOs should have transparently disclosed such agreements to other shareholders and general investors. There are also criticisms that legal and institutional measures to protect investors were insufficient.

A senior official from the venture capital industry familiar with IPOs said, "The HYBE case is somewhat unusual even within the industry. Usually, if option (conditional) contracts are made, they are disclosed to other shareholders, so keeping it secret is morally problematic." The official added, "Also, the fact that profits generated from the option contract were diverted to the personal benefit of the major shareholder rather than the company’s profits is an issue. However, these matters are more moral and qualitative than legal or quantitative, making it ambiguous to assign responsibility."

A senior official from a domestic pension fund stated, "It is common to include various conditions when making contracts between shareholders, but whether investor protection was violated or if the public offering price was unfairly influenced is a matter that regulatory authorities should examine." However, the official added, "It seems more like a gray area that is annoying but difficult to punish rather than a clear regulatory violation."

Under the current system, there is no disclosure obligation for the contents of contracts between shareholders, which is pointed out as a system deficiency. A senior official from the PEF industry said, "The uncertainty caused by the non-disclosure of the HYBE shareholder contract caused psychological anxiety for many investors and affected the stock price decline after listing. As a result, profits that should have gone to general shareholders ended up with Bang Si-hyuk personally." He added, "The controversy caused by the non-disclosure of important information to investors can undermine market trust, and such institutional deficiencies are one cause of the 'Korea discount.'"

Regarding this, a Korea Exchange official said, "We are currently cooperating with the Financial Supervisory Service (FSS) to look into related issues." The FSS stated, "No decision has been made yet regarding an investigation."

PEFs as All-Purpose Problem Solvers for Management Rights Defense and Corporate Succession

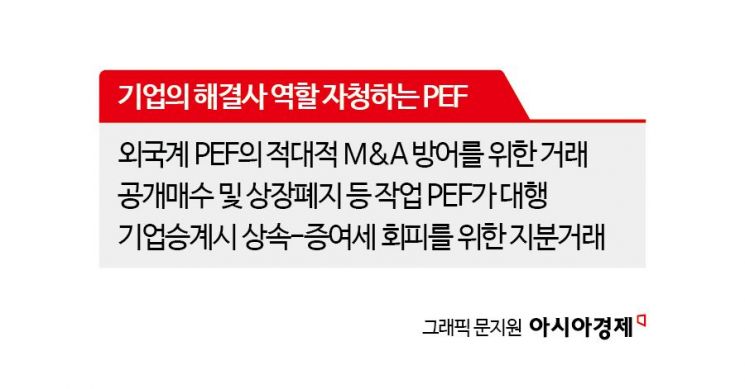

In terms of financial power, PEFs surpass banks and securities firms, but in terms of regulation, transactions between PEFs and companies are strongly protected as private contracts and are expected to increase further.

A senior official from the PEF industry said, "Although it might seem that relations between companies and funds would become strained after the management rights dispute between MBK and Korea Zinc, cooperation is actually increasing in more diverse forms. As more companies seek to proactively prepare against hostile foreign funds, the relationship between companies and domestic PEFs has become stronger," he hinted.

As the trend to convert listed companies into unlisted companies increases, companies have started to rely more on PEFs. The official said, "PEFs are preparing the groundwork for converting listed companies into unlisted companies through tender offers, and various transaction methods are emerging, such as receiving smart unlisted affiliates of the group in return."

Cooperation between PEFs and companies is also increasing in corporate succession. These transactions reduce inheritance and gift taxes incurred during succession without damaging corporate value.

For example, when the chairman of Company A passes Company B to his children, 60% of the shares are transferred to the son and daughter, and 40% to a PEF. They jointly hold shares and manage the company for about five years, increase corporate value, then sell and share the profits, thereby avoiding taxes.

Companies Face 'Liquidity Deterioration'... PEFs Gain Market Advantage

Experts predict that companies will face difficulties generating cash and liquidity shortages due to economic downturns, while funds will continue to flood into PEFs, creating a market dominated by PEFs for the time being. Accordingly, there are calls for regulatory authorities to monitor unfair trading and improve institutional frameworks.

Professor Lee Jun-seo of Dongguk University’s Department of Business Administration said, "Since a fund-dominant market rather than a company-dominant one has formed, it is time to carefully watch for unfair practices by PEFs during share acquisitions. Transparency and soundness are necessary throughout the entire process, including PEF tender offers and post-acquisition restructuring." Professor Kim Dae-jong of Sejong University’s Department of Business Administration said, "Cooperation between companies and PEFs should proceed in a way that develops the Korean capital market and promotes mutual growth."

With PEFs growing to a scale exceeding 100 trillion KRW and approaching 150 trillion KRW, there is advice to encourage them policy-wise to ensure transaction transparency commensurate with their capital size and to strive for investor protection. As the era of capital acquiring companies rather than inter-company transactions has arrived, the social role of PEFs, which have so far focused solely on the market’s venture capital function, is also expanding.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}