Financial Supervisory Service Chief Warns of 'Overheated Competition'; MBK Declares Preemptive Halt to 'Chicken Game'

Chairman Choi Yoon-beom's 'Price Increase' as Final Card, Buyback of Non-Voting Treasury Shares Poses 'Dilemma'

MBK Partners has announced the suspension of additional increases to the tender offer prices for Korea Zinc and Young Poong Precision. This is interpreted as a strategy that comprehensively considers the tender offer situation, profitability, and warnings from the Financial Supervisory Service. With attention focused on Chairman Choi Yoon-beom's response, the future management rights dispute is expected to shift from a 'price competition' to a 'vote battle.' Neither side has set a minimum purchase quantity condition, so they must buy even a single share if subscribed. Using the accumulated shares, they are likely to hold an extraordinary shareholders' meeting and engage in a vote battle. Chairman Choi's side still holds the 'price increase' card, giving them an advantage in the tender offer. However, since treasury shares have no voting rights, there is a possibility of the unusual phenomenon where they win the tender offer but lose at the shareholders' meeting.

MBK Declares 'Price Increase Suspension'... Did They Secure an Advantageous Position in the Tender Offer?

MBK's sudden declaration to suspend price increases is interpreted as a plan to secure an advantageous position in terms of purchase period and taxes in the tender offer, as well as to avoid the 'winner's curse' from perspectives such as profitability and corporate value deterioration.

MBK stated, "Regardless of whether Korea Zinc raises the tender offer price for acquiring treasury shares or whether Young Poong Precision raises the counter tender offer price, we will not further increase the tender offer prices for Korea Zinc and Young Poong Precision." In their statement, MBK cited that additional increases in tender offer prices would increase the company's financial burden and ultimately reduce corporate and shareholder value.

This decision by MBK came amid growing market concerns about the so-called 'winner's curse,' where expensive corporate acquisition costs ultimately damage the company. Especially, the strong warning remarks by Financial Supervisory Service Governor Lee Bok-hyun peaked concerns about overheated competition.

On the 8th, Governor Lee instructed an immediate investigation into unfair trading regarding Korea Zinc's tender offer at a Financial Supervisory Service executive meeting, pointing out that "excessive tender offer price competition that disregards long-term corporate value is highly likely to ultimately damage shareholder value." With MBK preemptively announcing no price increases, concerns over the tender offer escalating into a 'chicken game' have been temporarily alleviated.

Furthermore, since the minimum purchase quantity condition was removed, MBK, which will become a Korea Zinc shareholder later, has no practical benefit from further price increases. Internal reviews also concluded that MBK is in a favorable position regarding the second provisional injunction filed by Young Poong, which are cited as reasons behind MBK's bold move. This also exerts strong pressure on Chairman Choi's side, which is considering additional price increases, to join in 'abandoning price competition,' leveraging the Financial Supervisory Service Governor's remarks.

Some in the market analyze that although the stock purchase prices of the Young Poong-MBK alliance and Korea Zinc are the same, considering purchase periods and taxes, the Young Poong-MBK alliance has an advantage. While Korea Zinc's tender offer may be favorable for small investors, for large investors, the Young Poong-MBK alliance's tender offer could be more advantageous.

There is also ongoing speculation that investors seeking to eliminate uncertainty may side with the Young Poong-MBK alliance, whose tender offer period ends earlier on the 14th.

Chairman Choi Yoon-beom Gains Initiative... The 'Dilemma' of Treasury Shares Having No Voting Rights

The initiative in the game has now shifted to Chairman Choi Yoon-beom of Korea Zinc. Chairman Choi has staked his life on defending management rights in this dispute, even providing some Korea Zinc shares as collateral to Bain Capital. This is why there is considerable speculation that Chairman Choi will use the 'additional tender offer price increase' card to acquire even one more share.

Attention is focused on whether Korea Zinc will change the tender offer prices for Korea Zinc and Young Poong Precision on the 11th or 14th, which are considered turning points in the share purchase price competition. Notably, the 11th is the last day Korea Zinc can change the tender offer prices for Korea Zinc and Young Poong Precision without extending the treasury share tender offer period, which ends on the 23rd.

Of course, from Chairman Choi's perspective, increasing financial burden by raising additional borrowings is a concern. Another dilemma is that even if Chairman Choi's side mobilizes up to 2.6 trillion KRW to acquire treasury shares up to 15.5%, these shares have no voting rights at the shareholders' meeting. For example, if MBK convenes an extraordinary shareholders' meeting to change the board and engages in a vote battle, treasury shares may be unable to exercise voting rights.

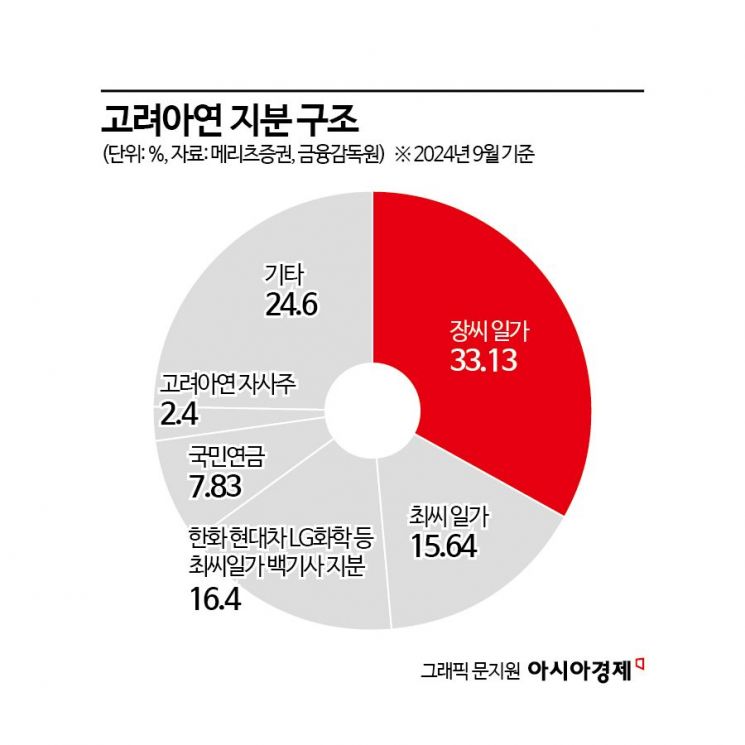

Especially since treasury shares are excluded from the denominator in shareholding calculations, the more treasury shares increase, the wider the gap in shareholding between the Young Poong-MBK side and Chairman Choi's side becomes. Currently, Korea Zinc's shareholding structure is approximately: Jang family 33.13%, Choi family 15.64%, Choi family's white knight shareholders such as Hanwha, Hyundai Motor, LG Chem 16.4%, National Pension Service 7.83%, Korea Zinc treasury shares 2.4%, and other shareholders 24.6%.

If Korea Zinc exchanges the treasury shares acquired through the tender offer with friendly shares instead of canceling them, voting rights would be restored. However, since they have announced a plan to cancel all tendered treasury shares, this card is no longer usable.

Meanwhile, Korea Zinc emphasized the legitimacy and necessity of defending management rights. Korea Zinc stated, "We will do our best to enhance shareholder value by completing the tender offer and cancellation of treasury shares," adding, "This is the only best way to minimize capital market turmoil such as stock price instability and to stabilize the market and protect investors after this situation ends."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}