Idle funds in the market are wandering aimlessly. Although the stock and real estate markets are cooling due to the delayed-than-expected interest rate cuts by the U.S. Federal Reserve (Fed), deposit products such as savings and time deposits are also losing their appeal as market interest rates decline. Financial consumers appear to be 'still in motion amid stillness' amid the uncertain market situation.

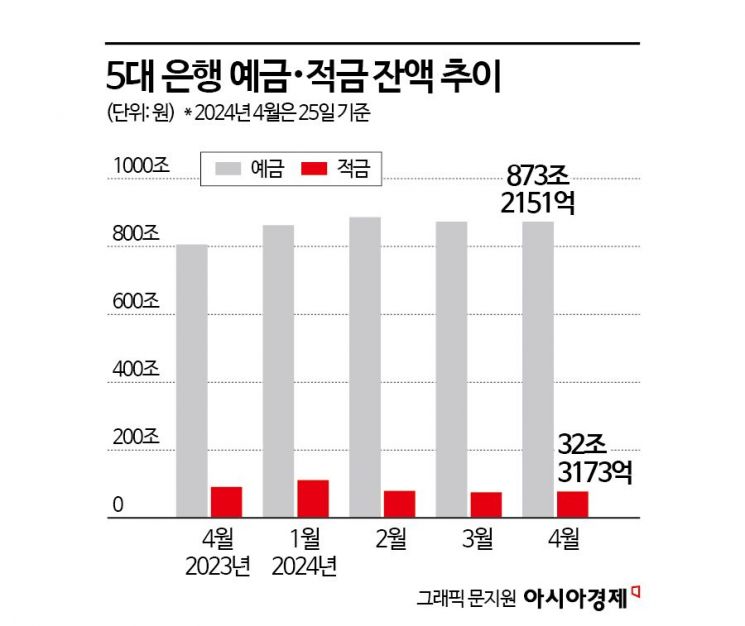

According to the financial sector on the 30th, the balance of regular savings and time deposits at the five major commercial banks (KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup) as of the 25th was 905.5324 trillion won. This represents a 0.09% (7.836 billion won) increase compared to the end of the previous month (904.7488 trillion won), indicating a stable 'sideways trend' with little change.

Breaking down savings and time deposits, regular time deposits stood at 873.2151 trillion won, showing a slight decrease of 0.02% (1.61 billion won) compared to the previous month (873.3761 trillion won), while regular savings increased by 3.01% (9.446 billion won) to 32.3173 trillion won, leading to a marginal increase. Despite the 12-month maturity time deposit interest rates at the five major banks remaining around 3.50?3.55% and savings rates around 3?4%, they managed to maintain the status quo.

Other investment asset markets are cooling rapidly. Investor deposit funds, known as funds waiting to enter the stock market, also reversed course. According to the Korea Financial Investment Association, investor deposit funds stood at 55.6712 trillion won as of the 25th, down 6.64% (3.9586 trillion won) from the beginning of the month (59.6298 trillion won). The balance of credit transaction loans also fell by 2.39% (466.9 billion won) to 19.0653 trillion won from 19.5322 trillion won at the start of the month. The real estate market is similar. According to the weekly apartment price trend recently released by the Korea Real Estate Board, nationwide apartment prices fell by 0.02% as of the 22nd.

Most Idle Funds Parked in 'Parking Accounts'... Due to Delayed Expected Interest Rate Cuts

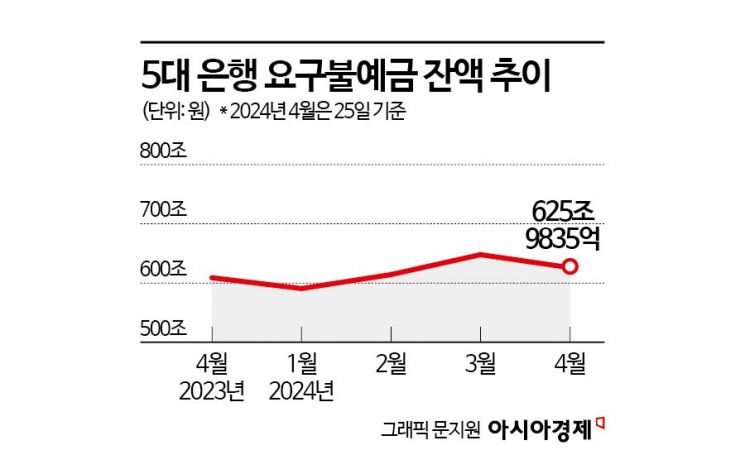

It appears that most idle funds are still tied up in bank demand deposit accounts (commonly called 'parking accounts'). Although the balance of demand deposits, including market rate-based demand deposit accounts (MMDA) at the five major commercial banks, was 625.9835 trillion won, down 21.9407 trillion won (3.38%) from the previous month, this is largely interpreted as a seasonal illusion.

An official from a commercial bank said, "The decrease in demand deposits this month is largely due to MMDA. MMDA, mainly used by large corporations, often decreases in March and April when dividends are concentrated, so this is not unusual," adding, "A significant portion of idle funds still remains in demand deposits."

In fact, the demand deposit balance (about 625 trillion won) as of the 25th is about 16 trillion won higher than in April 2023 (about 609 trillion won) a year ago. Compared to the end of January this year (about 590 trillion won), it is about 35 trillion won higher. This is due to the concentration of funds amounting to 57 trillion won into demand deposits in February and March when expectations for interest rate cuts were still high.

The reason why idle funds in the market are showing a still-in-motion pattern is attributed to the uncertain economic situation. Initially, there was speculation that the Fed could cut interest rates at least 2?3 times within the year, raising financial consumers' expectations. However, the recent U.S. Consumer Price Index (CPI) increase rate in March was 3.5%, and retail sales growth was 0.7%, both exceeding market forecasts. There is even speculation inside and outside Wall Street that the Fed might raise the benchmark interest rate to control inflation rather than cut it.

To make matters worse, geopolitical issues such as military clashes between Iran and Israel have also flared up. Although both sides are restraining escalation, and Israel and the Palestinian armed group Hamas have begun ceasefire negotiations, the uncertainty has caused the U.S. 10-year Treasury yield to hover around 4.6% in the latter half of this month. A financial sector official said, "It is a time with many variables, so it is premature to be optimistic that interest rate cuts will naturally follow," adding, "It is necessary to approach any asset cautiously."

Banks Compete to Attract Parking Account Funds

Meanwhile, commercial banks are fiercely competing to capture standby funds. SC First Bank offers a special interest rate of up to 3.5% daily on balances for first-time customers who subscribe to a daily compound interest savings deposit (MMDA) of 30 million won or more, up to 2 billion won, until the 30th. The daily compound interest savings deposit is a demand deposit account that pays interest compounded daily based on the daily balance. The more deposits, the higher the interest rate, making it a popular parking account for high-net-worth individuals to freely deposit and withdraw money. The total recruitment limit is 100 billion won, and the event ends once the limit is reached.

Hana Bank recently introduced the 'Daldal Hana Account,' a payroll account offering up to 3% annual interest for transferring salaries of 500,000 won or more. The basic interest rate is 0.1% per annum, with an additional preferential interest rate of 1.9 percentage points up to a limit of 2 million won if salary transfer conditions are met, plus a special event bonus of 1.0 percentage point for one year. Considering that typical demand deposit accounts offer 0.1% interest, this is a significant benefit.

IBK Industrial Bank's 'IBK Small and Medium Enterprise Worker Payroll Parking Account' offers up to 3.0% annual interest to SME employees, and KB Kookmin Bank provides up to 1.6% annual interest to salary transfer customers through the 'KB My Fit Account.' Shinhan Bank also launched a parking account targeting people in their 20s with an interest rate of up to 3%. Shinhan Bank's 'Hey Young Money Box' offers a basic interest rate of 0.1%, plus a preferential interest rate of 2.9 percentage points for depositors aged 18 to 29.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}