Shinhan Bank Raises Mortgage Loan Rates Starting Today

"Adjusting Household Debt Growth Speed"

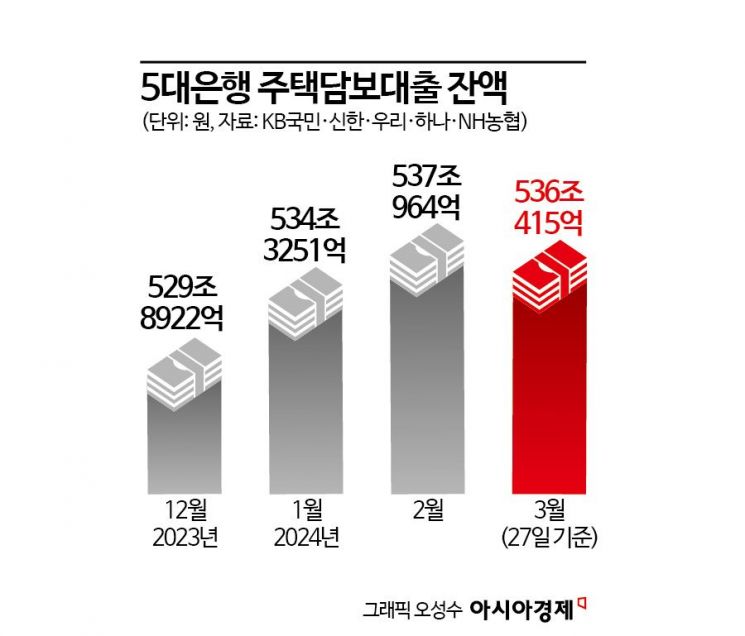

Mortgage and Household Loan Balances

Turn Negative for the First Time in 11 Months

Major commercial banks are raising mortgage loan interest rates. Due to the rise in interest rates and financial authorities' policies, the outstanding balance of mortgage loans has turned to a declining trend. This is the first time since April last year that both the outstanding balance of mortgage loans and household loans have decreased on a monthly basis.

Shinhan Bank raised mortgage loan interest rates by 0.1 to 0.3 percentage points on the 1st. A Shinhan Bank official said, "This is to control the speed of household debt and manage stabilization." The interest rate for new purchase funds within mortgage loans increased by 0.15 percentage points, and the interest rate for living stabilization funds rose by 0.1 percentage points. For mortgage refinancing, the interest rates based on 5-year and 6-month financial bonds increased by 0.04 and 0.3 percentage points respectively, and the COFIX (Cost of Funds Index) 6-month variable rate also rose by 0.2 percentage points.

KB Kookmin Bank raised mortgage loan interest rates by 0.23 percentage points annually in February, and Woori Bank also increased mortgage and jeonse loan interest rates by 0.1 to 0.3 percentage points from the end of March. As of this date, the variable mortgage loan interest rates (new COFIX basis) of the five major banks range from 3.9% to 6.868%, with the lower end dropping by 0.1 percentage points compared to early February (4.0% to 6.658%), but the upper end rising by 0.21 percentage points. Excluding NH Nonghyup Bank, both the upper and lower ends increased.

The reason banks have raised interest rates like this is that financial authorities have tightened household loans in the banking sector since the beginning of this year. Kim So-young, Vice Chairman of the Financial Services Commission, said at the household debt risk inspection meeting in February, "Considering the continued expectation of interest rate cuts within the year and the possibility of housing market recovery in the second half, household debt may increase significantly this year," urging banks to manage it. Recently, financial authorities have also held meetings with financial officers of major banks regarding household loans, urging restraint in mortgage loan competition and strengthening annual loan volume management. Accordingly, each bank is managing household loans by raising mortgage loan interest rates.

Due to these effects, the outstanding balance of mortgage loans has turned to a decline for the first time in 11 months. As of the 27th of last month, the outstanding balance of mortgage loans at the five major banks?Kookmin, Shinhan, Hana, Woori, and Nonghyup?was KRW 536.0415 trillion, down KRW 1.0549 trillion from the end of February (KRW 537.0964 trillion). As the mortgage loan balance decreased, the household loan balance also declined. The household loan balance of the five major banks was KRW 694.3047 trillion, down KRW 1.4875 trillion compared to the end of February.

The real estate market downturn also played a role. Apartment transaction volumes, which had been recovering this year, have also slowed. Last month, the number of apartment listings in Seoul approached 80,000, intensifying the inventory backlog. According to 'Asil,' a real estate big data company, the number of apartment listings in Seoul was 83,320 as of the 27th of last month, a 6.7% increase compared to the previous month. This is the first time in four months since November last year that Seoul apartment listings have exceeded 80,000.

The 'Stress Debt Service Ratio (DSR)' applied to mortgage loans since February 26 is also considered to have had an impact. DSR is the ratio of principal and interest repayment amount to annual income. Banks have traditionally provided loans as long as the DSR did not exceed 40%, but the stress DSR applies a certain level of stress interest rate (additional rate) reflecting the risk of future interest rate hikes. When interest rates rise, the increased principal and interest repayment burden is reflected, reducing the loan limit compared to before. A representative from a commercial bank said, "When interest rates rise, there is a psychological effect that reduces the outstanding balance of mortgage loans, and the ambiguous situation in the real estate market likely had a significant impact as well."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}