FSS "Accumulate Provisions Instead of Bonuses and Dividends"

Not Only Bonuses but Also Existing Wages Are Being Reduced

Union's Negotiation Power Weakens Ahead of Wage Agreement Talks

"Most of the annual salary is performance-based pay, and the expressions of the contract workers in the Investment Banking (IB) department are very gloomy."

This is a message from an employee of a small to medium-sized capital company. Ahead of the Lunar New Year holiday, when normally there would be excitement about bringing holiday rice cake money and performance bonuses to meet family, the atmosphere inside the company this year is colder than usual. This is because the Financial Supervisory Service (FSS) recently pressured the secondary financial sector to increase provisions for real estate project financing (PF) instead of paying performance bonuses.

Earlier this year, a certain capital company had a surplus when they conducted a preliminary settlement of last year's performance. However, the FSS recently demanded that they recognize 100% expected losses and set aside provisions for bridge loans that cannot be converted into main PF among real estate PFs. As a result, the company turned to a deficit. A representative of this capital company said, "IB employees at the manager level used to receive performance bonuses worth several hundred million won annually, but this time it is impossible due to the deficit," adding, "Even if the target performance by rank was achieved, many are disappointed because they cannot receive bonuses due to the additional provision issue."

Savings banks are in an even worse situation. Not only are performance bonuses out of the question, but there is even a sense that existing wages might be cut. One savings bank is expected to see an increased deficit last year due to the issue of additional provision accumulation. The problem is that with the expanding deficit, the union's bargaining power regarding wages and welfare in the upcoming labor-management collective bargaining negotiations will significantly weaken. A representative of this savings bank lamented, "Soon, we will have no choice but to choose between restructuring or wage cuts," and added, "Only financial workers are being sacrificed due to the financial authorities' risk management."

In some savings banks, there is also a sense of restructuring. JT Chin-Ae Savings Bank, a subsidiary of the Japanese comprehensive financial group J Trust Group, introduced a wage peak system as of the 1st of this month. While domestic financial companies did not move to adopt the wage peak system during the 2010s when it was popular, this time they decided to implement it suddenly. A representative of JT Chin-Ae Savings Bank said, "The sudden approval of the wage peak system last month has created an atmosphere among employees that restructuring or similar measures are imminent," adding, "Even Japan, where the retirement age is longer than in Korea, is in such a situation, which shows how bad things are."

Labor unions in the secondary financial sector, including capital companies and savings banks, have even taken collective action. The 'Joint Struggle Headquarters of Financial Workers,' composed of the National Office Financial Services Labor Union and the National Financial Industry Labor Union, held a press conference in front of the Financial Supervisory Service in Yeouido, Seoul, on the 7th. The Joint Struggle Headquarters stated, "The FSS governor, a former inspector, is threatening that if dividends and performance bonuses are paid instead of setting aside provisions, the asset soundness, asset management, internal control, and appropriateness of performance bonuses of the company will be thoroughly inspected and individual interviews will be conducted," calling it "FSS-driven administrative finance."

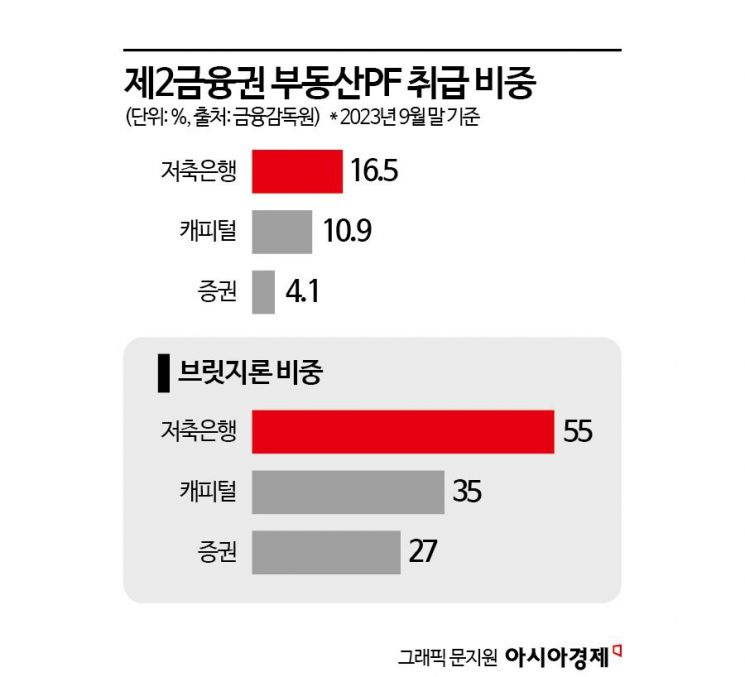

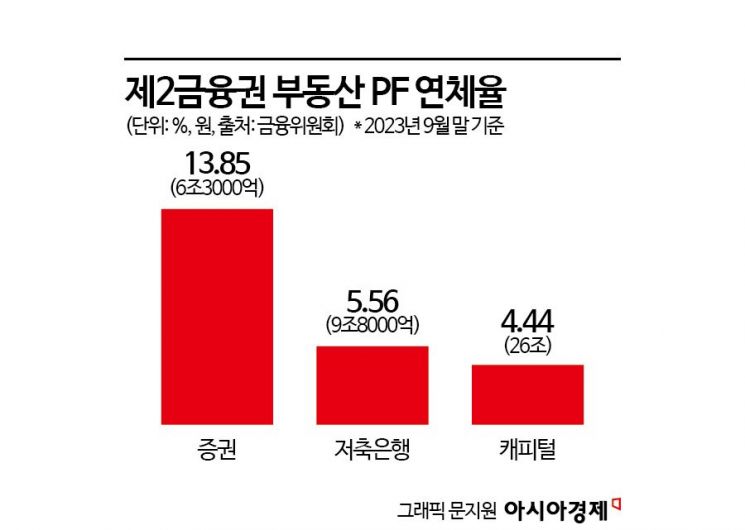

The FSS plans to increase pressure by conducting on-site inspections of the secondary financial sector after the Lunar New Year holiday to verify whether provisions were properly reflected in last year's settlement results. The inspection targets include eight savings banks, three capital companies, and the central associations of Nonghyup, Shinhan Credit Cooperative, and Suhyup. As of the third quarter of last year, the proportion of real estate PF handled relative to total assets in the savings bank sector was 16.5%, higher than other sectors such as capital companies (10.9%) and securities (4.1%). The proportion of bridge loans was also 55%, higher than securities (27%) and capital companies (35%). On the other hand, based on the proportion of real estate PF loans relative to equity capital during the same period, capital companies rated A or below had the highest risk at 150%. This was followed by savings banks (124%), AA-rated capital companies (92%), small to medium securities firms (41%), and large securities firms (36%). The delinquency rate for real estate PF is 5.56% for savings banks and 4.44% for capital companies. After the Lunar New Year holiday, there is a possibility that insolvent companies among savings banks and capital companies will surface.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}