Supply Scale Reduced but Benefits for Vulnerable Sectors Strengthened

From the 30th of this month, the Special BoGeumJaRi Loan will end, and a new BoGeumJaRi Loan will be launched. Although the supply scale will be significantly reduced to around 10±5 trillion KRW annually to manage household debt, benefits for vulnerable groups such as victims of jeonse fraud will be strengthened.

Additionally, financial authorities will undertake a major institutional reform, including changes to the role of the Korea Housing Finance Corporation (HF), to enable private financial companies to actively handle long-term mortgage loans by considering borrowers' repayment risks on their own.

The Financial Services Commission announced on the 25th that the newly revamped BoGeumJaRi Loan will be launched from the 30th. This follows the scheduled termination of the Special BoGeumJaRi Loan on the 29th.

The supply scale of the new BoGeumJaRi Loan will be based on 10 trillion KRW annually but will be flexibly adjusted by ±5 trillion KRW depending on market funding demand and other policy fund execution conditions. This scale is significantly reduced compared to the Special BoGeumJaRi Loan, which supplied about 43 trillion KRW as of the end of last year, and the existing BoGeumJaRi Loan, which typically supplied around 20 trillion KRW annually.

The Financial Services Commission stated, "We will manage policy mortgage supply within the principle of keeping the household debt growth rate within the nominal growth rate," and added, "Limited supply capacity will be managed to concentrate benefits on low-income and genuine demand households."

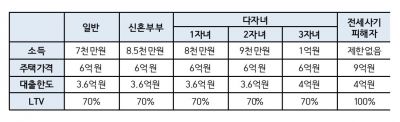

The supply targets for the BoGeumJaRi Loan are the same as those for the BoGeumJaRi Loan before the Special BoGeumJaRi Loan: combined annual household income of 70 million KRW or less, housing price of 600 million KRW or less, and either no home ownership or temporary two-home ownership conditional on disposing of the existing home.

Requirements for low-income, genuine demand, and vulnerable groups are significantly relaxed. The annual income limit is raised to 85 million KRW or less for newlyweds and ranges from 80 million KRW (one child) to 100 million KRW (three children) for multi-child families depending on the number of children. In particular, no separate income restrictions are imposed on victims of jeonse fraud, and the housing price limit is expanded to 900 million KRW or less.

The loan limit is up to 360 million KRW within a loan-to-value ratio (LTV) of 70% and a debt-to-income ratio (DTI) of 60%. In regulated areas, LTV of 60% and DTI of 50% apply. Multi-child families and victims of jeonse fraud can borrow up to 400 million KRW, and first-time homebuyers can borrow up to 420 million KRW.

The loan term will range from 10 to 50 years, but long-term mortgages of 40 years or more are targeted at young people. The 40-year term product is for those aged 39 or younger (49 or younger for newlyweds), and the 50-year term product is for those aged 34 or younger (39 or younger for newlyweds).

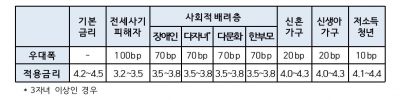

Interest rates will be applied at 4.2?4.5% annually, which is 30 basis points (bp) lower than the Special BoGeumJaRi Loan (preferential type). The preferential interest rate has increased by 20bp compared to before, with a maximum of 100bp applied. Victims of jeonse fraud receive the maximum 100bp, persons with disabilities, multi-child families (three or more children), multicultural families, and single-parent families receive 70bp, newlyweds and families with newborns receive 20bp, and low-income youth receive 10bp. Accordingly, vulnerable groups will receive interest rates in the 3% range. Victims of jeonse fraud will have rates of 3.2?3.5%, and persons with disabilities, multi-child families (three or more children), multicultural families, and single-parent families will have rates of 3.5?3.8%.

Additionally, prepayment penalties will be waived until early next year for socially considerate groups such as victims of jeonse fraud, persons with disabilities, multi-child families, and low-credit borrowers (below 804 points according to NICE). For general households, a fee of 0.7%, about half the level of commercial banks, will be applied.

A Financial Services Commission official said, "Unlike last year, with expectations of interest rate cuts within the year, it is an important time to take a balanced approach that strictly manages the pace of household debt increase while sufficiently supporting the necessary funds for low-income and genuine demand households," adding, "Even if the supply scale of BoGeumJaRi Loans is managed within a certain range for household debt management, we will ensure thorough operation so that sufficient support and benefits are provided to vulnerable groups in urgent need."

Meanwhile, authorities plan to stop supplying qualified loans and encourage private financial companies to supply long-term mortgage loans independently.

First, banks will be given institutional benefits to handle products where borrowers' repayment risks are safely managed. For mixed-type (fixed over 5 years, etc.), periodic, and pure fixed-rate products, additional interest rates will be relaxed when calculating the stress debt service ratio (DSR), and banks' deposit insurance premiums and contributions to the Korea Credit Guarantee Fund will be applied at lower levels than for variable-rate loans.

Related systems will also be reformed to indirectly support private long-term mortgage supply by utilizing the policy capacity of the Korea Housing Finance Corporation (HF) freed up due to the reduction in policy mortgage supply. Accordingly, a project to provide credit enhancement for covered bonds issued by commercial banks will be promptly promoted within the first quarter. Covered bonds are securitized bonds issued using mortgage loan receivables held by banks and other financial institutions as collateral and are used as a long-term funding method. Through credit enhancement by HF, private long-term mortgage products will be offered at competitive interest rates.

Furthermore, financial authorities plan to launch a "(tentative name) Covered Bond Re-securitization Organization" within the second quarter to support re-securitization so that covered bonds are supplied to the market with maturity structures and sizes desired by investors. They will also actively promote businesses such as swap banks that support interest rate swaps tailored to the needs of financial institutions facing difficulties in managing interest rate risks.

Tasks to revitalize covered bond issuance will continue. The current 1.0% loan-to-deposit ratio recognition limit for covered bonds will be raised, and procedural improvements and infrastructure expansion to reduce the burden of covered bond issuance on financial companies will be pursued.

A financial authority official said, "It is also a very important task to advance lending practices and methods by enabling private financial companies to closely manage borrowers' repayment burdens through changes in the role of HF," adding, "We will make policy efforts to improve the practice of financial companies excessively relying on policy institutions for long-term mortgage supply and create conditions for them to actively supply various long-term mortgage products that consider borrowers' repayment risks on their own."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}