Since 2021, Housing Price Adjustment

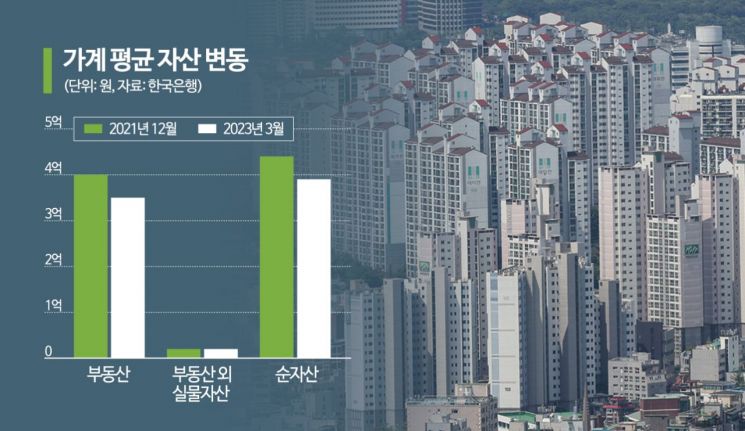

Average Household Net Assets Drop by 50 Million Won

Jeonse Price Decline, Increased Deposit Return Burden

Housing Price Slump Causes Surge in Unsold Houses

Construction Companies' Financial Soundness Deteriorates

A warning has been issued that if housing prices adjust sharply in the future, the size of household net assets could shrink, leading to a deterioration in financial soundness. It is pointed out that if the burden of returning jeonse deposits for landlords increases and the volume of unsold houses rises, causing profitability in the housing business to worsen, this could escalate into a real estate project financing (PF) insolvency crisis.

On the 21st, the Bank of Korea announced at the regular meeting of the Monetary Policy Committee that it had finalized the "June Financial Stability Report," which contains these details. According to estimates using last year's Household Financial Welfare Survey, the average household net assets decreased by 50 million KRW from 440 million KRW at the end of 2021 to 390 million KRW at the end of March this year due to the housing price adjustment continuing since the second half of 2021. During the same period, the proportion of high-risk households with weak repayment ability (relative to households holding financial debt) expanded from 2.7% to 5.0%. High-risk households are those whose debt service ratio (DSR) exceeds 40% and debt-to-asset ratio (DTA) exceeds 100%.

About 4.1~7.6% of Jeonse Rental Households Face Difficulty Returning Deposits

In particular, the burden of returning jeonse deposits for rental households has significantly increased due to the decline in jeonse prices. According to the Bank of Korea, if jeonse prices remain at the March level this year, the amount of deposit difference that rental households must return to tenants is estimated at 24.2 trillion KRW this year. This corresponds to about 8.4% of the total jeonse deposit amount expected to mature, which is 288.8 trillion KRW. Among the 1,167,000 jeonse rental households, approximately 4.1~7.6% are estimated to face difficulties in returning deposits even if they dispose of financial assets and take on additional loans.

The sluggish housing prices have also led to a rapid increase in unsold houses, especially in non-metropolitan areas such as Daegu, which is increasing financial stability risks. The increase in unsold houses can deteriorate the financial soundness of construction companies through increased housing inventory assets and accounts receivable. The average unsold housing inventory per construction company was 6.6 billion KRW last year and has recently increased again, while accounts receivable from sales and construction rose sharply by 34.1% year-on-year to 23.47 billion KRW. Kim In-gu, Director of the Financial Stability Department at the Bank of Korea, pointed out, "Looking at the period of rapid increase in unsold houses in 2007-2008, the risk of insolvency for construction companies significantly increased about three years after the rise in unsold houses," adding, "The recent surge in unsold houses could deteriorate the financial soundness of construction companies in the future."

The increase in unsold houses can also lead to defaults on real estate PF loans. As of the end of December last year, the delinquency rate and non-performing loan ratio for real estate PF loans were 1.19% and 1.25%, respectively, both rising since 2021. With public guarantees related to real estate significantly increasing since 2015 and their role expanding in the real estate market, if the financial soundness of major guarantee institutions deteriorates, related fiscal burdens could also increase. For example, the Korea Housing & Urban Guarantee Corporation's guarantee default amount increased from 800 billion KRW in 2021 to 1.6 trillion KRW last year, and the subrogation payment amount expanded from 600 billion KRW to 1.1 trillion KRW. The subrogation payment rate (subrogation payment amount/guarantee balance) also rose from 0.11% to 0.18%. Notably, the proportion of jeonse-related guarantees among subrogation payments increased significantly to 92.1% last year compared to 10.4% in 2017.

Director Kim said, "To prevent an expansion of defaults due to prolonged housing market sluggishness, it is necessary to prepare measures to ease regulations focused on actual demanders, adjust sale prices, and protect jeonse tenants facing risks of deposit non-return," adding, "Regarding real estate PF loans, support should be provided for smooth project progress for normal projects, while for risky projects, private and public financial institutions should prepare bad debt purchase programs to enable prompt restructuring if necessary."

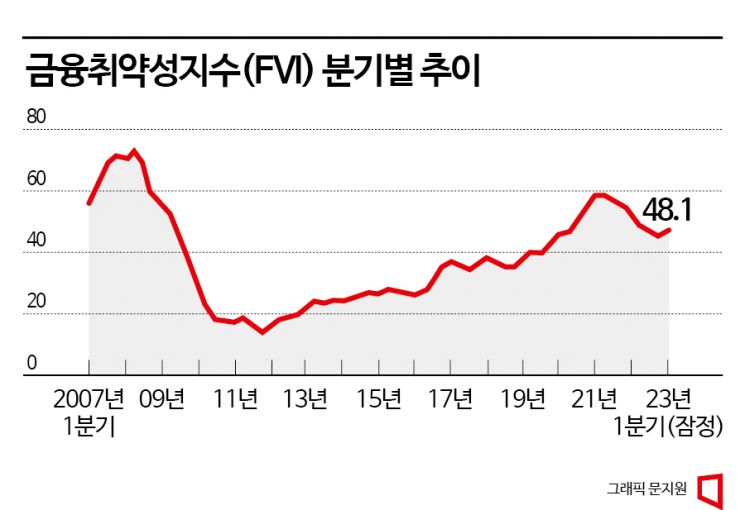

Financial Vulnerability Index (FVI) Turns Upward... Far Above Long-Term Average

Meanwhile, according to the Financial Stability Report, the Financial Vulnerability Index (FVI), which indicates medium- to long-term vulnerabilities within South Korea's financial system, turned to an upward trend this year, reflecting latent vulnerabilities. The FVI for the first quarter of this year was 48.1, rising from 46.0 in the fourth quarter of last year and significantly exceeding the long-term average (from Q1 2007 to Q1 2023) of 39.4. This index peaked at 59.4 in Q2 2021 and then showed a downward stabilization trend but switched to an upward trend in Q1 this year. The index is likely to rise further as household loans have returned to an increasing trend recently. On the other hand, the Financial Stress Index (FSI), which shows short-term volatility in financial market prices such as stocks, bonds, exchange rates, and credit default swap (CDS) premiums, was 17 as of May, falling back to the "caution" level after being close to the "crisis" threshold of 21.2 in February this year.

Lee Jong-ryeol, Deputy Governor of the Bank of Korea, emphasized, "Due to expectations of easing domestic and international monetary policy tightening this year, stock prices have risen and the decline in real estate prices has slowed, leading to an increase in household loans since April, which limits the reduction of financial imbalances," adding, "Going forward, policy authorities need to prepare preemptive and proactive response measures such as liquidity supply systems through policy coordination among related agencies to respond promptly to market instability, considering the high domestic and external uncertainties."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}