KOFIX Hits All-Time High Since 2010 Introduction

Time to Pay More Interest Than Principal Arrives

The Bank of Korea raised the base interest rate by 0.5 percentage points, and the real estate transaction market is expected to experience a prolonged winter. On the 13th, a red light was on at a traffic signal near an apartment in downtown Seoul.

The Bank of Korea raised the base interest rate by 0.5 percentage points, and the real estate transaction market is expected to experience a prolonged winter. On the 13th, a red light was on at a traffic signal near an apartment in downtown Seoul.

[Asia Economy Reporter Shim Nayoung] The COFIX, which serves as the basis for banks' variable interest rates on mortgage loans and jeonse deposit loans, has soared to an all-time high. As a result, the upper limit of variable interest rates on mortgage loans and jeonse deposit loans at commercial banks has exceeded 7%. Since COFIX (Cost of Funds Index), the benchmark for these rates, recorded its highest level since its introduction in 2010, approaching 4%, the shock has been fully passed on to market interest rates. The interest burden on "Yeongkkeul" borrowers and jeonse tenants is expected to snowball.

The Korea Federation of Banks announced on the 15th, through the 'COFIX as of October 2022' disclosure, that the COFIX based on new transactions last month rose by 0.58 percentage points from 3.40% in September to 3.98%. This is the highest level since COFIX disclosure began in 2010, and the largest increase ever. Last month, the Bank of Korea implemented a big step (a 0.50 percentage point hike in the base rate at once), which raised the interest rates on time deposits, and the rise in bank bond yields, driven by recent incidents such as the Legoland case, also led to the increase in COFIX.

Mortgage loan interest rates at commercial banks, which immediately reflected the COFIX changes, rose one after another. KB Kookmin Bank decided to raise its variable mortgage loan interest rates from the previous 5.18-6.58% per annum to 5.76-7.16% per annum starting from the 16th. The interest rates on jeonse deposit loans also increased from 5.24-6.64% to 5.82-7.22%. Woori Bank's variable mortgage loan interest rates rose from 5.74-6.54% to 6.32-7.12%, and NH Nonghyup Bank raised theirs from 5.09-6.19% to 5.67-6.77%.

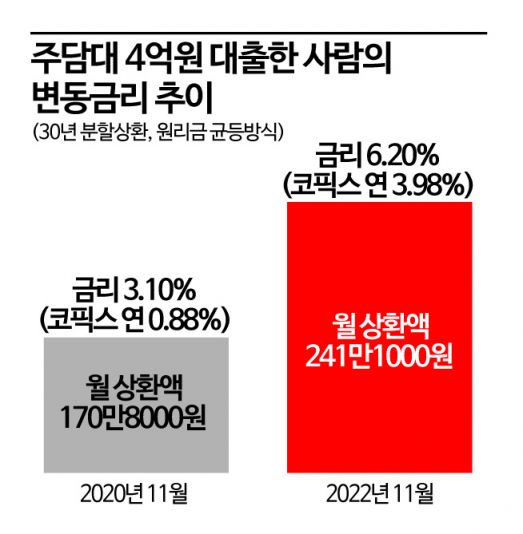

Office worker Cha Hyunju (43) is also deeply worried about the increasing interest burden. "It's been two years since I bought my house, but now the interest I have to pay each month is more than the principal," she said. "No matter how much I pay off, the repayment amount keeps increasing, so it feels like my blood is drying up."

When Cha bought an apartment in Namyangju, Gyeonggi Province two years ago, she took out a loan of 400 million won. At that time, her variable mortgage loan interest rate was 3.10%. The monthly repayment was about 1.7 million won (principal 1.1 million won + interest 600,000 won). The variable interest rate is recalculated every six months. Although the interest briefly dropped in 2021 when rates were at their lowest, since then, every time she received a text message from the bank notifying her of the interest rate, her heart would sink as the rates soared frighteningly.

Cha said, "The bank notified me this Wednesday that the loan interest rate has risen to 6.20%," adding, "My fixed monthly expenses going to the bank have reached 2.4 million won, and now that winter is coming, I wonder if I should live without even turning on the boiler. The future looks bleak."

If the Bank of Korea raises the base interest rate again on the 24th, loan interest rates are likely to approach 8%. When the base rate rises, bond yields increase, and mortgage fixed interest rates and credit loan rates, which use these as benchmark rates, also rise accordingly. The upper limits of fixed mortgage loan interest rates and credit loan rates at the five major banks have already far exceeded 7%.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}