91-Day CP Rate Surpasses 4%

Gangwon-do Refuses Debt Guarantee for Legoland ABCP

Institutional Investors Protest, Leading to Resolution

"A1 Rating Also Faces Growing Distrust"

[Asia Economy Reporter Hwang Yoon-joo] The debt default incident involving the Legoland real estate project financing (PF) asset-backed commercial paper (ABCP) has intensified liquidity tightening across the short-term funding and corporate bond markets. Amid aggressive interest rate hikes by the U.S. and South Korean central banks, a local government's refusal to guarantee payments has further dampened private capital markets, causing corporate commercial paper (CP) and corporate bond yields to surge. With tens of trillions of won worth of PF-ABCP maturities looming, concerns are rising that continued liquidity tightening could lead to liquidity risks for securities firms.

◆Legoland Fallout Adds to Unstable Funding Market

According to the Korea Financial Investment Association on the 20th, the 91-day CP rate closed at 4.02% (based on credit rating A1) on the previous day (19th). This is the first time since January 28, 2009 (4.09%) that the 91-day CP rate has exceeded 4%. While the sharp rise in CP rates is partly due to the Federal Reserve's aggressive tightening, the 'Gangwon-do asset-backed commercial paper (ABCP)' incident had a direct impact. On the 4th, the special purpose company (SPC) under Gangwon-do, iOne First SPC, which issued ABCP worth 205 billion won to build Legoland in Chuncheon, was finally declared in default.

The SPC was established by Gangwon Jungdo Development Corporation (GJC), which was responsible for the Legoland project, to raise project funds. When the SPC issued the ABCP, Gangwon-do provided a payment guarantee for the bonds. However, when the maturity date (September 29) arrived, the SPC did not issue refinancing and notified institutions that loan repayment was impossible. Since Gangwon-do, which guaranteed the payment, did not repay the loan principal, an event of loss of benefit of time (EOD) occurred, leading to the ABCP being declared in default.

Furthermore, statements by Governor Kim Jin-tae of Gangwon-do exacerbated market anxiety. On the 28th of last month, Governor Kim said, "To escape the guarantee burden of 205 billion won, we have decided to apply for rehabilitation of the Development Corporation," adding, "If the court-appointed administrator sells the corporation's assets properly at fair value, the loan can be repaid."

However, if the court initiates rehabilitation procedures for GJC, it will become difficult for investors to recover their investments. Under the procedure, all debt repayments by GJC are frozen, and a court administrator intervenes to sell the company's assets. Ultimately, although Gangwon-do has stated it will repay the loan, the shock to the funding market has not subsided.

A securities firm official explained, "The Legoland ABCP was a bond guaranteed by a local government (Gangwon-do) and received credit comparable to government bonds," adding, "Since a bond believed to be risk-free has defaulted, credit issues are now being raised across the CP and corporate bond markets."

◆Will Liquidity Tightening Spread Across CP and Corporate Bonds?

The securities industry points out that the Legoland ABCP incident has increased anxiety in the bond market. Although Gangwon-do has declared it will repay the loan after much controversy, uncertainty has spread throughout the bond market.

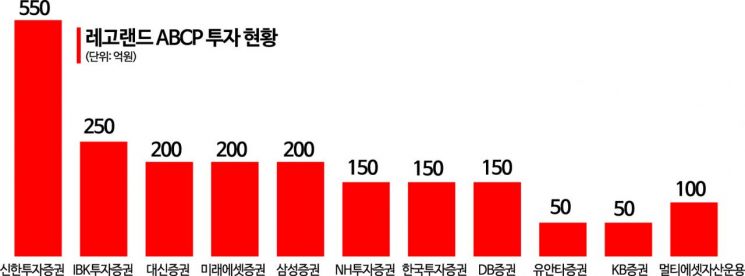

Regarding the scale of Legoland ABCP investments, Shinhan Investment Corp. holds 55 billion won, IBK Investment & Securities 25 billion won, Daishin Securities 20 billion won, Mirae Asset Securities 20 billion won, Samsung Securities 20 billion won, NH Investment & Securities 15 billion won, Korea Investment & Securities 15 billion won, DB Securities 15 billion won, Yuanta Securities 5 billion won, KB Securities 5 billion won, and Multi Asset Management 10 billion won.

Real estate PF ABCP is corporate commercial paper issued mainly by securities firms to securitize real estate PF loan receivables and gather multiple investors. The problem is that the maturities of real estate PF ABCP are approaching. The amount of real estate PF ABCP maturing in the fourth quarter alone is reported to be 31.4 trillion won. Moreover, real estate PF borrowers tend to have relatively low credit ratings. Approximately 27% of real estate PF ABCP have credit ratings below A2, compared to around 10% for other short-term instruments. If refinancing of ABCP fails, the issuing securities firms must bear the burden directly.

A representative of a Legoland ABCP investor said, "With even the highest-grade corporate commercial paper ‘A1’ becoming untrustworthy, liquidity tightening in the real estate PF market has intensified," adding, "Due to interest rate hikes and rising raw material prices, projects that were already unprofitable are now facing credit risks."

External conditions are also unfavorable. The trend of interest rate hikes is expected to continue this year. There is even speculation that the Federal Reserve may implement a ‘giant step’ (a 0.75 percentage point hike in the benchmark rate at once) at the November Federal Open Market Committee (FOMC) meeting. Since the Bank of Korea has also announced it will maintain its rate hike stance, the real estate PF market is bound to cool further. If the situation persists, securities firms could face liquidity risks.

As the situation worsened, the government stepped in. On the same day, Financial Services Commission Chairman Kim Ju-hyun announced in the ‘Special Instructions for Market Stabilization’ that "We will promptly resume purchases using 1.6 trillion won of available funds from the Channel Fund and prepare for additional capital calls immediately." He added, "We are closely monitoring the recent volatility expansion in the short-term funding market with vigilance," and "We are carefully monitoring market instability factors spreading after the Gangwon-do PF-ABCP issue." The FSC also plans to actively implement liquidity support through Korea Securities Finance.

An investment banking (IB) industry official said, "Recently, Korea Electric Power Corporation (KEPCO) issued a large-scale bond (KEPCO bond) with yields approaching 6%. If AAA-rated bond yields reach this level, it will become very difficult for other companies to issue bonds," adding, "This is a time when swift action by government authorities is necessary."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}