[Asia Economy Sejong=Reporter Kim Hyewon] The National Tax Service (NTS) will accept applications for this year's comprehensive real estate tax (Comprehensive Real Estate Tax, 종부세) exclusion from aggregation and temporary two-homeowner tax special cases from the 16th to the 30th.

The NTS announced on the 15th that it has sent notification letters for filing (application) since the 7th to about 640,000 people expected to be eligible for this year's 종부세 exclusion from aggregation and tax special cases.

Notification letters were sent to 157,000 couples with joint ownership, 47,000 temporary two-homeowners, 10,000 inheritance homeowners, 35,000 owners of low-priced houses in local areas, and 390,000 people eligible for exclusion from aggregation such as rental housing.

However, the temporary special deduction of 1.4 billion KRW for one household one homeowner, which failed to pass in the National Assembly, was excluded from the target.

92,000 People Eligible for Temporary Two-Homeowner, Inheritance Housing, and Local Low-Priced Housing Special Cases

The total number of people newly eligible for this year's temporary two-homeowner, inheritance housing, and local low-priced housing special cases is 92,000.

Taxpayers who applied for tax special cases for couples jointly owning one house, temporary two-homeowners, inheritance housing, and local low-priced housing one household one homeowner special cases will be subject to the one household one homeowner calculation method.

Even if they are not one household one homeowner, taxpayers who own inheritance housing or unauthorized housing accessory land will be subject to tax rates based on the number of houses calculated excluding those houses.

Properties reported for exclusion from aggregation are excluded from taxation. Public interest corporations such as religious organizations, public housing operators, social enterprises/cooperatives, and Jongjung (ancestral clan organizations) can apply for special cases and receive general progressive tax rates instead of corporate housing tax rates and a basic deduction benefit of 600 million KRW.

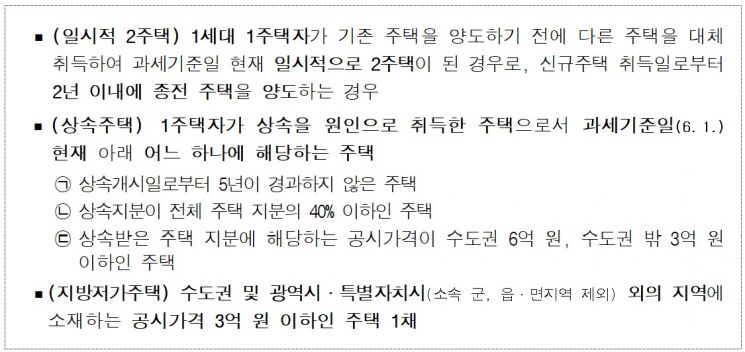

The newly introduced temporary two-homeowner, inheritance housing, and local low-priced housing tax special cases this year consider a one household one homeowner as such even if they temporarily become two-homeowners due to moving, inherit a house, or additionally own a local low-priced house.

Being considered a one homeowner allows benefits such as a basic deduction of 1.1 billion KRW and elderly/long-term holding tax credits (up to 80%).

The temporary two-homeowner special case applies when a taxpayer acquires another house before disposing of the existing house and becomes a temporary two-homeowner as of June 1 this year.

However, the previous house must be sold within two years from the acquisition date of the new house, and failure to comply will result in additional tax and interest charges.

To receive the inheritance housing special case, the inherited house must meet one of the following as of June 1: the inheritance start date (deceased date of the decedent) is within five years, the inherited share is 40% or less of the total house share, or the official price corresponding to the inherited share is 600 million KRW or less in the metropolitan area or 300 million KRW or less outside the metropolitan area.

Even if multiple houses are inherited, if the houses meet the requirements, the one household one homeowner special case can be applied.

The local low-priced housing special case applies only when owning one additional house priced at 300 million KRW or less located outside the metropolitan area, metropolitan cities, and special self-governing cities (excluding affiliated counties, towns, and townships).

Couples with Joint Ownership of One House Can Choose Single Ownership... Workplace Daycare Also Eligible for Exclusion from Aggregation

As in last year, couples with joint ownership of one house can choose the more advantageous option between joint ownership, which allows a total deduction of 1.2 billion KRW (600 million KRW per person), and single ownership, which allows an 1.1 billion KRW deduction plus elderly/long-term holding tax credits.

As of June 1, if a couple jointly owns only one house and other household members do not own any houses, they are eligible to apply for the single ownership special case.

Exclusion from aggregation can be reported for rental housing meeting requirements such as exclusive area and official price, employee housing such as dormitories, and land acquired by housing developers for housing construction.

Previously, only homes used for home daycare centers were eligible for exclusion from aggregation, but starting this year, all homes used for daycare centers, including workplace daycare centers, are subject to exclusion from aggregation reporting.

The NTS urged, "If it is confirmed after applying the tax special cases and exclusion from aggregation that the requirements are not met, the reduced tax amount and additional penalties must be paid, so please file and apply sincerely."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}