Decision on 320 Billion Won Capital Increase... Funding for 'B737-Max' Introduction

Interest Expenses to Rise from 41.4 Billion Won in 2023 to 123.2 Billion Won in 2027

"EPS Expected to Decrease to 1,391 Won by 2027"

Increased Competition with Launch of Hanjin Integrated LCC

Resumption of Japan Routes a Short-Term Positive Factor

[Asia Economy Reporter Hwang Yoon-joo] Jeju Air is flying low due to a larger-than-expected rights offering and concerns over intensified competition.

As of 9:10 a.m. on the 6th, Jeju Air's stock price was 15,250 KRW, down 9.23% from 16,800 KRW on the 25th of last month.

It has fallen 4.9% since the second half of the year began. Despite high expectations from the resumption of routes to Japan, the stock price remains low, and securities firms are lowering their target prices for Jeju Air. KB Securities lowered it to 15,000 KRW (down 6.3%), Daishin Securities to 17,000 KRW (down 34.6%), and SK Securities to 18,000 KRW (down 30.8%).

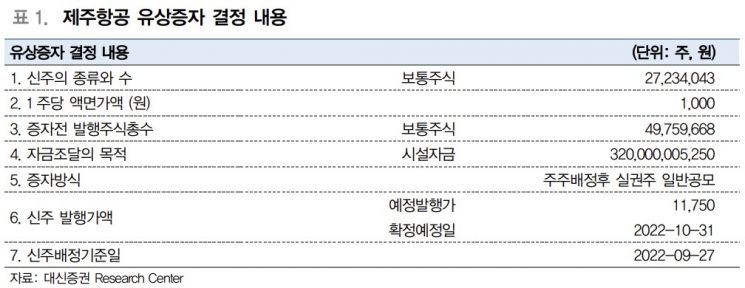

The main reason for the cautious evaluation of Jeju Air is the larger-than-expected rights offering plan. Jeju Air announced on the 26th of last month that it had decided on a rights offering worth 320 billion KRW (27.23 million shares).

The size of the rights offering far exceeded the securities firms' estimate (12.35 million shares), which became a risk factor. Due to the rights offering, the number of Jeju Air's outstanding shares will increase nearly threefold from 26.29 million shares at the end of 2019 before COVID-19 to 76.92 million shares after the end of 2022. Accordingly, Jeju Air's stock price fell more than 10% on the trading day following the announcement, on the 29th of last month.

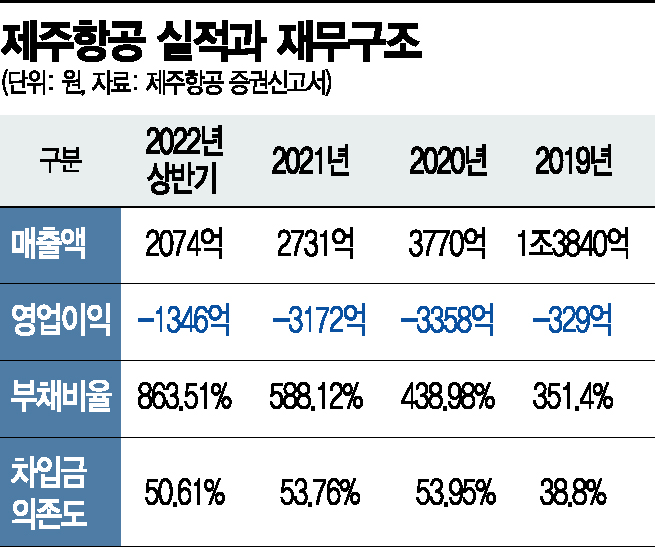

Cost burdens are also expected to increase. The rights offering appears to be aimed at raising funds for the introduction of the 'B737-Max' decided in 2018. Jeju Air plans to introduce at least 40 aircraft over five years. As a result, annual interest expenses are expected to sharply rise from 41.4 billion KRW in 2022 to 123.2 billion KRW in 2027.

Jeju Air expected improved performance from the resumption of the Japan routes, which accounted for a high sales proportion. However, the surge in travel demand at the early stage of reopening is seen as a short-term positive factor.

Kang Sung-jin, a researcher at KB Securities, analyzed, "Jeju Air's earnings per share (EPS), which was 2,936 KRW in 2017, is expected to decrease to 1,391 KRW in 2027 due to increased interest expenses and the number of shares, despite normalization of the industry and fleet expansion."

There are also concerns about the launch of Hanjin Group's integrated low-cost carrier (LCC). Recently, Australian authorities unconditionally approved the merger of Korean Air and Asiana Airlines, accelerating the merger process. It is explained that competition with Jin Air, the second-largest LCC, will intensify once the integrated LCC is launched.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}