Conflicting Securities Firm Outlooks

"Jeongamaesu Recommended" vs Target Price Downgrade

[Asia Economy Reporter Ji Yeon-jin] Securities firms have shown mixed evaluations of Hanse Industrial, whose stock price has plummeted over the past four months. While some raised their target prices to the early April peak level, citing that the stock price drop was excessive, others lowered their target prices due to inventory adjustment impacts.

On the 16th, according to the financial investment industry, Meritz Securities recommended buying Hanse Industrial at a low price, stating that the stock price drop was excessive compared to concerns about earnings. They set the target price at 29,000 KRW. Hyundai Motor Securities raised their target price from 27,000 KRW to 28,000 KRW.

Hanuri, a researcher at Meritz Securities, said, "Hanse Industrial has a 12-month forward price-to-earnings ratio (PER) of 5.8 times, which is half that of the latecomer Taiwanese company Makalot." He added, "It is true that a red light has been turned on for global apparel exports, and economic contraction is worsening consumer sentiment, leading to sluggish front-end sales and inventory burdens. However, structural improvement based on vendor market share growth and an increase in the proportion of high-priced products is effective." He also pointed out that additional expansion in Latin America, the operation of a new factory in Myanmar (with tariff-free exports to the EU), diversification of production sites, and expansion of the fabric business are attractive investment points.

On the other hand, Daishin Securities lowered the target price for Hanse Industrial by 17.9%, from 28,000 KRW to 23,000 KRW on the 16th, stating that despite a surprise performance in the second quarter this year, sales growth is expected to slow for a while. However, they maintained a 'buy' investment opinion, anticipating a rebound from the second half of next year.

Yoo Jeong-hyun, a researcher at Daishin Securities, said, "Hanse Industrial's sales in the third quarter of this year are expected to increase by 20% in US dollar terms," but forecasted, "Sales growth will slow due to the burden from strong performance since the fourth quarter of last year." He predicted that profit decline is inevitable until the first half of next year.

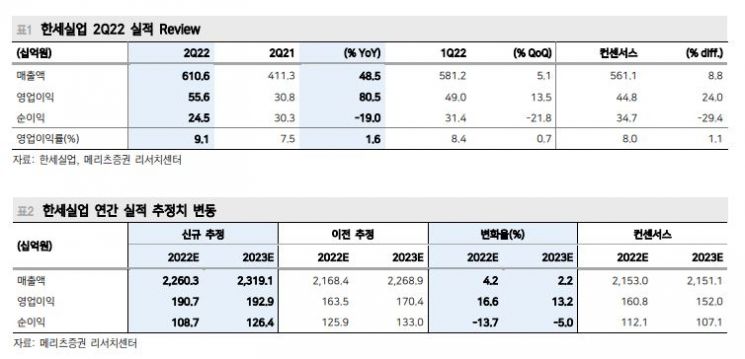

Meanwhile, Hanse Industrial's sales in the second quarter of this year reached 610.6 billion KRW, a 48.5% increase compared to the same period last year. Operating profit rose 80.5% to 55.6 billion KRW, while net profit decreased 19% to 24.5 billion KRW. Operating profit exceeded market expectations by 24%. It is analyzed that product price increases and exchange rate effects significantly boosted operating profit. However, the stock price fell from 29,500 KRW on April 5 to 17,550 KRW on the 12th.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}