"The principle of exclusivity within the financial industry is maintained, and finance-led non-financial convergence is also limited, posing constraints"

[Asia Economy Reporter Park Sun-mi] Recently, although financial authorities have promised to ease regulations related to bank applications (apps), it remains difficult to launch a single super app due to numerous legal constraints such as the Financial Holding Companies Act, the Financial Investment Services and Capital Markets Act, and the Financial Consumer Protection Act, which make customer information sharing among financial industries complicated. Among experts, there is active discussion on the need to improve the exclusive business regulations in the financial sector and to expand information sharing among affiliates.

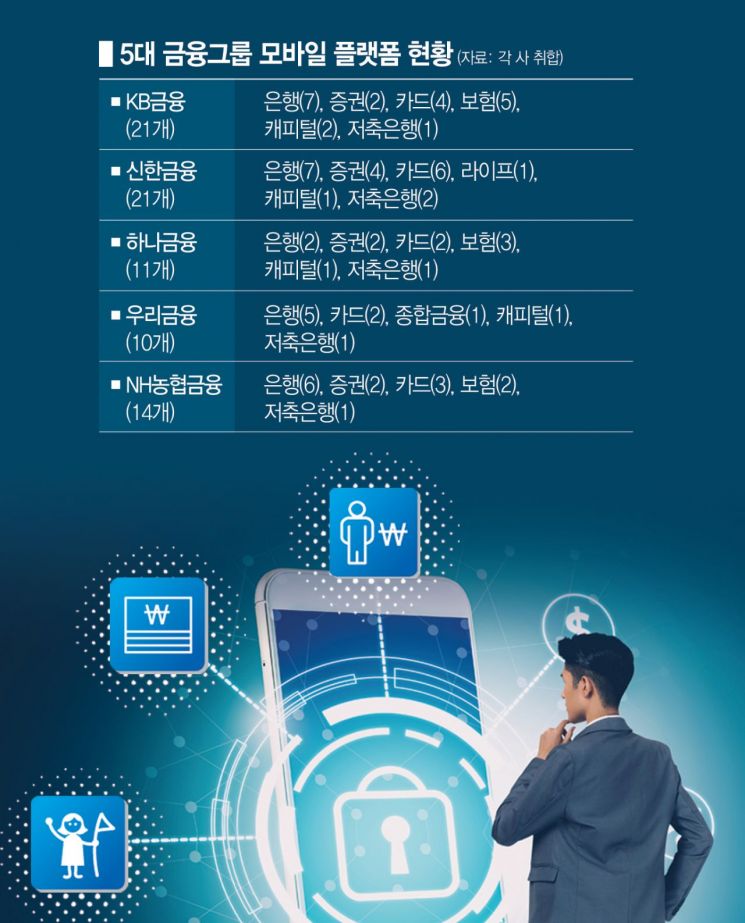

According to the financial sector on the 5th, the number of financial apps operated by five financial groups?KB, Shinhan, Hana, Woori, and NH Nonghyup?deemed effective, reaches 77. The groups with the most apps are KB and Shinhan, each offering 21 apps. Hana Financial operates 11 apps, while Woori and NH Nonghyup run 10 and 14 mobile platforms respectively.

Financial groups have been working for several years to create a ‘smart representative app’ that integrates affiliate services to respond to competition with big tech and fintech companies and to prevent the loss of MZ (Millennial + Generation Z) generation customers. However, as various financial service-related apps were added, consumer inconvenience increased. Apps with low usage frequency often got mixed with existing apps and were left neglected.

Financial companies cited regulatory barriers as the reason why a one-app strategy is difficult. A financial sector official explained, "There were many legal constraints such as the Financial Holding Companies Act, the Financial Investment Services and Capital Markets Act, and the Financial Consumer Protection Act, which made customer information sharing among group companies complicated."

On the other hand, big tech and fintech companies offer all services through a single super app. They incorporate banking, securities, insurance, payments, and other services into one financial app in a functional format, eliminating the need to install multiple apps from the start, creating a sensation.

Experts agree on the need to improve exclusive business regulations in the financial industry and to expand information sharing among affiliates as various financial services converge actively due to changes in the digital environment. Within the financial industry, the principle of exclusivity is strictly maintained, and financial-led non-financial convergence is also restricted, making innovation difficult; thus, improvement of exclusivity regulations is necessary.

Professor Yeo Eun-jung of Chung-Ang University said, “With the emergence of big tech financial operators, the meaning of the exclusivity principle inevitably fades due to the realization of de facto ‘universal banking’ through platforms,” adding, “It is necessary not only to consider applying the same regulations to big tech activities for financial consumer protection but also to explore various approaches to protect financial consumers in the digital age.”

Jung Joong-ho, Head of Hana Financial Management Research Institute, pointed out, “As consumers’ digital experiences become common, demands for one-stop services for financial and non-financial products are increasing,” and said, “To respond to the emerging trend where financial and non-financial convergence and platformization are becoming major competitive strategies, it is necessary to allow financial companies to provide non-financial convergence services.”

Jo Young-seo, Head of KB Management Research Institute, also mentioned, “Banks must evolve into digital financial platforms to provide hyper-personalized services through lifecycle asset management and the combination of financial and non-financial data,” and expressed the opinion, “To achieve this, investment discretionary business and investment advisory business other than real estate should be included in banks’ concurrent businesses, and banks should be allowed to invest in companies related to real estate, health, automobiles, telecommunications, and distribution.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}