Lee Ju-yeol "Prolonged Low Interest Rates One Factor Behind Asset Market Fund Concentration"

[Asia Economy Reporter Kim Eunbyeol] Although there has been a global surge in housing prices since the COVID-19 pandemic, it has been found that the rise in housing prices in South Korea is more closely linked to the increase in household debt. This was confirmed by statistics following remarks made by Lee Ju-yeol, Governor of the Bank of Korea, at a press conference after the Monetary Policy Committee meeting, stating that "the price-to-income ratio (PIR) of housing in the Seoul metropolitan area, including Seoul, is significantly higher than in other countries, and the price increase is closely connected to the rise in debt."

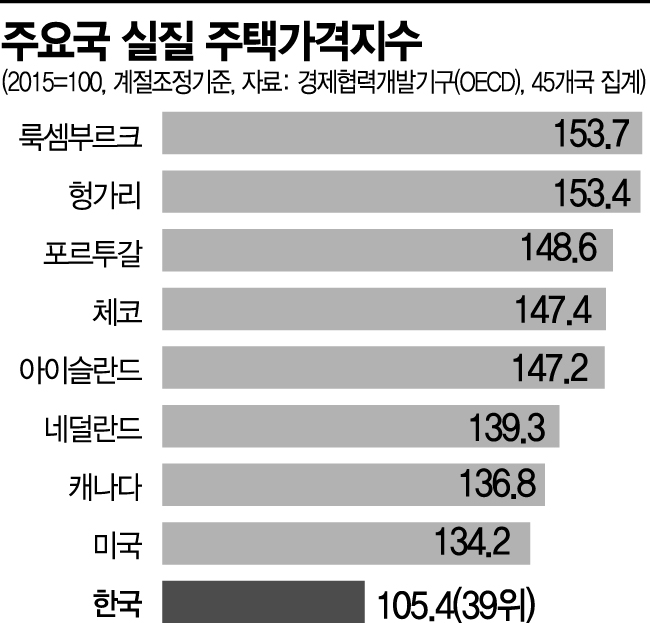

According to data compiled by the Organisation for Economic Co-operation and Development (OECD) on the 16th, when compared with major overseas countries, South Korea’s housing price level was not particularly high. Looking at the real housing price index compiled by the OECD with 2015 as 100, South Korea scored 105.4, ranking 39th out of 45 countries surveyed by the OECD. Housing prices rose more sharply in advanced countries such as Luxembourg (153.7), the Netherlands (139.3), and the United States (134.2). In Bloomberg’s “Housing Bubble Ranking,” New Zealand ranked first, with Canada, Sweden, and Norway also in the top 10. South Korea ranked 19th.

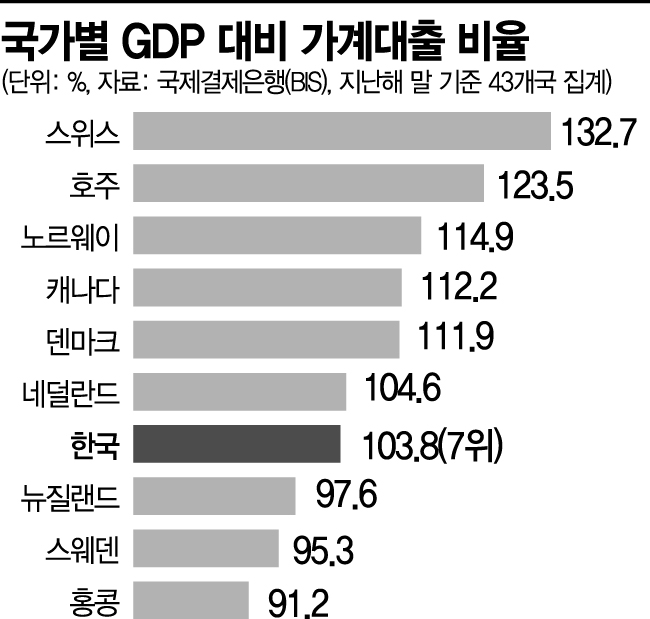

However, the story is different for household debt. In the first quarter of this year, South Korea’s household debt reached 1,765 trillion won, increasing by 9.5% compared to the same period last year, maintaining a high growth rate. Bank household loans also increased by 41.6 trillion won in the first half of the year, setting a record for the largest increase in the first half. The household debt-to-GDP ratio stood at 103.8%, ranking 7th among 43 countries compiled by the Bank for International Settlements (BIS).

This suggests that the rise in housing prices in South Korea is based on household debt. Unlike other countries where suburban real estate prices rose, housing prices in South Korea skyrocketed mainly in metropolitan cities such as Seoul. Most citizens believe in the “real estate invincibility” myth and often take out the maximum possible loans within their limits to buy homes. This trend continues, creating a vicious cycle that further stimulates housing prices.

Global housing prices rose after COVID-19, but

South Korea’s housing prices surged based on debt... Risk in case of internal and external shocks

"Need to raise interest rates to control prices"

The reason the Bank of Korea intends to raise the base interest rate soon despite the fourth wave of COVID-19 is related to this. While the impact on face-to-face services and vulnerable groups cannot be ignored, the risks posed by asset investment fueled by loans and asset inequality are also considered dangerous.

If housing prices rise based on debt, the possibility of a sharp drop in housing prices increases in the event of internal or external shocks. Even if citizens with heavy debt burdens recover from COVID-19, they may not be able to increase consumption sufficiently. At the press conference, Governor Lee said, "Recent trends show that as long as there is an expectation that low interest rates will be maintained for a long time, there are limits to the government's macroprudential regulations," adding, "It has become increasingly necessary to respond with monetary normalization within the scope of deteriorating macroeconomic conditions."

Jeon Sung-in, a professor of economics at Hongik University, also advised that now not only ‘quantity control’ of loans such as Loan-to-Value (LTV) and Debt Service Ratio (DSR) regulations but also ‘price control’ by raising interest rates is necessary. He said, "Continuing the liquidity party will only increase financial market instability," and added, "It’s not just about making loans harder to get, but the price of borrowing should also rise."

Meanwhile, Governor Lee appeared before the National Assembly’s Planning and Finance Committee on the same day and stated, "The long-term continuation of low interest rates and the market’s expectation that they will continue have been one of the factors driving funds into the asset market." However, he also said, "We need to consider whether there has been sufficient supply in the areas people want."

Regarding the indication of an interest rate hike within the year, he said, "If the economic situation improves, we are communicating with the market in advance about plans to start normalization to mitigate the side effects of prolonged low interest rates." He also said, "I understand that self-employed people and small business owners in face-to-face service industries, as well as those with unstable employment, who have borrowed, will face difficulties with interest repayment burdens," but added, "I think it would be more effective to use fiscal policy rather than monetary policy going forward." He also mentioned, "We will consider possible measures at the Bank of Korea level, such as financial intermediary support loans."

Lee Ju-yeol, Governor of the Bank of Korea, is striking the gavel at the Monetary Policy Committee plenary meeting held at the Bank of Korea in Jung-gu, Seoul, on the morning of the 15th.

Lee Ju-yeol, Governor of the Bank of Korea, is striking the gavel at the Monetary Policy Committee plenary meeting held at the Bank of Korea in Jung-gu, Seoul, on the morning of the 15th. [Photo by Yonhap News]

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}