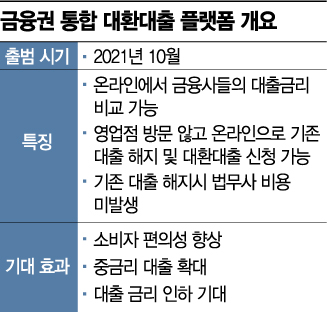

Ahead of October Service Launch

Financial Authorities Coordinate Opinions with Industry

[Asia Economy Reporter Kiho Sung] Financial authorities are accelerating coordination with related industries ahead of the non-face-to-face refinancing loan service scheduled for launch in October. The key issues are the form in which refinancing loans are made and the loan brokerage and early repayment fees. In particular, conflicting interests among industries over fees are expected to be the biggest hurdle for the launch of the non-face-to-face refinancing loan service.

According to the financial sector on the 10th, the Korea Financial Telecommunications & Clearings Institute held discussions with 12 private companies (Finda, Viva Republica, NHN Payco, Rainist, Fink, MyBank, Pinset, Fintech, TeamWink, Pinmart, Kakao Pay, SK Planet) and 4 related associations (Korea Federation of Banks, Korea Inclusive Finance Agency, Credit Finance Association, Fintech Industry Association). The meeting was held as a courtesy meeting to understand the operation method of the refinancing loan service and to identify companies capable of providing the service by October this year.

Reactions to the non-face-to-face refinancing loan service vary by sector. The fintech industry welcomes it, as refinancing loans can increase fee profits and strengthen platform dominance. On the other hand, dissatisfaction is voiced in the banking sector and secondary financial institutions. Especially, there are many concerns from secondary financial institutions such as savings banks, credit card companies, and capital companies. Currently, the average interest rate on credit loans from savings banks is around 18%, with many customers paying up to 24%. Due to the large interest rate gap, cutthroat competition is inevitable.

Therefore, the financial industry's focus is on setting the fee rate. The fee rate between financial companies and the platform providers facilitating switching is crucial. Frequent loan transfers could increase brokerage fees for platform providers. Currently, a proposal to set the fee rate at less than half of the existing rate (1.6?2.0% of the loan amount) is being seriously considered.

Another issue is the early repayment fee. If financial companies set high early repayment fees, switching loans becomes difficult. There are opinions that early repayment fees should be set at an appropriate level to activate the service.

The operation method of the refinancing loan service is also a key point. There is a significant disagreement among sectors between the authorities’ ‘infrastructure’ model and the fintech companies’ ‘platform’ model. The infrastructure model is easier to supervise, while the platform model offers better consumer accessibility.

A savings bank official said, "Currently, credit loan interest rates of savings banks are being compared and analyzed by consumers through affiliated fintech companies," adding, "However, if a significant number of customers gather on the refinancing loan platform in the future, the industry may face additional competition factors such as interest rate reduction competition or promotions."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}