Public Sentiment Turns Against Ruling Party in By-Elections

Push for Significant Loan Regulation Easing

Policy Consistency Emphasized but Out of Sync with Blue House

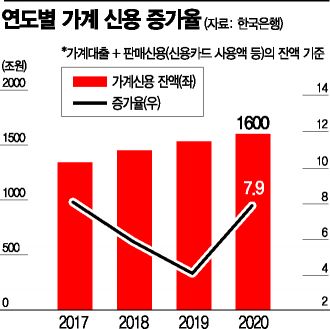

[Asia Economy Reporter Kiho Sung] Since the April 7 by-elections, the political sphere has introduced drastic loan regulation relaxation policies, raising concerns within the financial sector. In particular, the ruling party, having confirmed public discontent due to the failure to stabilize real estate and loan regulations, is exerting strong influence. However, there appears to be a discord with the Blue House, which insists on maintaining consistency in existing housing policies. The market is worried that with household loan balances exceeding 1,000 trillion won, loosening loan regulations during a period of rising interest rates will inevitably deteriorate the quality of household debt. This could become a burden not only for the financial sector but also for the entire domestic economy. Furthermore, the policy stance of the financial authorities responsible for household debt has inevitably become confused.

Loan Regulation Authorities Struggle Amid Discord Between Ruling Party, Government, and Blue House

◆Flood of Populist Financial Policies from the Ruling Party= According to political and financial sources on the 14th, the ruling party, sensing public discontent over real estate in the election, is pushing for significant relaxation of loan regulations for youth and the homeless. During a joint speech session held the previous day, candidates for the Democratic Party floor leader unanimously agreed that the next leadership should review real estate easing policies. Representative Yoon Ho-jung said, "If elected as floor leader, I will urgently review real estate policies and prepare countermeasures." Representative Park Wan-joo also emphasized, "If elected as floor leader, I will create a special committee on real estate and actively support policies."

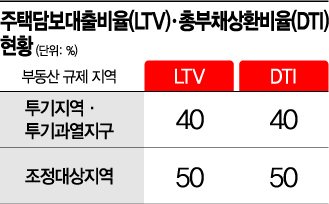

Additionally, Representative Song Young-gil, running for party leader, argued, "For first-time homebuyers without a house, the loan-to-value ratio (LTV) and debt-to-income ratio (DTI) should be drastically increased to 90% so they can buy a house immediately." This means allowing home purchases with only 10% of the house price.

The ruling party's loan regulation relaxation stance was rapidly formed just before the election. Former leader Lee Nak-yeon announced the ‘National Responsibility System for Homeownership,’ which aims to significantly ease financial regulations for first-time homebuyers and greatly expand tailored support such as preferential housing subscription. Hong Ik-pyo, the party’s policy committee chairman, also stated, "LTV and DTI will be raised for low-income real demanders." Chief spokesperson Choi In-ho of the Democratic Party said, "There is a possibility that financial regulations such as DTI will be somewhat relaxed to create conditions for the homeless and youth to secure housing."

The problem is that the ruling party, government, and Blue House seem to have reached no agreement on loan regulation relaxation. Prime Minister Chung Sye-kyun drew a line, saying he "has not been briefed" on the Democratic Party’s real estate loan regulation easing, and Lee Ho-seung, director of the Blue House policy office, emphasized, "We believe it is a very important time to maintain consistency in housing policy."

Financial authorities are also in a difficult position due to the discord among the ruling party, government, and Blue House. Not only is the lack of unified opinion problematic, but there is also concern that it could send the wrong signal of ‘loosening the money supply,’ further unsettling the market. The Financial Services Commission, which planned to announce household debt management measures last month, had to postpone the announcement due to the land speculation scandal involving employees of the Korea Land and Housing Corporation (LH), increasing its dilemma.

Populist financial policies beyond loans are also pouring out. Last month, the ‘Partial Amendment to the Act on Support for Financial Life of the Underprivileged (Amendment to the Underprivileged Financial Support Act),’ which requires all financial sectors to bear the costs necessary for operating financial products for the underprivileged, was passed. It is regarded as the ‘first case of profit-sharing’ in conjunction with the ‘Profit Sharing System’ proposed by the Democratic Party in January.

Independent lawmaker Lee Yong-ho introduced a bill to lower preferential commission rates for card company merchants, and Democratic Party lawmaker Min Hyun-bae proposed a law allowing self-employed people to request debt forgiveness from financial institutions during disasters, with banks required to take appropriate measures.

Populist Financial Policies Without Party Lines... Experts Warn "Inconsistent Policies Cause Financial Market Confusion"

◆Financial Sector Caught Between Ruling Party, Government, and Blue House... Experts Say "Don’t Amplify Confusion"= Populist financial policies know no party boundaries. Seoul Mayor Oh Se-hoon pledged ‘4-No Loans’ as an election promise. The ‘4-No Loans’ refer to no guarantee fees, no interest, no collateral, and no paperwork. The core is to provide loans up to 100 million won to self-employed people who suffered during COVID-19. According to Mayor Oh’s manifesto, the number of beneficiary businesses is estimated at 200,000 when applying a 50 million won limit, and 400,000 when applying the actual average amount of 25 million won.

Banks, which would actually provide the loans, say the promise is not entirely impossible but worry that if loan defaults increase, the impact could spread to banks as well. A bank official said, "We need a concrete implementation plan to accurately evaluate, but since the Seoul Credit Guarantee Foundation provides guarantees and Seoul City pays the interest, it is not an impossible structure." However, the official pointed out, "There is no collateral, and it is difficult to properly assess repayment ability, so if loan defaults spread, Seoul City alone has limitations and it could affect the banking sector."

Experts warn that indiscriminate loan relaxation combined with the real estate market could cause significant turmoil. Professor Sung Tae-yoon of Yonsei University’s Department of Economics said, "The current disruption in the real estate and housing market stems from policy aspects, especially related to jeonse and monthly rent regulations, and trying to solve this suddenly by expanding loans is risky." He added, "It could also fuel confusion regarding policy consistency."

There are also forecasts that rapid policy shifts could further accelerate house price increases. Professor Kim Sang-bong of Hansung University’s Department of Economics emphasized, "We need to carefully consider whether the political and government movements are aligned. Now is the time to focus on supply rather than loosening money, ensuring timely supply to those who need and can afford housing."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}