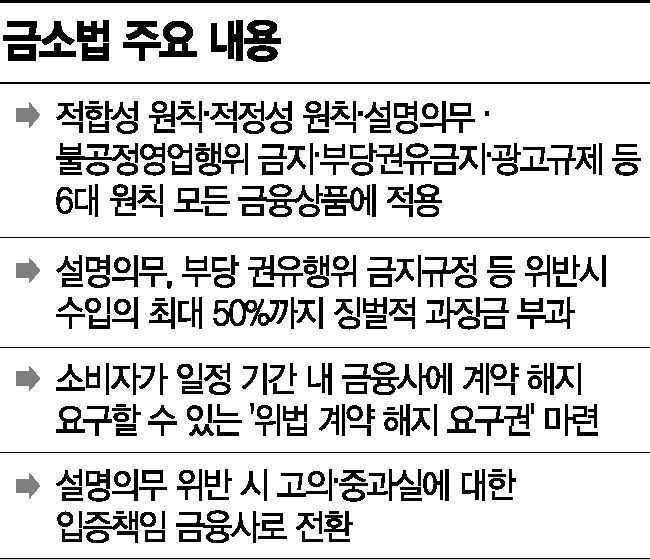

[Asia Economy Reporter Park Sun-mi] In preparation for the enforcement of the Financial Consumer Protection Act (FCPA) on the 25th, financial authorities are posting answers to major inquiries to minimize confusion in the field. The following are Q&A contents related to the FCPA posted on the Financial Services Commission and Financial Supervisory Service websites.

Q. What sanctions apply if a loan solicitor who has been conducting business fails to register with the FSC by the enforcement date (March 25)?

Registration for new operators is expected to be possible from September 25 this year, similar to 'financial product advisory businesses.' To prevent operators who have been engaged in loan solicitation (including lease and installment finance solicitors) before the 24th of this month from suffering disadvantages due to non-registration, such operators will be considered registered with the FSC until September 25, and no sanctions will be imposed for non-registration during this period.

Q. Do prepaid/debit payments, credit card cash services, and revolving credit fall under financial products under the FCPA?

Prepaid and debit payments are judged not to be similar to the financial products listed in Article 2, Paragraph 1 of the Act. On the other hand, cash services and revolving credit arising from agreements added upon credit card subscription are not easily regarded as independent separate financial products themselves, but since credit cards are considered financial products, regulations under the FCPA, such as the obligation to explain matters related to cash services and revolving credit in connection with credit card contract conclusion, apply.

Q. Does the act of introducing financial product sellers (including online) fall under the legally required registration category of 'financial product sales agency/brokerage'?

'Financial product sales agency/brokerage' refers to the business of acting as an agent or broker in concluding contracts related to financial products. If the activity occurs before the solicitation of financial products and is not considered to have a direct impact on the conclusion of financial product contracts, it generally does not qualify as brokerage.

Q. By the enforcement date of September 25 for the internal control standards under the FCPA, must organizations and executives required by the internal control standards be established?

The securing of organizations and personnel related to internal control standards is a matter to be included in the standards according to the draft subordinate regulations of the FCPA, but it is not an obligation to be fulfilled exactly on the enforcement date. Therefore, organizations and executives related to internal control standards should prepare the internal control standards by the enforcement date and subsequently establish the related organizations and personnel through necessary procedures such as shareholders' meetings and board meetings without delay.

Q. Should the Consumer Protection Internal Control Committee be separate from the existing internal control committee under the 'Financial Company Governance Act'?

The purpose of the draft enforcement decree of the FCPA requiring the inclusion of the establishment of a 'Consumer Protection Internal Control Committee' in the internal control standards is to have representatives and key executives discuss major decisions regarding overall business activities from the perspective of consumer protection, thereby embedding consumer protection-centered management within the organization. As long as this purpose is not violated, for organizational management efficiency, it is not necessary to form the Consumer Protection Internal Control Committee separately from the existing internal control committee under the 'Financial Company Governance Act' if deemed necessary.

Q. If the consumer protection department can operate independently from the sales department, is it possible to operate it together with other departments?

The purpose of including necessary matters for securing the independence of the consumer protection department from the sales department in the internal control standards in the draft enforcement decree of the FCPA is to prevent conflicts of interest between consumer protection and sales department tasks and to enhance the organization's consumer protection capabilities. As long as this purpose is not violated, for organizational management efficiency, it is possible to operate the consumer protection department together with other departments directly under the representative, such as the compliance officer, if necessary. However, if a separate executive in charge of the consumer protection department is appointed, it cannot be operated together with other departments.

Q. In the case of non-face-to-face transactions, is it considered that there is no 'solicitation' by the seller, and thus the suitability principle does not need to be applied?

In non-face-to-face transactions, if the consumer expresses the intention to receive 'solicitation' for financial products subject to the suitability principle under the FCPA, and then the financial product seller solicits the conclusion of a financial product contract, the suitability principle generally applies. ▲When the consumer provides information necessary for tailored product recommendations, ▲when the consumer selects specific criteria (such as transaction frequency, yield, interest rate, loan limit) to find products meeting those criteria, etc., it is generally considered that the consumer has expressed the intention to receive 'solicitation.'

Afterward, solicitation such as product recommendation and explanation can proceed only if the consumer agrees to the application of the suitability principle. However, it is prohibited to solicit unsuitable products after obtaining the consumer's signed confirmation of 'not wanting product solicitation' and 'wanting contracts for unsuitable products.'

Q. What is the scope of money that financial product sellers must pay consumers when exercising the right to rescind illegal contracts?

The purpose of introducing the right to rescind illegal contracts is to ensure that consumers do not suffer financial disadvantages from contract termination due to illegal contracts. It is important to note that this differs from the right to claim damages for losses caused by illegal contracts. Since the effect of rescinding an illegal contract occurs prospectively, the contract becomes void from the time of rescission. Therefore, costs incurred during the service provision process under the contract from contract conclusion to rescission are generally not included in the scope of money to be paid to the consumer after contract rescission.

Q. What is the scope of advertising related to the 'business' of financial product sellers, etc.?

The purpose of regulating business advertising is to prevent financial consumers from being misled about related financial products due to business advertising. Business advertising can be classified into two types: ▲ advertisements related to advisory services of financial product advisors, and ▲ advertisements related to services provided by financial product sellers to induce consumers to conclude financial product contracts.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}