[Asia Economy Reporter Jang Hyowon] Automotive parts manufacturer Myungshin Industry has been on a growth trajectory since it began supplying body parts to Tesla in 2018. This is because lightweight body technology is an essential factor in increasing the driving range of electric vehicles. It is expected that Myungshin Industry’s parts will also be used in Tesla’s next model, indicating a bright future outlook. However, there are many potential shares such as convertible bonds (CB), which may cause stock dilution issues after the lock-up period ends.

Construction of 2nd Plant in the U.S.

Myungshin Industry manufactures automotive body parts. It is a secondary supplier that delivers lightweight body parts to assembly companies through its core technology, the ‘hot stamping process.’ Its major clients include Hyundai and Kia Motors, and it also sells body parts to partners such as Tesla in the U.S. and BYD in China.

Demand for Myungshin Industry’s products is gradually increasing as the electric vehicle market expands. Due to the characteristics of electric vehicles, where battery efficiency is crucial, vehicle weight must be reduced to increase driving range. Hot stamping is a technology that manufactures ultra-lightweight, ultra-high-strength parts by simultaneously performing high-temperature heating above 950 degrees Celsius, forming, and cooling through electric control technology. The global market size for hot stamping was approximately 12 trillion KRW in 2019, with an annual growth rate of 15.2%. Additionally, global electric vehicle sales are expected to more than double from around 6 million units in 2020 to 2023.

Myungshin Industry recorded consolidated sales of 354.7 billion KRW and operating profit of 22.7 billion KRW in the first half of last year. Due to the global economic downturn caused by the COVID-19 pandemic, these figures decreased by 6.3% and 24.8%, respectively, compared to the same period the previous year. Although there was a temporary slowdown in the first half, recent sales growth has been remarkable.

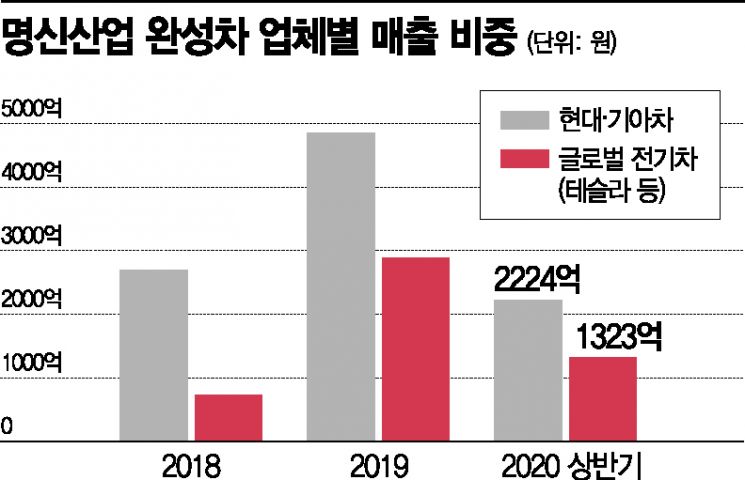

Myungshin Industry’s average annual sales growth rate from 2016 to 2019 reached 61%. In particular, sales more than doubled starting in 2018. This increase is attributed to the exclusive supply of hot stamping parts to Tesla, the world’s leading electric vehicle manufacturer, from that year. Sales of hot stamping body parts to global electric vehicle clients surged 293%, from 73.7 billion KRW in 2018 to 289.7 billion KRW in 2019. The share of global exports in total sales also expanded from 21.4% to 37.3% during the same period. Global sales remained robust, recording 132.3 billion KRW through the first half of last year.

In line with Tesla’s aggressive sales expansion, Myungshin Industry plans to establish a second plant in the U.S. At the end of last year, Myungshin Industry raised 24.4 billion KRW by listing on the KOSPI. All of these funds are planned to be invested in establishing the second U.S. base plant.

Park Chansol, a researcher at SK Securities, said, “The production of the second model will expand much faster than the first model in the future,” and added, “Since Myungshin Industry will exclusively supply parts for the second mass-market model as well, its performance is expected to grow rapidly.”

Will a Large Volume Flood the Market on June 7?

Myungshin Industry’s debt ratio is at a high level. As of the end of the first half of last year, it stood at 223.6%. The reliance on borrowings was also 138.9%. Net borrowings, which subtract cash equivalents from total borrowings, reached the 100 billion KRW level. Even adding the 24.4 billion KRW raised through the public offering at the end of last year, the debt ratio is expected to remain above 180%.

The high debt ratio is analyzed to be due to the issuance of convertible bonds and convertible preferred shares worth 80 billion KRW in 2018 and 2019. At that time, the company laid the foundation for global market entry through borrowing.

Fortunately, the debt ratio has been gradually decreasing as performance improves. Myungshin Industry’s debt ratio was 514.7% in 2018 and 360.5% in 2019. The reliance on borrowings also decreased from 348.4% to 138.9%. The debt ratio declined as capital increased with a net profit of approximately 34 billion KRW in 2019.

In the future, if convertible bonds and convertible preferred shares are converted into common stock, the debt ratio could decrease further. Currently, about 40 billion KRW of outstanding convertible bonds and convertible preferred shares remain. Before listing, at the end of March last year, 29 billion KRW of convertible preferred shares and 11 billion KRW of convertible bonds were already converted into common stock.

The conversion prices of these are around 3,355 to 3,506 KRW. Considering the recent stock price hovering around 40,000 KRW, it is expected that all will be converted into shares after the lock-up period ends. In this case, 11,691,960 shares will be newly released into the market, accounting for 22.3% of the current number of shares.

Meanwhile, these convertible bonds and convertible preferred shares have submitted a non-conversion commitment for six months. They may enter the market after June 7. At that time, 12,898,079 shares held by institutional investors will also have their lock-up lifted. Adding these together, the total freely tradable shares will increase from the current 24% to 57.9%.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}