Concerns Over High Refund Rate Mis-selling

Financial Services Commission Revises to Lower Standard Type Level

Exploitation of Sales by Encouraging Insurance Enrollment Before Revision

[Asia Economy Reporter Oh Hyung-gil] So-young Jo (pseudonym, 35), an office worker, recently hurriedly signed up for a children's insurance policy after hearing from an agent that "it will no longer be possible to subscribe to no-surrender refund type insurance" while researching insurance for her child.

Although there is no refund if canceled early, she was persuaded by the argument that it was the last chance to subscribe at a low premium. She said, "The agent said that as long as I don't cancel early, it would be beneficial, and that it would be discontinued in September," adding, "I don't quite understand why such an efficient insurance product is being discontinued."

As financial authorities announced revisions to no-surrender and low-surrender refund type insurance products, discontinued product marketing has been rampant in the insurance industry.

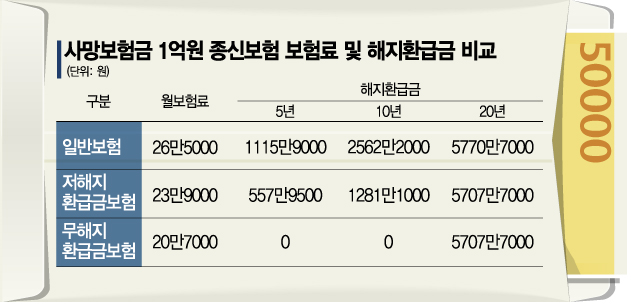

No-surrender and low-surrender refund type insurance offers the same coverage as standard insurance but features lower premiums in exchange for little or no refund upon early cancellation.

According to the insurance industry on the 3rd, just a week after the Financial Services Commission announced a draft amendment to the Insurance Business Supervisory Regulations to improve the structure of no-surrender insurance products, posts promoting discontinuation appeared on internet cafes, blogs, and social networking services (SNS).

Most of these posts urge people to subscribe by September, claiming "the amendment will take effect from October" or "due to the financial authorities' measures, the refund rate will become similar to that of general insurance products, causing no-surrender insurance to lose its advantages," implying that it will no longer be possible to subscribe.

Earlier, the Financial Services Commission announced that after review by the Ministry of Government Legislation and the Regulatory Reform Committee by the end of September, the amendment would be approved by the Financial Services Commission and implemented in October.

The amendment was made because no-surrender insurance was being disguised and sold as a savings product due to its high refund rate, raising concerns about consumer damage from early cancellations. The refund rate will be aligned with that of standard products.

However, the news of the amendment has led to untimely discontinued product marketing. A representative from an insurance general agency (GA) said, "There is no problem with sales until the authorities complete the amendment process," adding, "To explain the characteristics of no-surrender products, we have no choice but to mention the upcoming amendment and refund rates first."

The authorities' intention to fix the problem of emphasizing only the refund rate in sales is ironically being exploited for discontinued product marketing.

In the insurance industry, there are also criticisms that the measure caused confusion by not considering the characteristics of no-surrender insurance. A life insurance company official said, "The important point in choosing a no-surrender product is not the refund rate but that you can receive the same coverage at a low premium," adding, "Because the amendment did not consider consumers' needs to subscribe cheaply, discontinued product marketing inevitably emerged."

Meanwhile, financial authorities stated that they will continuously monitor discontinued product marketing before the implementation of the Insurance Business Supervisory Regulations and will actively respond if signs of incomplete sales or excessive competition are detected.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}