Ruling party signals Stock Price Suppression Prevention Act... Key battleground is inheritance and gift tax reform

Mandatory tender offers and stewardship code expected to strengthen minority shareholders

With amended Commercial Act set to take effect, a mountain of follow-up legislative tasks remains

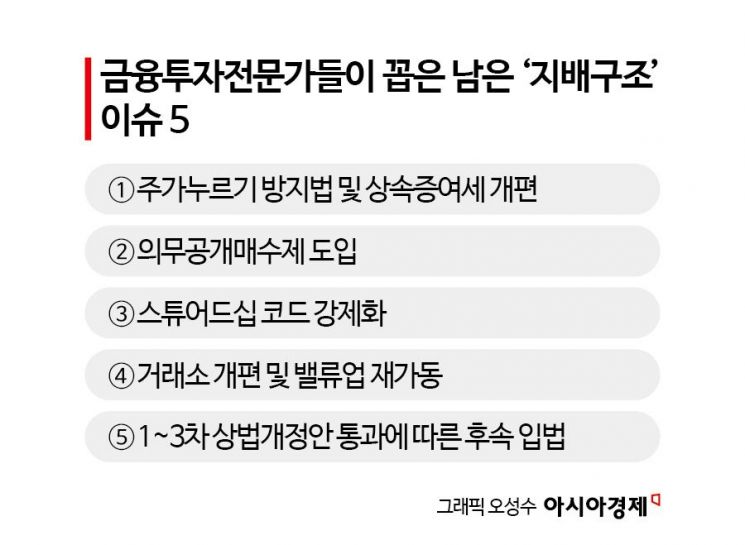

With the third Commercial Act amendment bill, centered on mandating the cancellation of treasury shares, passing the National Assembly plenary session on the afternoon of February 25, the market’s attention is now shifting to the remaining corporate governance agenda items. Following the so-called "Stock Price Suppression Prevention Act," major discussions are lined up on reforming inheritance and gift taxes, introducing a mandatory tender offer system, strengthening the stewardship code, and supplementing the Korea Exchange and the Value-Up program. With the full implementation of the amended Commercial Act, including the expansion of directors’ duty of loyalty, scheduled for the second half of this year, there are also many follow-up legislative tasks that urgently need to be completed.

Third Commercial Act amendment passes plenary session... Next major point of contention is 'taxation'

The first to third Commercial Act amendments, passed under the leadership of the Democratic Party, respectively focus on revising the basic framework of corporate governance by expanding the scope of directors’ duty of loyalty, mandating cumulative voting and expanding the separate election of audit committee members, and mandating the cancellation of treasury shares.

In the financial investment industry, the next biggest issue after the third Commercial Act amendment is taxation, especially the reform of inheritance and gift taxes. Under the current system, the application of premium valuation for controlling shareholders and other rules has repeatedly been criticized for creating an excessive tax burden in the process of business succession. Because of this, there has also been significant criticism that companies make distorted decisions, such as choosing internal reserves instead of increasing dividends or actively returning capital to shareholders. Lee Namwoo, Chairman of the Korea Corporate Governance Forum, pointed to taxation as a key corporate governance issue going forward, stressing that "tax policy is important" and that "beyond the Stock Price Suppression Prevention Act, what is ultimately needed is a rationalization of inheritance and gift taxes."

The Stock Price Suppression Prevention Act, in particular, is already under active policy drive. The core of the bill is that, for listed companies with a price-to-book ratio (PBR) below 0.8 times, inheritance and gift taxes will be levied not based on the market stock price but using the valuation method for unlisted companies (fair value assessment of assets plus earnings). President Lee Jaemyung reiterated his commitment to pushing this forward on this day as well, saying, "There is a mountain of work to do, including the Stock Price Suppression Prevention Act." The Democratic Party expects that, once the bill is implemented and the incentive to artificially depress stock prices for succession purposes disappears, companies with a PBR below 0.8 times will voluntarily move to boost their stock prices.

However, tax experts are also voicing caution. In the case of the Stock Price Suppression Prevention Act, they are concerned that PBR is not an absolute indicator and that the law could instead create side effects by encouraging more sophisticated tax-avoidance schemes. Accordingly, some argue that a predictable tax-rate framework is needed, including abolishing the premium for controlling shareholders, introducing conditional tax reductions for companies that expand long-term investment and dividends, extending installment payment periods, and allowing separate taxation of dividend income. If the first to third Commercial Act amendments are the "stick" regulating corporate governance, then inheritance and gift tax reform could serve as the "carrot" that reduces owners’ distorted decision-making. Park Hoon, a professor in the Department of Taxation at the University of Seoul, suggested that "easing the top marginal tax rate is a politically polarizing issue and will be difficult to pursue," but that "it could be an option to broadly remove measures such as the premium valuation for controlling shareholders, which have already been relaxed for small and medium-sized enterprises."

Regarding the introduction of separate taxation for dividend income, he also noted, "It is somewhat regrettable that a progressive tax rate is applied once income exceeds 20 million won," and diagnosed that "this is not simply a system that provides benefits to the wealthy but one that can offer a channel to return profits to all shareholders, so it needs to be improved in a direction that does not apply progressive taxation." Bold introduction of separate taxation for dividend income has been cited as a factor that could eliminate the incentive for major shareholders to maintain opaque corporate governance structures.

Mandatory tender offers and stewardship code expected to strengthen 'minority shareholders'

In addition, the Democratic Party has already flagged the strengthening of minority shareholders’ rights through a mandatory tender offer system and the stewardship code as its next tasks. Kim Namgeun, a member of the Democratic Party’s Special Committee on K-Capital Markets, appeared on a YouTube radio program on this day and said, "Minority shareholders cannot freely make their own proposals at general shareholders’ meetings. We need to make sure that shareholders’ intentions are reflected so that (controlling shareholders) cannot exercise unchecked power." Shin Jangshik, a lawmaker of the Cho Kuk Innovation Party, also emphasized that the next step after the Commercial Act amendments is "to continuously enhance the rights of retail investors and level the tilted playing field. The key direction going forward is how to strengthen the rights of minority shareholders."

The introduction of a mandatory tender offer system is evaluated as a mechanism to enhance fairness in the process of transferring control. The idea is that when a controlling shareholder sells shares at a control premium, minority shareholders must also be guaranteed the opportunity to sell under the same conditions. To achieve this, an amendment to the Capital Markets Act is required. Strengthening the stewardship code, which promotes responsible investment by institutional investors, is also seen as a mechanism that can protect minority shareholders. Given that the code has repeatedly been embroiled in debates over its effectiveness, further discussions are inevitable. Chairman Lee noted, "The current stewardship code is a soft norm, and compliance is not a legal obligation," adding, "Some argue that it should be elevated to a legal obligation and that the Financial Supervisory Service should be tasked with monitoring compliance." Debates over the structure of how the National Pension Service exercises its voting rights are also expected to reignite. In the market, there is discussion of adopting a Japanese-style model in which voting rights are delegated to external asset managers.

Alongside these issues, the restructuring of the Korea Exchange and the reactivation of the corporate Value-Up program are also drawing market attention. Analysts warn that, as the Lee Jaemyung administration’s capital market reform moves into its second phase, if the exchange fails to function properly, it will be difficult for the amended Commercial Act to take root. Among experts, there are also arguments that the Value-Up policy, which has so far been limited to voluntary recommendations, should be given some degree of binding force.

Voices are also emerging that stress the need for swift progress on follow-up legislative tasks after the first to third Commercial Act amendments. Cheon Junbeom, managing partner at Wise Forest, said, "There are an enormous number of minor follow-up legislative tasks still remaining," and pointed out that "the most urgent work is to clearly define merger ratios under the Capital Markets Act based on fair value and to fill the gaps related to cash-settled comprehensive share exchanges under the Commercial Act." He explained that, for the Commercial Act amendments to be more than just declarations, follow-up measures that ensure consistency with the Capital Markets Act are essential. Hwang Hyunyeong, a research fellow at the Korea Capital Market Institute, likewise suggested that "follow-up legislation in line with the Commercial Act amendments must also be put in place."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}