Private credit heavily concentrated in AI industry

Without proof of growth and profitability, fears of loan distress may rise

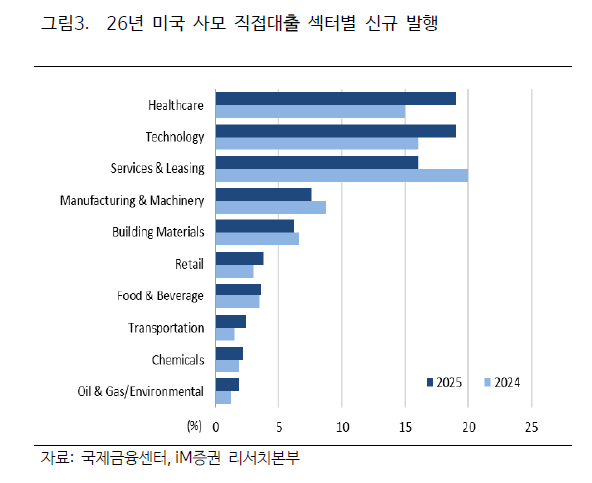

Concerns over potential distress in the U.S. private credit market are proving persistent. Analysts note that lending has been heavily concentrated in the healthcare and technology sectors, and in particular that loans have surged alongside the boom in AI investment. While this may not trigger major problems immediately, the worry is that if controversy over the profitability of AI investments grows, fears of credit deterioration could spread further.

As funds rush into private credit, concerns are rising

On the 24th, iM Securities cited the debate over the profitability of AI investments as the biggest factor behind concerns about distress in the U.S. private credit market. U.S. big tech companies such as Google, Microsoft (MS), Meta, and Amazon are making massive investments in the AI field. To secure the large-scale funding needed, they are even ramping up corporate bond issuance. In addition, unicorn-level unlisted companies such as OpenAI are also raising large amounts of capital, drawing market liquidity into the AI space.

At the same time, controversy over AI profitability is emerging due to the lack of services that are clearly “making money.” Liquidity is being funneled into AI, but substantial value added has yet to be fully created, which is fueling concern. Even though liquidity remains abundant, the atmosphere is one of growing credit squeeze worries, especially as the U.S. Federal Reserve is increasingly expected to maintain its rate-hold stance.

Park Sanghyun, a researcher at iM Securities, assessed that concerns over distress in private credit reflect this broader mood. At the end of last year, the back-to-back bankruptcies of U.S. auto lender Tricolor Holdings and auto parts maker First Brands brought the issue of overlapping collateral in private credit to the surface. More recently, a private credit fund managed by BlackRock marked down the value of some of its investment assets, while Blue Owl Capital halted redemptions in one of its private credit funds, developments that many see as flashing early warning signs of a credit squeeze.

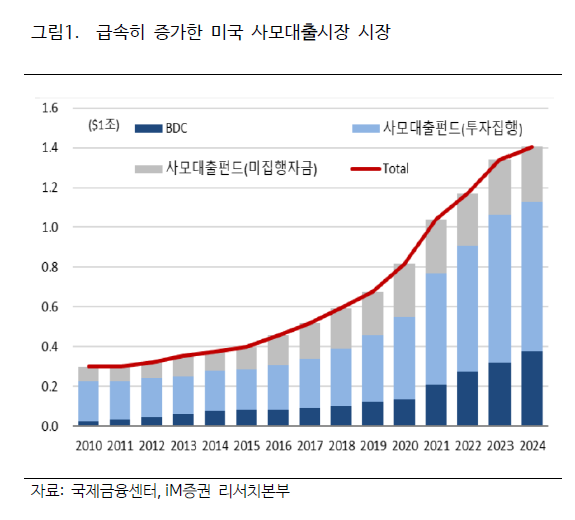

Although it is not yet a situation in which credit concerns are spreading across the board, he stressed that the risk of distress in the private credit market still needs to be closely watched. Given the rapid growth of the market, there is concern that if distress does occur, it could appear in a chain reaction. Park noted, “The U.S. private credit market is concentrated in the healthcare and technology sectors and has grown rapidly, particularly alongside the AI investment boom,” adding, “The Bank for International Settlements (BIS) expects the outstanding amount of private credit to AI-related companies to increase from the current level of around 200 billion dollars to between 300 billion and 600 billion dollars by 2030.”

Distorted default rates, double collateral issues... links to financial institutions also a concern

iM Securities pointed first to the underestimation of default rates as the primary latent risk in the private credit market. Park said, “As of the fourth quarter of last year, the default rate in the private credit market was only 2.46%, but the consensus is that the true default rate is higher than that,” and added, “Because of the opacity of private credit and other factors, there is a high possibility that default statistics are being underestimated or distorted.” He particularly highlighted the use of payment-in-kind (PIK) options. PIK is a method in which interest, dividends, and principal are paid not in cash but in the form of bonds, stocks, or inventory, among others. A rising share of loans utilizing PIK suggests that the hidden scale of distress in the private credit market could be larger than it appears.

He also noted that private credit relies more on the internal models of individual institutions than on external standards and recognized methodologies when valuing assets. This has drawn criticism that the market is not free from the risk of overstating asset values.

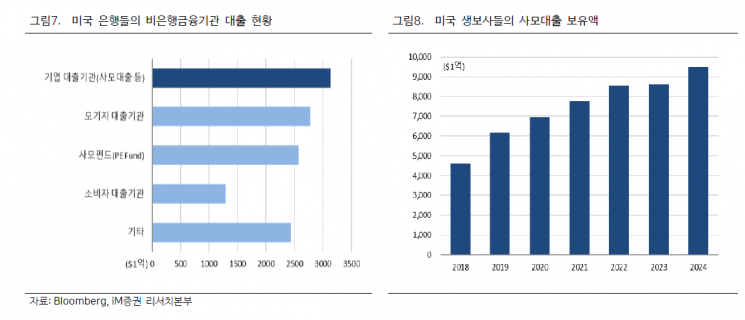

Deepening interconnectedness with banks and insurers was also cited as a potential risk. The concern is that distress in the private credit market could be transmitted to financial institutions. Park warned, “Given the experience of the subprime mortgage crisis, there may be derivatives held by banks and insurance companies that are linked to private credit,” and added, “The exposure of U.S. financial institutions to the private credit market could be larger than is currently known.”

The key is AI industry profitability... if it is not proven, contagion fears may grow

Ultimately, he stressed that everything comes back to the profitability of AI investments. Because the AI industry, which accounts for the largest share of the private credit market, still has high growth potential, the view is that it is unlikely to trigger a major credit shock in the near term. However, he pointed out that if the profitability of AI, which is already being questioned in some quarters, fails to be demonstrated, concerns about distress could grow. He also emphasized that the process of separating winners from losers among AI companies itself represents a potential risk factor.

Park warned, “The AI industry has strong growth prospects, but not every company will survive. If some big tech firms fall behind in the competition for survival, and if bankruptcies among small and mid-sized AI companies increase, that will be a negative for the private credit market,” adding, “The AI industry could enter a phase of taking a breather or of sorting the wheat from the chaff, and in that case, the risk of distress in the structurally vulnerable private credit market could materialize.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}