Concerns Grow Over Specialized Credit Finance Bond Yields Entrenching Above 3%

Bank of Korea Unlikely to Cut Rates Soon

Diversification of Funding Sources Urgent Amid Prolonged 'Lean Period'?ABS and ESG Bonds in Focus

Card Companies Must Accelera

Credit card companies are maintaining a conservative management approach focused on cost control. This is due to expectations that the Bank of Korea will keep its base interest rate unchanged for an extended period, leading to continued high yields-above 3%-on bonds issued by specialized credit finance companies (known as “Yejeonchae”), which are a primary funding source for card issuers. Experts advise that card companies should diversify their funding channels, such as by utilizing overseas asset-backed securities (ABS) or ESG (environmental, social, and governance) green bonds, in order to reduce their reliance on Yejeonchae.

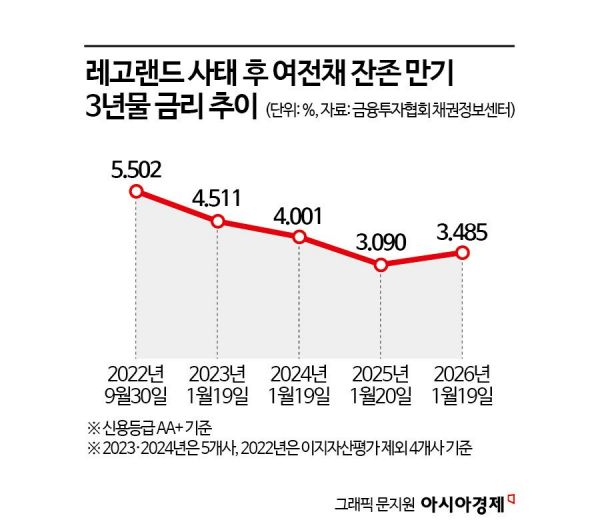

According to the financial sector and the Korea Financial Investment Association on January 20, the previous day’s average market yield for three-year Yejeonchae bonds (with a credit rating of AA+) was 3.485%, up 38.2 basis points (1bp=0.01 percentage points) from the same period last year. The yield on Yejeonchae bonds soared to the mid-5% range during the Legoland default incident at the end of the third quarter of 2022, then stabilized to the high-2% range by the end of the third quarter last year. However, since late last year, yields have risen again to the low-3% range, and, following recent hawkish (monetary tightening) remarks from the Bank of Korea, have climbed to the mid-3% range. Previously, on January 15, the Bank of Korea signaled its intention to maintain a rate freeze by removing references to a possible rate cut from its monetary policy decision statement.

Card Companies Without Deposit Functions Face a Vicious Cycle of Profitability Concerns Amid Rising Interest Rates

The card industry believes that, given unstable real estate prices and a weak won (high exchange rate), the likelihood of the monetary authorities lowering rates in the near future is limited. There is particular concern that Yejeonchae yields may become entrenched in the mid-3% range or even return to the 4% range.

Unlike banks, card companies do not have deposit-taking functions and thus raise most of their funds by issuing Yejeonchae bonds. With these funds, they pay merchants in advance and later collect payments from consumers to repay bond interest. Therefore, when funding costs rise, not only does profitability deteriorate, but overall business operations can also contract, creating a vicious cycle.

On top of this, card companies are struggling to secure new growth drivers, falling behind banks and fintech (finance + technology) industries in future-oriented businesses such as stablecoins. An industry insider stated, “With funding costs rising and a lack of revenue sources, there is no alternative but to pursue austerity management.” Some also point out that regulatory tightening by financial authorities-such as including card loans in the total debt service ratio (DSR) regulations last year-is further deteriorating the business environment for card companies.

“Diversifying Funding Sources Through ABS and Overseas Bonds Is Essential”

Experts note that since it is unlikely that merchant fee rates will be lowered or household loan regulations will be eased, card companies must diversify their funding sources on their own. By issuing ABS or ESG green bonds to decrease dependence on Yejeonchae, they can secure the capacity to focus on developing innovative products to discover new businesses and increase credit sales.

Industry activity is accelerating as well. Just the previous day, Hyundai Card issued a “Kimchi Bond” (a foreign currency-denominated bond issued in Korea) worth 20 million dollars (approximately 29.4 billion won), and more specialized credit finance companies are tapping into overseas bond markets.

Suh Jiyong, President of the Korea Society of Credit Card Studies and Professor at Sangmyung University’s School of Business Administration, explained, “If a company issues bonds overseas during a period of rapid currency depreciation and converts the dollars into won, it increases demand for the won, which can help strengthen the currency.” He added, “Regulators are also more likely to take a favorable view of overseas issuance, rather than restricting it due to exchange rate risk as in the past.” Professor Suh emphasized, “Card companies should actively secure alternative funding sources beyond Yejeonchae by leveraging these macroeconomic conditions.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}