Korea Social Investment Forum Releases Report on the 27th

"Significantly Lower Than the Global Average Score of 4.7 for Major Insurers"

"Funds Withdrawn from Fossil Fuel Finance Not Redirected to Renewable Energy"

An analysis has found that the climate risk management levels of major domestic insurance companies show a significant gap compared to the global average.

According to the "2024 Korea Scorecard" published by the Korea Social Investment Forum (KoSIF) on the 27th, the climate risk management score of domestic insurance companies was 0.9 out of 10. This is significantly lower than the average score of 4.7 for 10 major global insurance companies.

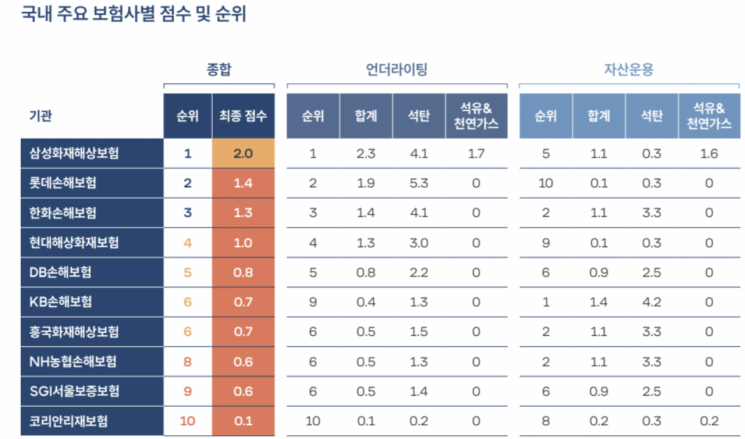

KoSIF conducted a comprehensive evaluation and analysis to assess insurance companies' policies related to fossil fuels and their climate risk response. The evaluation covered whether there are underwriting and asset management restriction policies for fossil fuel business projects, phased reduction plans aimed at phasing out fossil fuels, and the current status of greenhouse gas emission reduction targets. The scores were based on data obtained through the Financial Supervisory Service and the office of National Assembly member Kim Hyunjung, evaluating 10 major domestic insurance companies (Samsung Fire & Marine Insurance, DB Insurance, Hyundai Marine & Fire Insurance, KB Insurance, Heungkuk Fire & Marine Insurance, NH NongHyup Property & Casualty Insurance, Hanwha General Insurance, Lotte Insurance, SGI Seoul Guarantee Insurance, and Korean Reinsurance).

The average score for domestic insurance companies was 1.0 for underwriting (insurance risk assessment) and 0.8 for asset management. Among the companies, Samsung Fire & Marine Insurance received the highest score at 2.0, followed by Lotte Insurance (1.4) and Hanwha General Insurance (1.3). Korean Reinsurance had the lowest score at 0.1.

Domestic insurance companies are only restricting new coal-fired power plants or applying policies on a project basis, so insurance for existing clients or entire companies remains unchanged. As a result, the actual effect of these restrictions is minimal. Many financial institutions have not yet established fossil fuel policies that also cover oil and natural gas.

In contrast, major global insurance companies are implementing phase-out policies for fossil fuels that cover the entire value chain of coal, oil, and gas, including not only new contracts but also existing holdings. They apply restrictions at the client or company level, thereby increasing transition pressure at the portfolio level, according to KoSIF's analysis.

Exception clauses are also pointed out as a problem. All 10 domestic insurance companies have policies restricting new coal underwriting, but six of them include exception clauses. Some companies allow operational insurance and increases or extensions of existing contracts, as well as insurance for ancillary facility construction, citing risk diversification for hedging purposes or maintaining existing contracts. This is seen as greatly undermining the effectiveness of coal restriction policies. There are also no withdrawal plans or phased reduction roadmaps for existing coal insurance contracts, which stands in stark contrast to global insurance companies such as Allianz and AXA, which have set coal phase-out deadlines of 2030 for OECD countries and 2040 globally.

According to the report, the global insurance industry has suffered losses of about $600 billion (approximately 837 trillion won) due to climate change over the past 20 years. The damage is also severe in Korea. The payout for crop disaster insurance, a representative disaster insurance product, exceeded 1 trillion won in 2023 and reached 1.017 trillion won last year. It is expected to surpass 1 trillion won again this year. Nevertheless, support for fossil fuel insurance by domestic insurance companies is actually expanding. As of June last year, the balance of fossil fuel insurance was 182.7 trillion won, up 30.7% from the same period the previous year, showing a clear divergence from the coal phase-out policy direction.

Support for renewable energy is virtually stagnant. In the first half of last year, the insurance coverage provided by insurance companies for renewable energy projects was 24.8 trillion won, only 13.6% of the 182.7 trillion won fossil fuel insurance balance. Investment funds withdrawn from fossil fuel finance are not being redirected to renewable energy, so there is no substantial asset reallocation to support the energy transition. In the first half of last year, the balance of fossil fuel finance investments was 12.4 trillion won, down 5.6% compared to 2022. During the same period, the balance of new and renewable energy finance investments was 4.4 trillion won, an increase of only 2.3%. New funding for renewable energy decreased from 400 billion won in 2023 to 100 billion won in the first half of last year, showing a declining trend.

Kang Yunseo, a researcher at KoSIF, said, "The climate risk response of domestic insurance companies remains at a declarative level," adding, "It is necessary to expand the scope of coal policies to include not only power generation but also metallurgical coal, address the blind spots of high-carbon industries, establish a comprehensive risk management system that includes oil and natural gas, and set sustainable energy investment goals in order to drive structural transition."

Climate risk management scores and rankings by insurance company from the "2024 Korea Scorecard" published by the Korea Social Investment Forum (KoSIF) on the 27th. KoSIF

Climate risk management scores and rankings by insurance company from the "2024 Korea Scorecard" published by the Korea Social Investment Forum (KoSIF) on the 27th. KoSIF

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}