Hyosung Chemical and Others Producing Propylene Without NCC

Rising Debt and Shrinking Margins; Taekwang Industrial Halts Plant Operations

SK Advanced Faces Poor Performance and Debt Ratio of 241%

Propane Dehydrogenation (PDH) facilities, which produce propylene from propane gas instead of using Naphtha Cracking Centers (NCC), have significantly lost cost competitiveness over the past two years. Propylene is a fundamental raw material for polypropylene (PP), a synthetic resin. Since PDH facilities produce only propylene, they are more vulnerable to market fluctuations. Industry voices are now calling for restructuring in the petrochemical sector to include not only NCCs but also specialized facilities like PDH plants focused on specific products.

According to semiannual reports from each company as of August 18, PDH-focused companies without NCCs are experiencing common performance pressures. Hyosung Chemical is maintaining liquidity through capital injections from its parent company, Hyosung, while Taekwang Industrial has completely halted PDH operations. SK Advanced is facing increasing financial strain due to expanding losses and a debt ratio that has surpassed 240%.

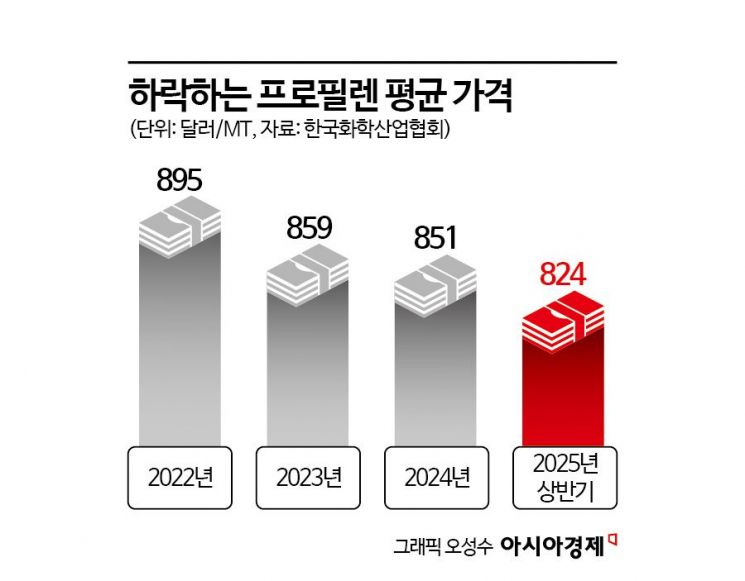

PDH was previously considered to have greater cost competitiveness than NCC in propylene production. However, a recent rise in propane feedstock prices, coupled with a decline in propylene prices, has sharply reduced the spread (margin). International propane prices have remained at $600-700 per ton, while Asian propylene prices fell from $1,000 per ton in 2023 to $876 per ton as of June this year. As a result, the margin, after accounting for additional costs, has dropped to below $50 per ton, and at times has even turned negative.

The structural burden has been exacerbated by increased propylene supply, especially from China. As of last year, China’s propylene production capacity reached approximately 50 million tons, of which 16 million tons came from PDH facilities. With several million tons of new capacity being added each year, global oversupply has become entrenched.

Hyosung Chemical’s poor performance has been aggravated not only by its domestic operations but also by its PDH facility in Vietnam. Since 2017, Hyosung Chemical has invested a total of 1.3 trillion won to construct PDH and PP facilities in stages, each with an annual capacity of 600,000 tons, and began commercial operations in 2021. However, during this large-scale investment, its borrowings surged, with total debt exceeding 6 trillion won by the end of 2022 and annual interest expenses alone surpassing 300 billion won. The average plant operating rate has continued to decline, from 85.6% in 2023 to 76.6% in 2024, and to 68.8% in the first half of this year.

As a result, Hyosung Vina Chemicals, Hyosung Chemical’s Vietnamese subsidiary, entered into debt guarantee and capital replenishment agreements totaling 300 billion won this past May, and on July 30, decided on an additional debt guarantee of 170 billion won. At the end of last year, Hyosung Chemical fell into a state of complete capital erosion and managed to defend its liquidity only by selling its specialty gas business unit to its affiliate, Hyosung TNS. This year as well, the company is repeating a structure in which it cannot survive independently without parent company guarantees and capital injections.

SK Advanced’s losses have widened. Established as a physical spin-off of SK Gas’s PDH division, SK Advanced is jointly owned by SK Gas (45%), Saudi Arabia’s AGIC (30%), and Kuwait’s PIC (25%), and operates PDH and PP facilities in Ulsan with annual capacities of 700,000 tons and 600,000 tons, respectively. In the first half of this year, SK Advanced posted an operating loss of 129.7 billion won, a 36% increase compared to the same period last year (95.2 billion won). The debt ratio also rose from 212% last year to 241% this year, raising further concerns about financial soundness.

Taekwang Industrial completely halted operations of its PDH facility in Ulsan, which has an annual capacity of 300,000 tons, earlier this year due to deteriorating profitability. All these companies face the dual challenges of high debt and low margins, making fundamental recovery of competitiveness difficult.

An industry insider commented, "Until 2023, we benefited from the influx of cheap propane from U.S. shale gas, but recently, more of that supply is being consumed within the United States. Since PDH is a single-process facility for propylene, it is even harder to respond when the market turns unfavorable."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}