Bank of Korea's "2024 Payment and Settlement Report"

Caution Needed for Side Effects in Cross-Industry Operations

Prolonged Settlement Cycles as a Form of Interest-Free Borrowing

System Improvements Needed to Prevent Similar Damages in Advance

In the 'Timon-Wemakeprice (T-Mep) settlement payment default incident,' the practice of extending the settlement cycle for sales payments and holding funds internally for an extended period has been characterized as a form of fundraising (interest-free borrowing). Experts have warned that similar issues could arise in other sectors such as delivery agency and accommodation reservation services, and have advised caution. They emphasized the need to preemptively block potential consumer damages by checking for possible misappropriation of customer funds and verifying payment capabilities.

On April 21, the Bank of Korea stated this in its '2024 Payment and Settlement Report,' specifically in the section titled 'Directions for Institutional Improvement and Implications Following the Timon-Wemakeprice Incident.'

In July of last year, T-Mep, an e-commerce and electronic payment gateway (PG) platform, failed to pay settlement funds to its registered sellers. As of August last year, the total unpaid settlement amount to sellers was estimated at 1.3 trillion won, and the number of affected businesses was estimated at 48,000. By industry, the largest losses were seen in digital and electronics (29.0%), gift certificates (25.2%), and food (10.0%). More than half of the unpaid settlement funds (675.9 billion won, 52.9%) were concentrated among 74 companies.

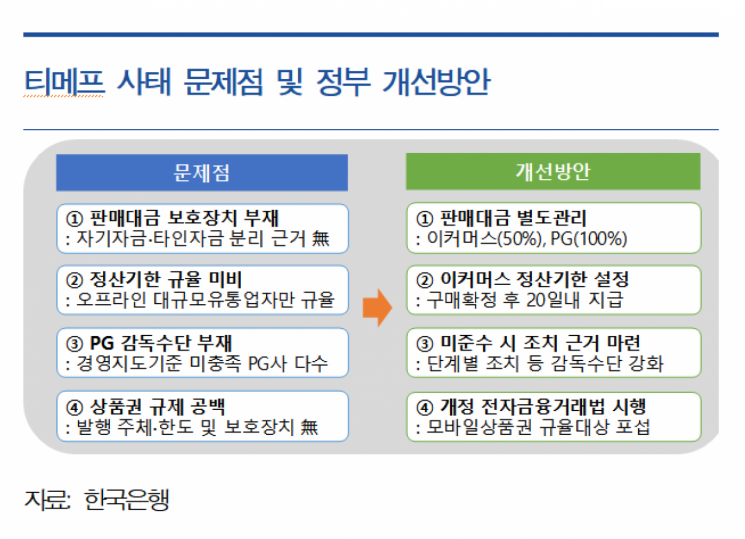

The Bank of Korea identified several institutional issues, including the lack of safeguards for sales payments, insufficient regulation of settlement deadlines, lack of supervisory tools for PG companies, and regulatory gaps concerning gift certificates. The first problem cited was the absence of protection measures for sales payments in relevant laws such as the Distribution Industry Development Act and the Electronic Financial Transactions Act. In response, the government plans to amend these laws to impose separate management obligations on e-commerce companies (under the Distribution Industry Development Act) and PG companies (under the Electronic Financial Transactions Act), requiring them to manage sales payments (unsettled funds) through escrow, trust, or payment guarantee insurance. The amendments will also prohibit the transfer, provision as collateral, or third-party seizure and set-off of separately managed funds.

The Bank of Korea also pointed out that, currently, only offline large-scale distributors are subject to settlement period regulations, and there are no such regulations for e-commerce companies or PG companies, which needs to be addressed institutionally. The government is pushing to amend the Distribution Industry Development Act and the Electronic Financial Transactions Act to require e-commerce companies to settle sales payments within 20 days after purchase confirmation, and to require PG companies to settle sales payments within the contractually agreed period.

There is also no supervisory mechanism to compel PG companies to comply with management guidance standards if they fail to do so. Accordingly, the supervisory authorities plan to revise relevant supervisory regulations so that, if a PG company fails to comply with management guidance standards or the obligation to separately manage settlement funds, they can implement step-by-step measures such as corrective orders, business suspension, and registration cancellation.

Another issue identified was that, following the abolition of the Gift Certificate Act in February 1992, restrictions on issuers and limits for gift certificates were removed, and there were no safeguards for user deposits (funds paid to purchase gift certificates). However, with the revision of the Electronic Financial Transactions Act in September last year, most mobile gift certificates are now regulated, requiring separate management of user deposits through external escrow, trust, or payment guarantee insurance. Issuing gift certificates at a discount or providing rewards is now only permitted if financial soundness requirements are met, thereby strengthening regulations.

A Bank of Korea official stated, "This incident is an example of an e-commerce (industry) and PG (finance) combination, where an e-commerce company's insolvency was addressed using PG sales payments. With the recent rise of big tech and the acceleration of digital transformation, the boundaries between industries are rapidly becoming blurred, so it is important to pay attention to potential side effects that may arise during cross-industry business operations."

It has been pointed out that T-Mep's practice of extending the settlement cycle for sales payments and holding significant funds internally was a form of fundraising (interest-free borrowing), and that similar problems could occur in other sectors such as delivery agency and accommodation reservation services. A Bank of Korea official stated, "Efforts to improve the system must continue to preemptively block the possibility of damage to consumers and service providers by checking for possible misappropriation of customer funds and verifying payment capabilities." The official also emphasized, "The Bank of Korea will strengthen monitoring and analysis in this sector by exercising its authority to request data from electronic financial businesses and PG companies that issue prepaid electronic payment instruments."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}