Despite Bank of Korea's Rate Cuts,

Mortgage Interest Rates Remain High

Benchmark Rates Drop to Mid-3% Range

Widened Spread Between Additional and Preferential Rates Persists

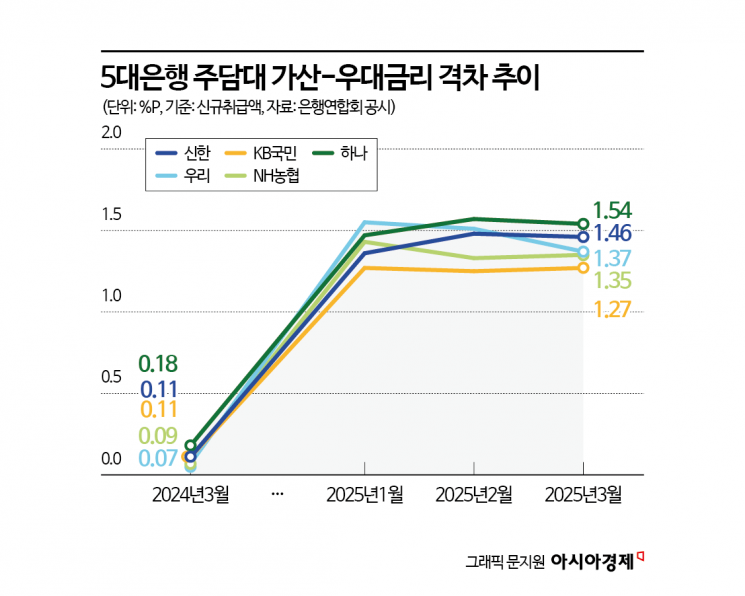

Spread Jumps from 0.09-0.18% to 1.27-1.54% in One Year

Although the Bank of Korea has entered a rate-cutting phase by lowering the base interest rate three times since October last year, the interest rate barrier perceived by consumers remains high. The average mortgage loan interest rates at the five major commercial banks have stayed in the 4% range despite the rate cuts, declining slowly. While benchmark interest rates (such as COFIX and 5-year financial bonds) have fallen in response to the base rate cuts, the spread between the banks' discretionary additional interest rates and preferential rates remains in the low to mid 1% range.

On the 18th, the average mortgage loan interest rates at the five major commercial banks (KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup) for last month were between 4.27% and 4.52% per annum. The average loan interest rate across the five banks is estimated at about 4.39%. This is lower than the February average of 4.44%, but still higher than the average of 3.95% in October last year when the Bank of Korea began cutting the base rate. Despite the base rate cuts, mortgage loan interest rates have actually risen and are declining slowly.

Generally, mortgage loan interest rates are determined by adding an additional interest rate to benchmark rates such as COFIX and 5-year financial bonds, then subtracting preferential rates. While benchmark rates move in tandem with the base rate, the additional and preferential rates are largely at the banks' discretion.

The downward trend in benchmark interest rates (market rates) has become clear before and after the base rate cuts. In fact, COFIX (newly handled amount), as announced by the Banks Association, fell continuously for six months from 3.3% in November last year to 2.84%. According to the Korea Financial Investment Association, the 5-year financial bond (AAA) also dropped from 3.089% at the end of December last year to 2.797% as of the 17th. The base rate reflected by banks also fell from the mid-3.2% range to 2.98%. The fact that the lowest mortgage loan interest rate fell to the mid-3% range this month is also due to the decline in benchmark rates.

Despite the decline in benchmark rates linked to the base rate, the perceived interest rate remains high due to the spread between additional and preferential rates. To manage the total volume of household loans, banks artificially raised additional interest rates and lowered preferential rates from the fourth quarter of last year, widening the spread. Although there has been a trend of lowering additional rates since the beginning of the year, the reduction has been slight, and the widened spread between additional and preferential rates has hardly decreased.

According to the Banks Association, the spread between additional and preferential rates at the five major banks last month remained between 1.27% and 1.54%. Even though banks have partially lowered additional rates, preferential rates have also decreased, maintaining the spread in the low to mid 1% range. In March last year, the spread was between 0.09% and 0.18%.

A representative from a commercial bank said, "The guideline to manage the total volume to prevent the base rate cuts from leading to a surge in household loans is still valid," adding, "It is true that banks find it difficult to find ways to manage the total loan volume other than raising the hurdle for loans themselves or not lowering interest rates."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}