MBK Partners has warned that Chairman Choi Yoon-beom's open tender offer for treasury shares could cause significant damage to both the company and the remaining shareholders of Korea Zinc.

On the 4th, MBK stated, "Chairman Choi Yoon-beom's open tender offer for treasury shares, financed by a high-interest loan of up to 7% amounting to 2.7 trillion KRW, faces legal risks such as breach of trust, and from both monetary and financial perspectives, it will cause considerable harm not only to Korea Zinc but also to the remaining shareholders."

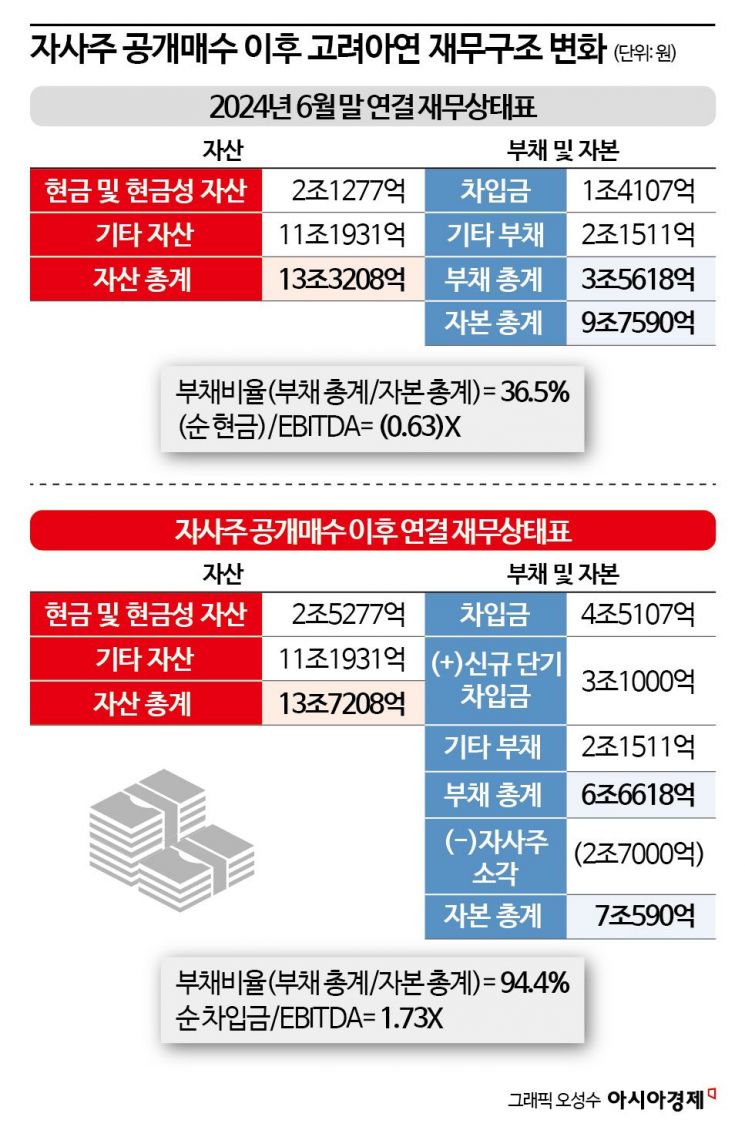

First, they explained that acquiring treasury shares on such a large scale of 2.7 trillion KRW would reduce Korea Zinc's net assets by about 27%. According to Korea Zinc's consolidated financial statements as of the end of the first half of 2024, net assets (total equity) are approximately 9.8 trillion KRW. After the treasury share acquisition, net assets would shrink to 7.1 trillion KRW. A decrease in net assets means that the shareholders' portion of the corporate value is reduced accordingly.

Korea Zinc's debt ratio will rise sharply.

At the end of this half-year, Korea Zinc's debt ratio was 36.5%, but according to a recent disclosure regarding the financing for the open tender offer for treasury shares, borrowings increased by 3.1 trillion KRW (400 billion KRW from commercial paper issuance + 2.7 trillion KRW loan) compared to the half-year end, pushing the debt ratio close to 95%. The 'net debt/EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization)' is also expected to rise to 1.73 times. In this case, Korea Zinc will significantly exceed the credit rating agencies' downgrade review criteria of 'net debt/EBITDA being 0 or below 0.5 times,' meaning Korea Zinc will have to prepare for the possibility of a credit rating downgrade.

With the total borrowings increasing to 3.1 trillion KRW, including the 2.7 trillion KRW loan for the open tender offer, the additional interest expense alone is expected to be about 186 billion KRW, which will reduce Korea Zinc's net profit by the same amount. Although Korea Zinc had a net cash position as of the end of the first half of this year based on consolidated financial statements, if most of the 2.7 trillion KRW loan is spent on acquiring treasury shares, Korea Zinc is expected to immediately shift to a net debt position of about 2 trillion KRW.

MBK pointed out that the problem is that the company's monetary and financial damages will be directly passed on to the remaining shareholders.

On a consolidated basis, Korea Zinc's net income for the twelve months ending at the end of the first half of 2024 is approximately 559 billion KRW. Considering the current total number of issued shares of 20,703,283, the earnings per share (EPS) is 26,985 KRW.

Due to the increase in borrowings by 3.1 trillion KRW, the additional estimated interest expense of about 186 billion KRW will reduce net income to approximately 413 billion KRW. Taking into account the reduction of 3,209,009 shares through treasury share cancellation, the EPS will decrease by about 12.5% to 23,624 KRW. MBK explained that this means the value of the shares held by the remaining shareholders is damaged accordingly.

The value of the shares held by the remaining shareholders will also decline based on book value per share (BPS).

Korea Zinc's consolidated net assets (total equity) as of the end of the first half of 2024 are 9.8 trillion KRW. Considering the current total number of issued shares of 20,703,283, the BPS is 471,374 KRW. After a capital reduction of 2.7 trillion KRW due to treasury share acquisition and a decrease of 3,209,009 shares due to treasury share cancellation, the BPS will fall by about 14.0% to 405,591 KRW.

Furthermore, MBK predicted that acquiring a large amount of treasury shares with a 2.7 trillion KRW loan will also impose difficulties on Korea Zinc's plans to secure approximately 14 trillion KRW in investment funds over the next five years (of which 12 trillion KRW is for Troika Drive), potentially negatively impacting the company's growth prospects. MBK concluded, "Chairman Choi Yoon-beom's open tender offer for treasury shares to defend his personal management rights will boomerang, damaging Korea Zinc's corporate value and shareholder value."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}