'CP+Dankisachae' 50 billion to 840 billion in one year

'Heavy tail' ship payment structure increases working capital burden

3.6 trillion short-term debt repayment and refinancing burden within one year

"Short-term borrowings expected to decrease as cash flow improves"

Samsung Heavy Industries is raising funds by issuing short-term commercial paper (CP, including short-term bonds) with maturities of less than one year. After securing liquidity by issuing private bonds for several years, the method of fundraising changed last year. It is analyzed that the company increased short-term financing due to the sharp rise in ship orders, which significantly increased working capital burdens, as well as the concentrated repayment burden of borrowings.

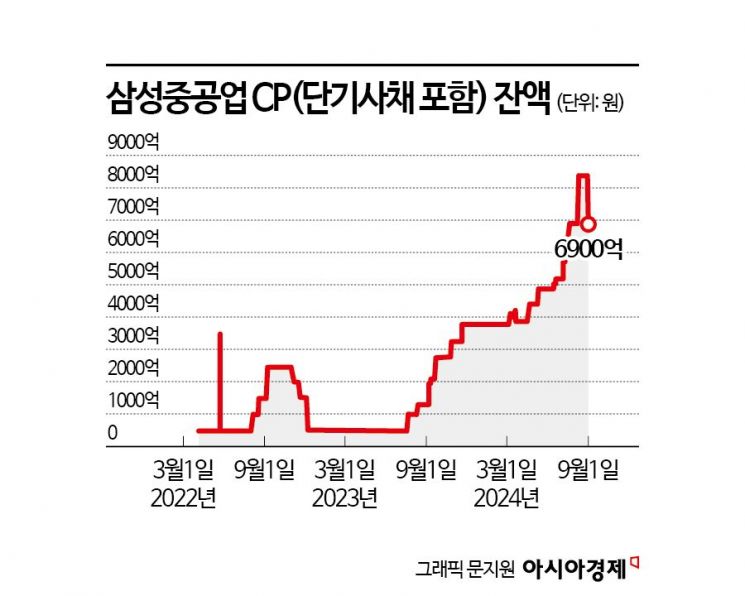

According to the investment banking (IB) industry on the 5th, Samsung Heavy Industries has been increasing its CP balance since last year. The amount of CP issuance, which was only about 50 billion KRW until June last year, has increased to 840 billion KRW recently through repeated issuance and repayment. After repaying 150 billion KRW of CP that matured on the 30th of last month, the current balance stands at about 690 billion KRW.

The company is not issuing private bonds, which had been a major fundraising method. Since Samsung Heavy Industries’ credit rating fell to BBB+ in March 2017, it has not issued public bonds. Until last year, it mainly issued private bonds. Starting with 255 billion KRW in 2017, it issued around 200 billion KRW of private bonds annually on average until last year. However, it has not issued private bonds for over a year since May last year.

As Samsung Heavy Industries raises funds on a short-term basis, the burden of repaying short-term borrowings has increased. As of the end of the first half of this year, short-term borrowings and long-term liabilities due within one year (long-term borrowings to be repaid within one year) have grown to about 3.6 trillion KRW. This is an increase of about 900 billion KRW from 2.7 trillion KRW in the first half of last year.

The IB industry views the increase in Samsung Heavy Industries’ short-term borrowings as paradoxically related to the rise in orders. As of the end of March this year, Samsung Heavy Industries’ order backlog reached 33 trillion KRW, centered on its main ship types, liquefied natural gas (LNG) carriers and container ships. This has rapidly increased from about 12 trillion KRW at the end of 2020.

However, the payment terms for ship financing are structured as a so-called ‘heavy tail,’ where more than 50% is received at the time of ship delivery. Since the proportion of down payments and interim payments is low, the costs invested in shipbuilding must rely on external funds, inevitably increasing the working capital burden.

Moreover, Samsung Heavy Industries’ credit rating has not improved enough to issue long-term public bonds. In June this year, its credit rating was raised from BBB to BBB+, and its short-term credit rating was upgraded from A3 to A3+. The reason for switching to CP, which has relatively lower interest costs, is also because the interest rates on private bonds have risen compared to the past.

An IB industry official said, "With a rich order backlog, cash flow is expected to steadily improve during the shipbuilding process," adding, "It seems that the company will first borrow short-term funds with relatively low interest rates and then reduce short-term borrowings by repaying them when shipbuilding payments are received."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}