Financial Supervisory Service to Disclose 'Status of Non-Performing Loans of Domestic Banks' on 28th

NPL Ratio Rises by 0.03 Percentage Points to 0.53% Compared to Previous Quarter

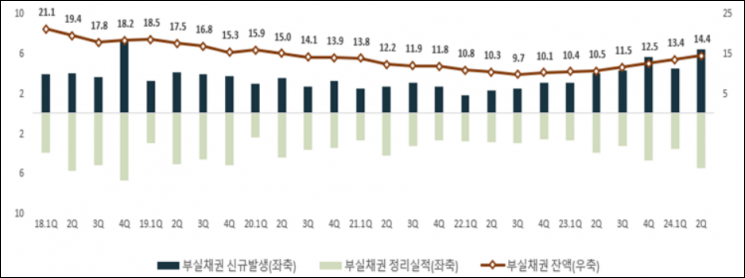

At the end of June this year, the balance of non-performing loans (NPLs) at domestic banks reached 14.4 trillion won, marking the highest level in four years. NPLs refer to loans overdue by more than three months and difficult to recover. This is evidence that borrowers' repayment ability is declining due to the impact of high interest rates.

According to the 'Status of Domestic Banks' Non-Performing Loans (Provisional)' released by the Financial Supervisory Service on the 28th, the NPLs of domestic banks at the end of June this year amounted to 14.4 trillion won, an increase of 1 trillion won compared to the previous quarter (13.4 trillion won). This is the largest figure on a quarterly basis since the second quarter of 2020 (15 trillion won). The scale was largest in the order of corporate loans (11.6 trillion won), household loans (2.6 trillion won), and credit card receivables (200 billion won).

In the second quarter of this year alone, new NPLs of 6.4 trillion won occurred. Among these, new corporate loan NPLs increased by 1.9 trillion won from the previous quarter to 5 trillion won. During the same period, new household loan NPLs increased by 100 billion won to 1.3 trillion won. The amount of NPLs resolved in the second quarter was 5.4 trillion won, up 1.9 trillion won from the previous quarter.

At the end of June, the bank NPL ratio was 0.53%, up 0.03 percentage points from the previous quarter (0.50%). The NPL ratio is the proportion of NPLs to total loans and is a representative soundness indicator of banks. From 2013 to June 2024, the average NPL ratio was 1.06%, and it is currently managed at about half that level. The NPL ratio steadily declined from 0.97% in 2018 to 0.40% in 2022, then rebounded from last year (0.47%).

The corporate loan NPL ratio was 0.65%, up 0.04 percentage points from the previous quarter (0.61%). Among these, the large corporate loan NPL ratio was 0.44%, down 0.04 percentage points from the previous quarter (0.48%). The small and medium-sized enterprise (SME) loan NPL ratio rose 0.08 percentage points to 0.77% from 0.69% in the previous quarter.

The household loan NPL ratio remained unchanged at 0.27%, while the credit card receivables NPL ratio decreased by 0.01 percentage points to 1.60% from 1.61% in the previous quarter.

The balance of loan loss provisions stood at 27.1 trillion won. It increased by 3.3 trillion won compared to the same period last year but decreased by 100 billion won compared to the previous quarter. The loan loss provision coverage ratio, calculated by dividing loan loss provisions by NPLs, was 188%. As NPLs increased, it fell by 15.1 percentage points from 203.1% in the previous quarter.

An official from the Financial Supervisory Service said, "Although the NPL ratio has been rising since reaching its lowest point (0.38%) in September 2022, it remains significantly lower compared to 2019 (0.77%), before the COVID-19 pandemic. However, since the delinquency rate continues to rise and credit risk may expand due to domestic and external uncertainties, we will strengthen asset soundness management, including the sale and disposal of NPLs and sufficient loan loss provision accumulation."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}