Financial Services Commission Holds Household Debt Review Meeting

Policy Loans Cited as Cause of Household Loan Increase

"Calculate and Manage DSR for All Household Loans Without Exception"

The financial authorities have instructed banks to calculate the Debt Service Ratio (DSR) for all new household loans handled from September onwards. Policy loans and jeonse loans, which were previously exempt from DSR application, are now included in the calculation. Through this, banks plan to establish customized management plans.

On the 21st, the Financial Services Commission held a household debt inspection meeting at the Government Seoul Office to discuss this management direction. The meeting was attended by related agencies such as the Ministry of Economy and Finance, Ministry of Land, Infrastructure and Transport, Bank of Korea, Financial Supervisory Service, as well as the Korea Federation of Banks, the Second Financial Sector Association, and the five major commercial banks (KB Kookmin, Shinhan, Hana, Woori, NH Nonghyup).

The financial authorities stated that it is a necessary time for proactive household debt management to prevent abundant market liquidity from excessively flowing into the real estate market or household debt sector. First, banks will calculate the DSR without exception for all new household loans handled from September for internal management purposes. This includes jeonse loans, policy loans (Didimdol, Buteemok, Bogeumjari Loan, etc.), interim payment and moving cost loans, and loans under 100 million KRW, which currently do not have DSR applied. DSR levels will also be calculated according to loan type, region, and borrower income. The DSR is calculated by dividing the annual principal and interest repayment amount by the annual income. For the newly calculated policy loans, principal and interest refer to the actual principal and interest; for interim payment and moving cost loans, it refers to the principal and interest based on a 25-year maturity; and for jeonse loans, it refers to the actual interest burden. Calculating the DSR allows identification of whether excessive loans are being made relative to the borrower's repayment capacity. Since the DSR is calculated for internal management purposes, it does not affect borrower loan limits.

Didimdol and Buteemok loans are products that allow low-income and non-homeowners to borrow at relatively low interest rates. Didimdol (annual 2.45~3.55%) is for purchasing a home, and Buteemok (annual 2.1~2.9%) is for jeonse deposits, with additional interest rate benefits depending on the number of children or whether the household is newlywed. The Bogeumjari Loan can be borrowed for purchasing, loan repayment, or jeonse deposit return purposes for homes priced under 600 million KRW.

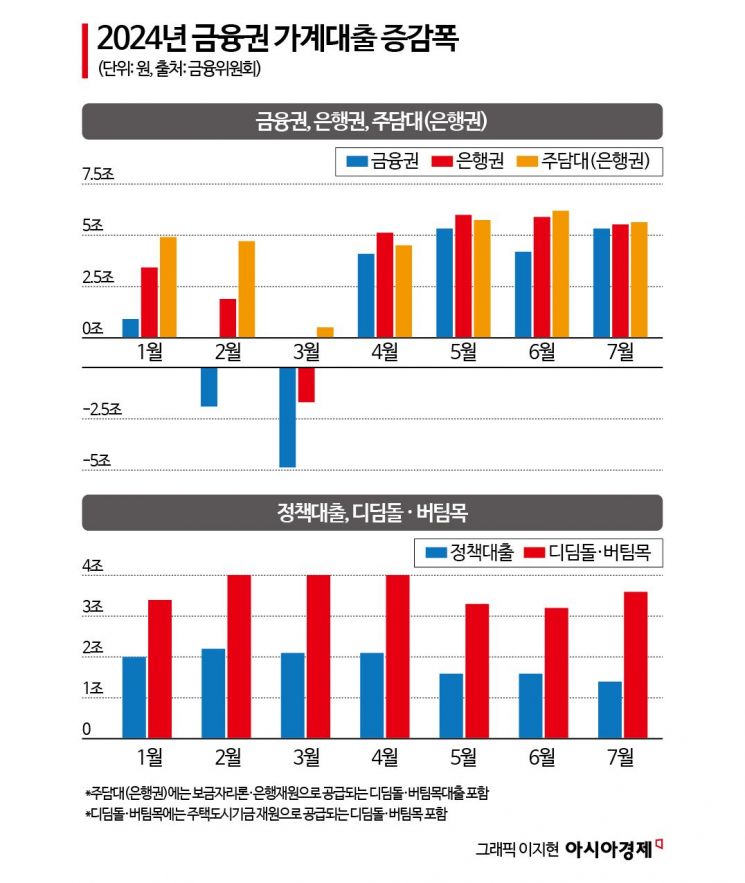

The reason for calculating DSR for such policy loans and jeonse loans is that bank mortgage loans and policy loans have been identified as causes of the increase in household loans in the financial sector. The recent household loan status was also reviewed at this meeting. Household loans in the financial sector increased by 4.1 trillion KRW in April this year, and the upward trend continued in May (5.3 trillion KRW), June (4.2 trillion KRW), and July (5.3 trillion KRW). In particular, bank mortgage loans increased by 6.2 trillion KRW in June, and policy loans excluding Bogeumjari Loans (Didimdol and Buteemok loans) showed an increasing trend from January to July. Bogeumjari Loans have been decreasing since this year due to stricter requirements (homes under 600 million KRW and combined annual income under 70 million KRW for couples) and higher interest rates compared to commercial bank mortgage loans (3.95~4.25% annually as of July). Additionally, the continued decline in market interest rates due to expectations of rate cuts since the end of last year and the real estate price rise centered in Seoul are estimated to be driving the increase in household debt.

Banks can continuously monitor DSR information and establish household debt management plans accordingly. The financial authorities plan to continuously monitor banks' DSR management status, including requiring banks to submit DSR management plans when establishing household loan management business plans from next year.

The second phase stress DSR, which the government announced the day before, was also included in the household debt management measures. The second phase stress DSR is a system that calculates the DSR by adding a certain level of stress interest rate to reflect future interest rate fluctuation risks for household loan borrowers. In the first phase implemented in February, the stress interest rate was applied at 0.38 percentage points. In the second phase, it applies to bank mortgage loans, credit loans, and second financial sector mortgage loans, with a stress interest rate of 0.75 percentage points. For mortgage loans in the metropolitan area (Seoul, Gyeonggi, Incheon), which have been identified as a cause of household debt, the stress interest rate is raised to 1.2 percentage points.

The financial authorities will monitor future household debt trends and real estate market conditions and consider additional measures such as expanding the scope of DSR application or raising risk weights on bank mortgage loans if necessary, implementing them step by step. Kwon Dae-young, Secretary-General of the Financial Services Commission, who chaired the meeting, said, “It is time for related ministries and the financial sector to work together with high vigilance to manage household debt,” and added, “Since banks are starting to calculate DSR for internal management purposes rather than responding mainly through loan interest rates, we expect them to respond by carefully reviewing loan execution and limits through strict repayment ability assessments.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}