Korea Capital Market Institute Publishes Report on Development Plans for Token Securities

As the token securities market is expected to grow to a scale of 367 trillion won by 2030, voices are calling for the urgent establishment of related legal systems.

Kim Gap-rae, Senior Research Fellow at the Korea Capital Market Institute, pointed out in the report titled "Key Issues and Development Plans for Establishing Token Securities Issuance and Distribution Systems," published on the 20th, that "along with the legislative enactment of related amendment bills concerning the Electronic Securities Act and the Capital Markets Act, related subordinate regulations must also be promptly revised."

Token securities are digitalized securities under the Capital Markets Act utilizing distributed ledger technology. They are distinguished from 'virtual assets,' which belong to digital assets rather than securities. Although similar to electronic securities, token securities are characterized by the use of decentralized blockchain technology. By leveraging this, all products including artworks, real estate, and music copyrights can be securitized and traded like stocks.

Researcher Kim emphasized, "For the sustainable development of the nascent token securities ecosystem, it is necessary to institutionalize the distribution system of this new form of financial product called token securities, and also focus on institutional improvements for technological innovation of distributed ledger trading platforms and diversification of over-the-counter trading facilities," urging the National Assembly to expedite legislation.

The report, citing analysis from Hana Financial Management Research Institute, forecasted that the domestic token securities market will grow to 367 trillion won by 2030. The largest share of the total market is expected to be non-financial assets (29.8%), followed by stocks (24.2%), real estate (19.9%), other financial assets (18.6%), and funds and bonds (7.5%). However, this optimistic outlook is conditional upon the establishment of proper legal systems.

Researcher Kim noted, "Since the token securities market is essentially a securities market, it is subject to existing securities laws (Capital Markets Act). Issuance and distribution of token securities in a securities market that is strongly regulated by securities laws without legislative reflection of the characteristics of tokenization is very difficult."

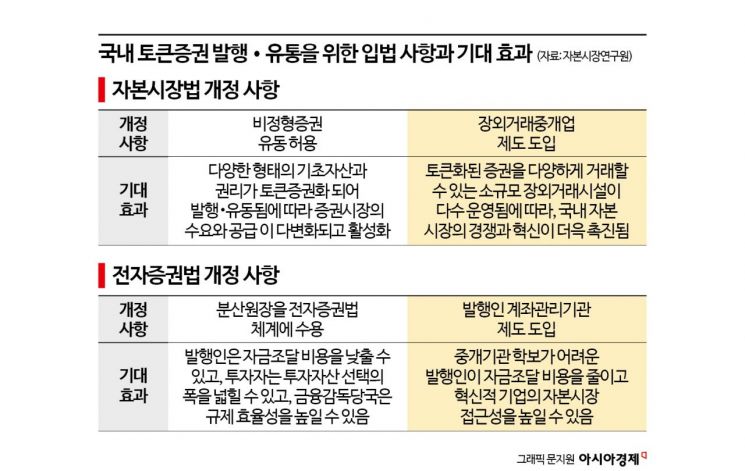

Need for Amendments to the Electronic Securities Act and Capital Markets Act

Currently, there are two major areas requiring legal amendments. The first concerns the Electronic Securities Act, where in the short term, amendments to the Electronic Securities Act granting presumptive rights to distributed ledgers and revisions to subordinate regulations are necessary. Specific discussion points include △eligibility requirements for distributed ledgers △qualification requirements for issuer account management institutions △authority and responsibilities of account management institutions and electronic registration institutions (such as total volume management) △methods for recording, preserving, and disposing of token securities transaction information.

In the long term, it is necessary to recognize the innovation and utility brought by tokenization of payment methods in addition to tokenization of underlying assets and to make institutional adjustments accordingly. Researcher Kim explained, "Tokenized payment methods are effective when based on programmed real-time gross settlement (RTGS). Increasing interoperability and standardization levels among token securities mainnets can maximize the efficiency of tokenized delivery versus payment (DvP) systems."

The second area concerns the Capital Markets Act, where an amendment bill is needed mainly to establish systems related to the distribution of non-standard securities and over-the-counter brokerage businesses. Specific discussion points include △deletion of the proviso clause on investment contract securities △provisions for issuing non-monetary trust beneficiary certificates △clauses related to over-the-counter brokerage businesses △investment limit restrictions for general investors.

Researcher Kim stated, "In the long term, it is necessary to institutionalize and apply unified regulatory principles under the Capital Markets Act for various over-the-counter trading facilities where token securities and traditional unlisted securities can be traded. Additionally, consideration should be given to relaxing or abolishing sales regulations, which are excessively restrictive for modernized over-the-counter trading today."

However, it is expected to take time for token securities-related laws to pass in the National Assembly. With the defeat of lawmakers Yoon Chang-hyun and Kim Hee-gon of the People Power Party, who led related legislative efforts, the 22nd National Assembly lacks a legislative focal point. The National Assembly's Political Affairs Committee is also a 'half committee' without the ruling party. Currently, the committee consists of 14 members from the Democratic Party of Korea, 1 from the Party for Innovation and Justice, and 1 from the Social Democratic Party.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}