Textile and Apparel Industry Shows Lowest Profitability in Past Year

Uncertain Rebound in Second Half Following First Half

Focus on OEM Companies with Improving Front-End Demand

The stock prices in the apparel sector continue to underperform. Most securities firms predict that the downturn in apparel companies will persist into the second half of the year. However, in the case of Original Equipment Manufacturing (OEM), some companies with high visibility for performance recovery from a mid- to long-term perspective are expected to present investment opportunities.

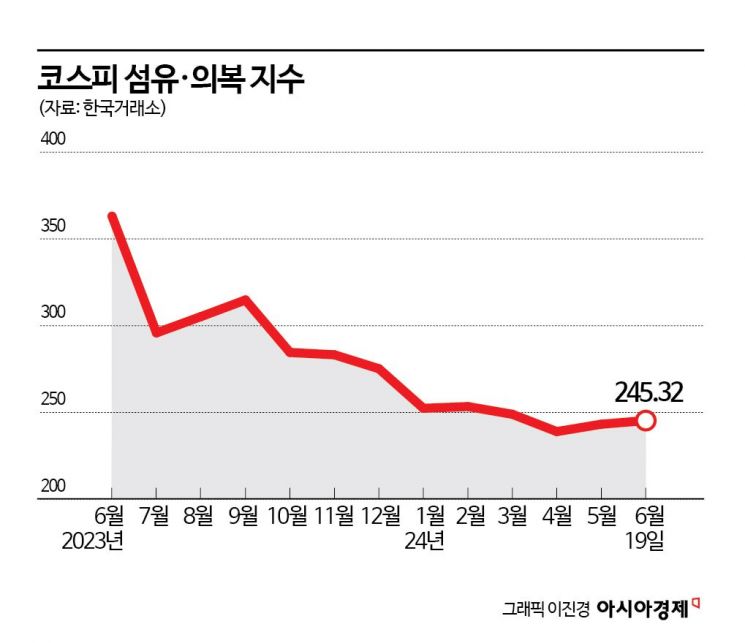

According to the Korea Exchange on the 20th, the KOSPI Textile and Apparel Index has fallen 36.79% over the past year, making it the worst-performing sector among all industries. During the same period, the KOSDAQ Textile and Apparel Index also dropped 39.57%, indicating a prolonged slump across the apparel sector. In particular, the stock prices of companies with large market capitalization such as F&F (-51.85%), Hansome (-25.88%), and LF (-12.55%) were weak, contributing to the sector index decline.

Securities analysts attribute the apparel sector's poor performance to weak demand for clothing amid a macroeconomic environment characterized by high inflation, high interest rates, and low growth. As a result, apparel companies are expected to continue experiencing sluggish earnings for the time being. So Sojeong, a researcher at Kiwoom Securities, said, "The textile and apparel industry is especially sensitive to changes in the macro environment, and currently, consumer conditions in most countries except the U.S. are unfavorable," adding, "Apparel companies' earnings are expected to remain weak in the second half of the year." However, she noted, "Not all companies are performing poorly. Some companies show growth trends depending on consumer trends or individual issues, so a selective approach is necessary," and explained, "Attention should be paid to changes in demand for cost-effective consumption and mid- to low-priced apparel."

Hyung Kwonhoon, a researcher at SK Securities, also said, "Apparel consumption was sluggish in the first half, which was the expected outcome," adding, "In the second half, brands with a large domestic sales ratio or products in the maturity stage will inevitably have limited stock price upside." He continued, "However, companies with brand growth or export momentum may have opportunities," pointing out, "In the case of Fila Holdings, recent rebranding results seem to be gradually becoming visible."

Meanwhile, even within the apparel sector, relatively positive outlooks are emerging for OEM companies rather than brands or fashion distribution. Yoo Jeonghyun, a researcher at Daishin Securities, said, "Companies that had experienced excessive inventory problems have resolved inventory backlogs through efforts to reduce stock, and now they need to increase inventory for actual sales," adding, "Looking at U.S. companies' apparel inventory-related indicators, it is confirmed that there is no inventory buffer for new products for the next season's sales, so the inventory accumulation trend is expected to be optimistic for the time being." He further noted, "Companies like GAP and Adidas, which focused on inventory reduction by cutting orders last year, are showing steep profit growth this year," and added, "Vendor companies such as Hansae Co., Ltd. and Hwasung Enterprise are likely to see simultaneous improvements in orders and performance this year."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}