Geonsanyeon Predicts 0% Drop in Seoul Metropolitan Area and 2.5% Decline in Provinces

Apartment Prices in Seoul Metropolitan Area Rose 0.8% from January to March

"Policy Finance Balance Low and Limited Interest Rate Cuts Keep Downward Trend"

Nationwide Jeonse Prices Expected to Rise Additional 2.8% in Second Half of Year

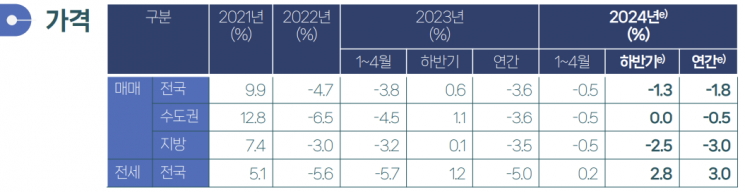

It is forecasted that nationwide housing sale prices will decline by 1.3% in the second half of this year, with the metropolitan area maintaining stability and regional areas expected to fall by 2.5%. Meanwhile, jeonse prices are anticipated to rise by 2.8% in the second half.

Real Estate Sale and Jeonse Price Forecast for the Second Half of 2021-2024 (Source: Korea Real Estate Research Institute)

Real Estate Sale and Jeonse Price Forecast for the Second Half of 2021-2024 (Source: Korea Real Estate Research Institute)

Due to policy financing such as the special loan for newborns, capital is flowing into the metropolitan area, leading to the depletion of the lowest-priced listings first, suggesting a possible rise due to a base effect in the metropolitan area. However, considering the insufficient balance of policy funds, the limited extent of interest rate cuts compared to expectations, and the perceived economic slowdown, a nationwide downward trend is expected to continue in the second half.

On the 11th, the Construction Industry Research Institute held the '2024 Second Half Construction and Real Estate Market Outlook Seminar' at the Construction Hall in Gangnam-gu, Seoul. The institute analyzed that nationwide sale prices will fall by 1.8% annually this year, while jeonse prices will rise by 3.0%. The institute adjusted the decline forecast downward from the initial estimate of a 2.0% drop, influenced by the inflow of 5.2 trillion won in policy funds during the first half, which helped restore consumer sentiment.

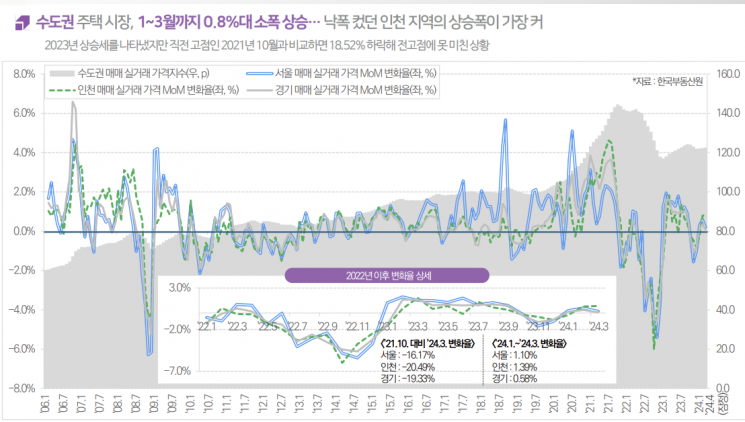

Apartment Sale Price Fluctuation Trends in the Seoul Metropolitan Area (Source: Korea Construction Industry Research Institute)

Apartment Sale Price Fluctuation Trends in the Seoul Metropolitan Area (Source: Korea Construction Industry Research Institute)

From January to March, apartment sale prices in the metropolitan area rose by around 0.8%, with Incheon, which had experienced a significant decline, showing the largest increase. The sale price change rates from January to March were 1.0% in Seoul, 1.39% in Incheon, and 0.58% in Gyeonggi. However, compared to the previous peak in October 2021, prices remain 18.52% lower.

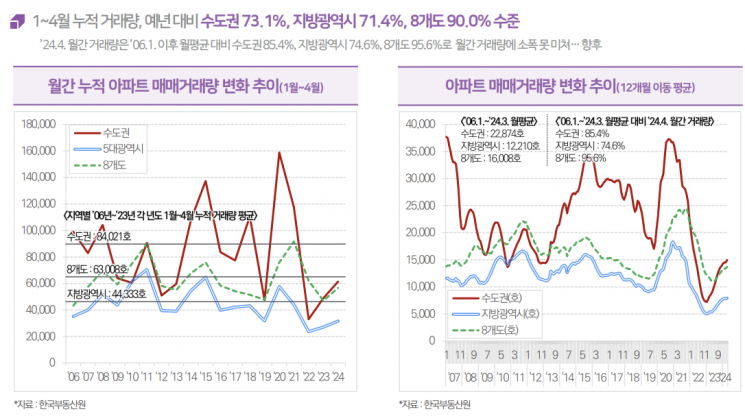

Although transaction volumes increased from January to April, they remain below historical averages. The cumulative apartment sale transaction volume from January to April reached only 73.1% of the usual level in the metropolitan area and regional metropolitan cities, and 90.0% in the eight provinces.

Apartment Sales Transaction Volume Trend from January to April 2024 (Source: Korea Real Estate Research Institute)

Apartment Sales Transaction Volume Trend from January to April 2024 (Source: Korea Real Estate Research Institute)

Kim Seong-hwan, a senior researcher at the Construction Industry Research Institute, predicted, "The balance of sale-related policy financing available for operation during the remainder of 2024 is relatively low, and considering bank loan margins, the potential for interest rate cuts is limited, so the downward trend is expected to continue."

The institute expects housing prices in the second half to continue declining, especially in regional areas, due to limited room for interest rate cuts and a political environment dominated by opposition parties. Concerns over real estate project financing (PF) require the cleanup of troubled projects, and the anticipated onset of financial instability in the second half may also dampen demand.

In the metropolitan area, prices are expected to remain stable in the second half. Although the decline narrowed until April in regional areas, a renewed drop is likely in the second half. Pressure to raise sale prices remains due to increased construction costs and expected reductions in supply, so the decline in sale prices is not expected to be significant.

Senior researcher Kim stated, "Among the major pledges of ruling and opposition candidates mentioned in the last general election, those considered feasible have likely already been reflected in market prices. If the market does not experience a sharp drop again, there is little incentive for additional policy factors to directly impact prices."

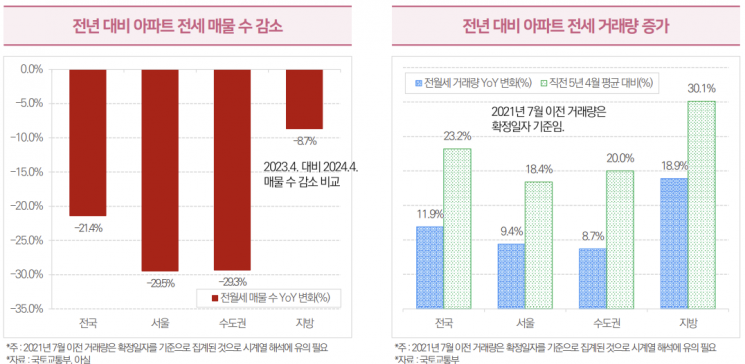

Particularly, the jeonse market rose by 0.2% in the first half and is expected to increase by 2.8% in the second half. More jeonse policy funds flowed in than for sales until April, and due to avoidance of jeonse in row houses and multi-family houses, the upward trend is likely to continue centered on small apartments. As of April, the number of apartment jeonse listings decreased by 29.5% in Seoul and 29.3% in the metropolitan area compared to the previous year. Jeonse transaction volumes in April also increased by 18.4% in Seoul and 20.0% in the metropolitan area compared to the five-year average. The monthly rent trend in non-apartment lease markets is expected to accelerate due to jeonse fraud and other factors.

Senior researcher Kim explained, "Jeonse loan interest rates are steadily declining, and demand inflow is expected due to reduced sale demand, while annual move-in volumes are projected to slightly decrease compared to 2023."

Number of Jeonse Listings and Jeonse Transaction Volume from January to April 2024 (Data=Konsanyeon)

Number of Jeonse Listings and Jeonse Transaction Volume from January to April 2024 (Data=Konsanyeon)

This year’s permits and public supply volumes meet the levels mentioned in supply measures, but the impact on the private sector is expected to be limited. Permits are estimated at 370,000 households, and pre-sale volumes at 260,000 households. Compared to the previous year, permits decreased by about 59,000 households, while pre-sale volumes increased by 68,000 households.

Senior researcher Kim said, "Although the backlog of unstarted construction since 2022 has improved compared to last year (192,000 households), this is due to a base effect," adding, "The supply volume is at the same level as during the global financial crisis in 2008."

He emphasized, "While the recent rise in sale prices is important, it is also necessary to consider that the macroeconomic environment that led to the housing price decline has not changed significantly. Rather than anticipating market movements such as unrealized interest rate cuts prematurely, it is a time to be somewhat cautious, considering that homeownership is a long-term plan spanning 30 years."

Domestic construction orders this year are expected to decrease by 10.4% compared to the previous year. Construction orders, which reached a record high of 229.7 trillion won in 2022, fell by 17.4% to 189.8 trillion won last year and are estimated to decline further by 10.4% to 170.2 trillion won this year.

The institute forecasts domestic construction investment this year to decrease by 1.3% from the previous year to 302.1 trillion won. Due to the decline in building starts in 2022 and last year, residential and non-residential construction work is expected to weaken, turning to a downward trend in the second half.

Researcher Lee Ji-hye of the Construction Industry Research Institute said, "High interest rates will continue in 2024, and real estate PF restructuring will intensify in the second half, causing ongoing difficulties in corporate financing conditions. Construction companies need to manage liquidity and financial stability, seek ways to enhance mid- to long-term competitiveness through technological investment, and continue efforts to diversify their portfolios."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}