Limited Impact on Fund Depletion Timing Even with Enhanced Guarantees

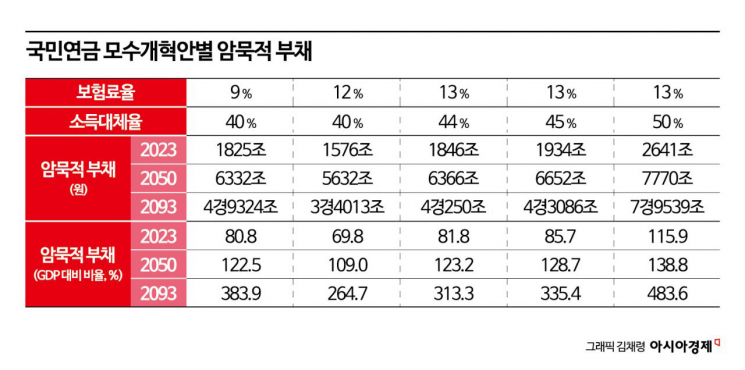

Implicit Debt of 2641 Trillion Won if Income Replacement Rate is 50%

"Focusing Only on Depletion Timing is an 'Illusion'... Must Consider Implicit Debt"

Amid claims mainly from opposition parties that increasing the income replacement rate of the National Pension to strengthen coverage does not significantly advance the depletion timeline, an analysis has emerged suggesting that future discussions on National Pension reform should consider the scale of implicit debt (unfunded liabilities). Even if the income replacement rate is raised, the fund depletion point changes by only about five years, but the implicit debt, which is debt passed on to younger generations, increases astronomically.

Implicit debt is an indicator used to assess the financial soundness of the National Pension, calculated as the total amount of benefits to be paid to pension subscribers minus the insurance premiums collected from them. Although it is not a debt that must be repaid immediately, it is considered debt passed on to younger generations because future generations will have to cover it through taxes and insurance premiums.

Source: 5th National Pension Fund Calculation Committee Financial Stability Plan Announcement Materials

Source: 5th National Pension Fund Calculation Committee Financial Stability Plan Announcement Materials

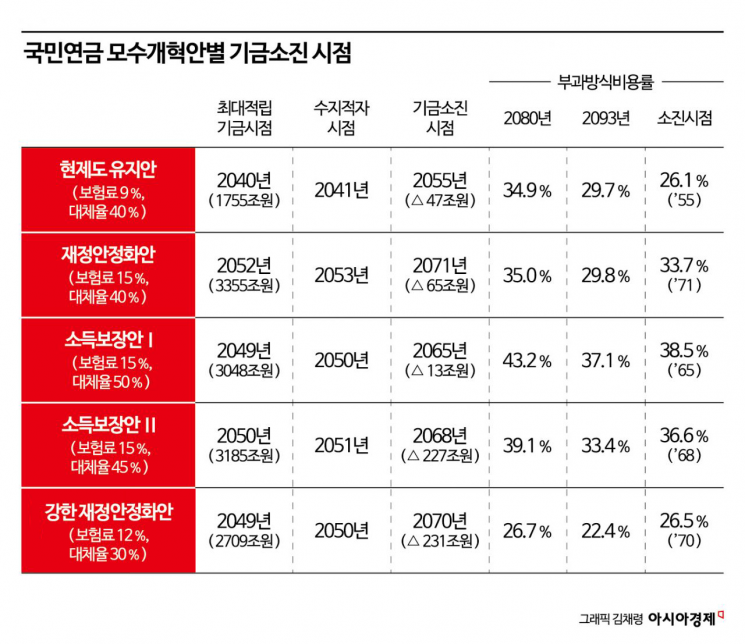

According to the “Financial Projections by National Pension Parameter Reform Plans” document from the 5th National Pension Financial Calculation Committee obtained by Asia Economy on the 7th, the “Strengthened Financial Stabilization Plan” (insurance premium rate 12%, income replacement rate 30%) would lead to pension depletion by 2070. In contrast, the “Income Guarantee Plan” (insurance premium rate 15%, income replacement rate 50%), which strengthens coverage, would see depletion by 2065. Although the Income Guarantee Plan requires paying 3 percentage points more in premiums and provides 20 percentage points higher pension benefits than the Strengthened Financial Stabilization Plan, the depletion point is only about five years earlier.

Other scenarios also showed little change in the National Pension depletion timeline. Lowering the income replacement rate by 5 percentage points to 45% compared to the Income Guarantee Plan results in fund depletion in 2068. Under the “Financial Stabilization Plan,” which raises the insurance premium rate to 15% while maintaining the current income replacement rate (40%), the pension fund is depleted in 2071. Even with a 10 percentage point difference in the income replacement rate at the same 15% premium rate, the depletion point differs by only six years.

Source: Estimated scale of unfunded liabilities by National Pension reform plan (Professor Jeon Young-jun, Hanyang University)

Source: Estimated scale of unfunded liabilities by National Pension reform plan (Professor Jeon Young-jun, Hanyang University)

However, implicit debt increases significantly as the income replacement rate rises. Under the current National Pension system, implicit debt stood at 1,825 trillion won last year, equivalent to 80.8% of the gross domestic product (GDP). If the insurance premium rate is raised to 12% while keeping the income replacement rate at 40%, implicit debt decreases by 249 trillion won to 1,576 trillion won. Conversely, raising the insurance premium rate and income replacement rate to 13% and 50%, respectively, increases implicit debt to 2,641 trillion won (115.9% of GDP).

The burden of implicit debt grows sharply over time. If the current National Pension system is maintained, implicit debt will exceed 6,000 trillion won by 2050 and approach 500 trillion won (5,000 trillion won) by 2093, equivalent to 383.9% of GDP. If the insurance premium rate and income replacement rate are raised to 13% and 50% to strengthen coverage, implicit debt will near 8,000 trillion won in about 25 years and reach 800 trillion won (8,000 trillion won) in about 70 years, equivalent to 483.6% of GDP.

The problem is that implicit debt ultimately represents debt passed on to future generations. As implicit debt increases, the net tax burden on the current generation decreases somewhat, but the net tax burden on future generations soars. Raising the income replacement rate to 50% results in an increase in the net tax burden for future generations amounting to 2% of lifetime income.

Yoon Seok-myung, Honorary Research Fellow at the Korea Institute for Health and Social Affairs, emphasized that the reason the fund depletion timeline remains similar regardless of fluctuations in the income replacement rate is a “shocking phenomenon that occurs because the golden time for pension reform has passed.” He added, “If pension reform had been completed at least during the Moon Jae-in administration, there would have been meaningful changes in the fund depletion timeline. Now, focusing only on the depletion timeline can create the illusion that strengthening coverage does not pose significant problems for the National Pension’s soundness. It is time to discuss insurance premium rates and income replacement rates while considering implicit debt.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}