Hyundai, Lotte, Woori Shrink... "Need to Improve Cost Efficiency"

Real Delinquency Rate Surpasses 2%, Soundness Shows 'Red Light'

The card industry secured profitability in the first quarter of this year but missed out on soundness. While the total net profit of domestic card companies increased by 24% compared to last year, their performance diverged due to 'cost management.' The delinquency rate exceeded 2% in half of the card companies, raising warning signs about financial soundness.

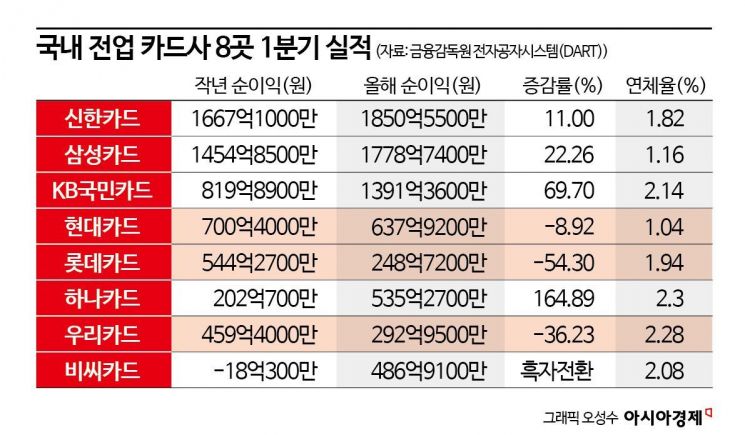

According to each card company on the 17th, the net profit attributable to controlling shareholders of the eight domestic full-service card companies (Shinhan, Samsung, KB Kookmin, Hyundai, Lotte, Hana, BC, and Woori Card) in the first quarter of this year totaled 722.2 billion KRW. This represents a 23.88% increase from 582.9 billion KRW in the first quarter of last year.

By company, five card companies?Shinhan, Samsung, Kookmin, Hana, and BC Card?showed improved performance. Shinhan Card, the number one credit card company, recorded a net profit of 185 billion KRW in the first quarter of this year, an 11% increase compared to the previous year. During the same period, Samsung Card's net profit rose 22.2% from 145.4 billion KRW to 177.8 billion KRW. Kookmin Card achieved a 69.7% growth with a net profit of 139.1 billion KRW, and Hana Card recorded a 164.9% increase with 53.5 billion KRW in net profit. BC Card, which posted a net loss for the first time in a quarter last year, returned to profitability with 48.7 billion KRW in the first quarter of this year.

However, Hyundai, Lotte, and Woori Cards underperformed. Lotte Card's net profit decreased the most, dropping 54.3% from 54.4 billion KRW in the first quarter of last year to 24.8 billion KRW this year. During the same period, Woori Card's net profit fell 36.2% to 29.3 billion KRW, followed by Hyundai Card with an 8.9% decrease to 63.7 billion KRW.

The divergence in performance was due to cost management. Card companies with increased net profits collectively stated that "despite the overall deterioration in the operating environment, including funding costs, efficient cost management generated profits." On the other hand, the operating expenses of the three underperforming card companies showed that financial costs (interest expenses) surged by about 30% in the first quarter compared to the same period last year. Woori Card's interest expenses increased 35.4%, from 81.2 billion KRW in the first quarter last year to 110 billion KRW this year. Lotte and Hyundai Cards' interest expenses rose by 30.5% and 28.3%, respectively.

In Hyundai Card's case, bad debt expenses also hampered performance growth. Hyundai Card's bad debt expenses doubled to 139.2 billion KRW in the first quarter of this year from 65.7 billion KRW in the first quarter of last year. A Hyundai Card official said, "Operating income increased due to higher credit sales," but added, "Because we expanded financial products focusing on high-quality members, the provision for bad debts increased, which led to a decrease in operating profit and net profit."

Some card companies saw a deterioration in soundness as the actual delinquency rate exceeded 2%. The actual delinquency rate is an indicator that includes refinancing loan claims and represents the ratio of claims overdue by more than one month. Half of the eight card companies had an actual delinquency rate exceeding 2%. Hana Card had the highest delinquency rate at 2.3%, followed by Woori Card (2.28%), Kookmin Card (2.14%), and BC Card (2.08%). Lotte Card (1.94%) and Shinhan Card (1.82%) approached the 'critical 2%' delinquency rate threshold.

An industry insider said, "The delinquency rate in the card industry is rising due to external factors such as inflation, economic slowdown, and continued interest rate instability," adding, "The delinquency rate is still within a manageable range. The industry as a whole will monitor delinquency rates, vulnerable borrowers, and market conditions carefully."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}