Currently Limited to Crop and Livestock Disaster Insurance

Insurance Research Institute "Need for Personal Injury and Productivity Loss Coverage Products"

Proposal of 'Index Insurance' Paying Fixed Benefits Based on Weather Indicators

Beyond policy insurance primarily targeting crops, livestock, and aquaculture as insurance products to prepare for climate change, the need for products that compensate for personal injuries or productivity decline has been raised.

According to the May report from the Korea Insurance Research Institute on the 16th, the need for small-scale insurance products for individuals to prepare for climate change is growing. Unlike insurance that compensates for crop or livestock disasters, these products allow individuals to receive compensation for damages that may occur when natural disasters such as heatwaves happen.

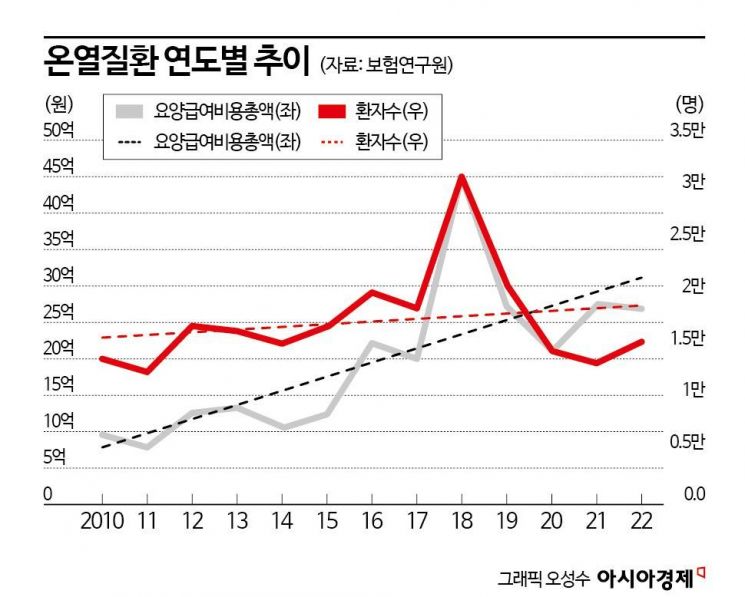

So far, the amount of insurance payouts due to abnormal climate events has steadily increased. According to the Korea Insurance Research Institute, payouts for crop disaster insurance rose from 1.4 billion KRW in 2001 to 555.8 billion KRW in 2022, and livestock disaster insurance payouts increased from 4.2 billion KRW to 155.2 billion KRW during the same period, representing increases of 397 times and 37 times respectively. Subscription rates also increased accordingly. During the same period, crop disaster insurance subscription rates expanded significantly from 17.5% to 49.9%, and livestock disaster insurance from 21.7% to 94.6%.

However, these climate change-related insurance products are designed to prepare for cases where large-scale damages occur due to natural disasters or accidents, causing significant harm to industries or society. The Korea Insurance Research Institute explains that now there is a need for climate change preparedness products at the individual level as well.

Researcher Cheon Ji-yeon of the Korea Insurance Research Institute stated, "Since climate change is no longer limited to crop damage, it would be meaningful to consider introducing insurance that compensates individuals for physical injuries or productivity decline that may occur during natural disasters such as heatwaves." For example, the number of patients and medical costs for personal heat-related illnesses continue to rise, indicating that problems caused by climate change are expanding not only in some industries but across the board.

In response, insurance products addressing heatwave damage have been launched overseas. The U.S. insurance startup 'Blue Marble' partnered last year with the Rockefeller Foundation and the Self-Employed Women’s Association (SEWA) in India to introduce the 'Extreme Heat Income Insurance' targeting Indian women. This insurance product pays workers $3 per day if a heatwave lasts for more than three days. It aims to compensate for income loss caused by unsafe working conditions due to extreme heat.

The Korea Insurance Research Institute proposed developing small-scale 'index insurance' products for individuals. Index insurance pays out based on objective criteria set according to climate indices such as temperature and precipitation. Unlike general insurance, which determines payouts based on the scale of damage, index insurance sets a predetermined fixed payout regardless of the extent of loss, which reduces the insurer’s burden relatively. Researcher Kim Kyung-sun of the Korea Insurance Research Institute explained, "By providing innovative services across the 'health value chain,' from customer health management to additional services, it is possible to diversify revenue streams."

In particular, to encourage enrollment among low-income groups who are more vulnerable to weather-related health impacts, developing these products into policy insurance could be considered. Researcher Kim Kyung-sun added, "If insurance companies can secure premium subsidies through consultations with local governments as part of climate crisis response measures while developing small-scale insurance products, these could take on the characteristics of policy insurance."

Professor Seo Yong-min of Sangmyung University’s Department of Economics said, "Product composition can vary depending on whether the damage affects property or physical health and life," adding, "However, when setting the index that functions as an indicator to assess risk levels, delicate design is necessary considering that insurance payouts are automatically triggered based on the index." He warned that compensation triggered by the index even without actual loss could cause moral hazard, so caution is needed.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}